Updated on May 19, 2026

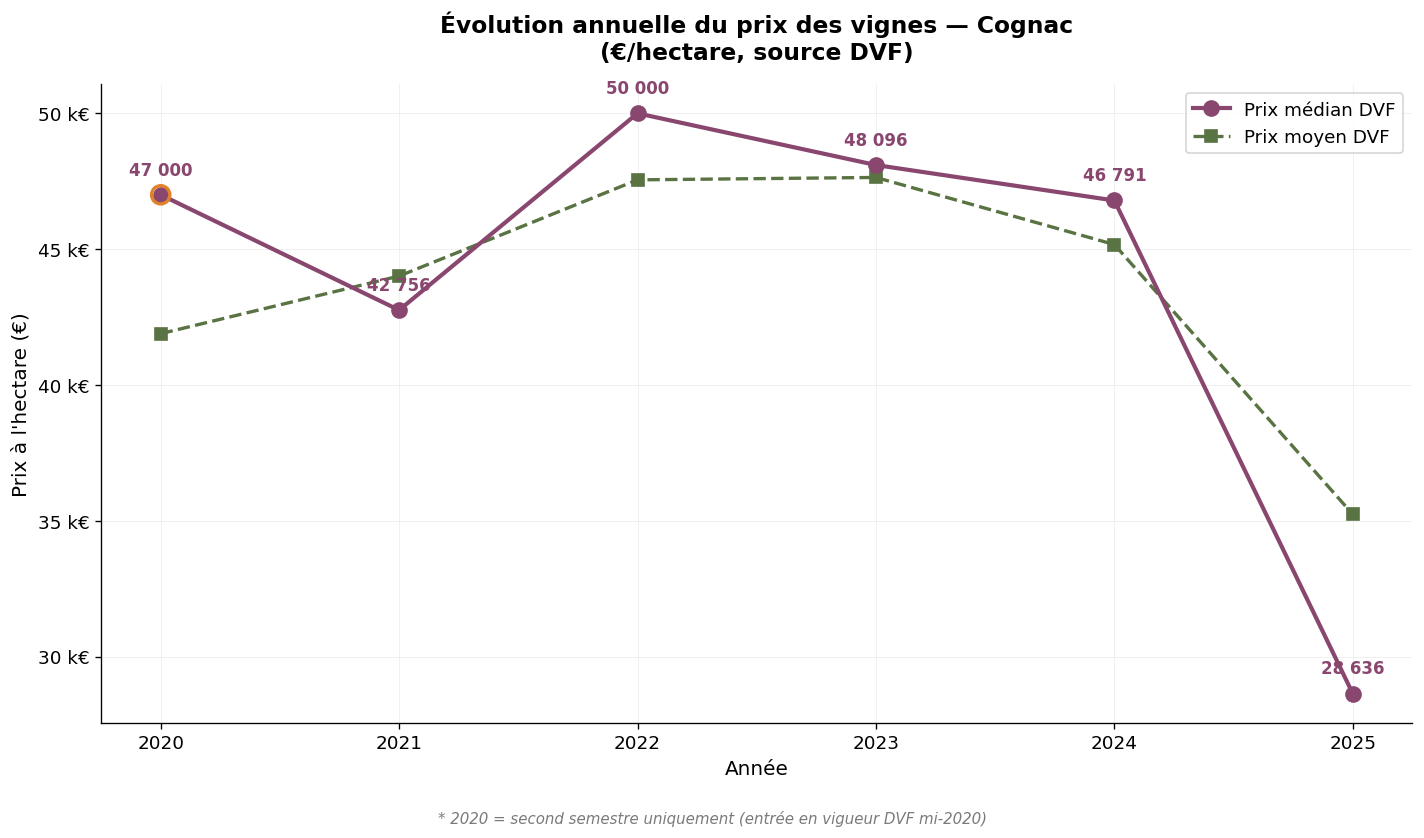

The Cognac vineyard represents a unique case in the French wine landscape: producing a controlled appellation eau-de-vie from a wine-growing area organised around two departments and six delimited crus. With approximately 80,000 hectares planted, Cognac is the second-largest French vineyard by area after Bordeaux. The commercial dynamics of Cognac — heavily export-oriented, particularly towards the American and Chinese markets — give the land market specific cycles, sometimes disconnected from other French wine regions. Here we analyse the price of Cognac vineyard land over the 2020-2025 period, based on DVF (Land Value Requests) data and SAFER references. The 2025 figures, now complete, mark a major shift and serve as our reference; the 2024 figures provide the basis for comparison. The median DVF price for 2025 drops to €28,636/ha (-39% vs 2024), marking a major inflection in the Cognac market. Note: 2020 covers only the second half of the year. This article is part of our observatory of vineyard prices in France.

The Cognac vineyard extends across two departments: Charente-Maritime (17), which covers most of the vineyard, and Charente (16), which notably includes the prestigious Grande Champagne and Petite Champagne crus. The specificity of the market lies in the nature of the grape varieties cultivated (essentially ugni blanc, secondarily colombard and folle blanche) and in the valuation through distillation: the land price is closely correlated with the price of new eaux-de-vie set by the trade association.

Over the entire H2 2020 – 2025 period, our observatory has retained 657 transactions of vineyard land in the Cognac region. The average price stands at €44,683/ha and the median price at €45,249/ha. The near-coincidence between average and median — the average being only slightly below the median — reflects a remarkable homogeneity of the Cognac market. It is one of the tightest distributions of all French vineyards.

| Year | Volume | Average price | Median price | Avg. area (sqm) |

|---|---|---|---|---|

| 2020 * | 57 | €41,888/ha | €47,000/ha | 20,745 |

| 2021 | 118 | €44,009/ha | €42,756/ha | 21,282 |

| 2022 | 131 | €47,551/ha | €50,000/ha | 20,780 |

| 2023 | 161 | €47,639/ha | €48,096/ha | 22,028 |

| 2024 | 119 | €45,169/ha | €46,791/ha | 16,194 |

| 2025 | 71 | €35,237/ha | €28,636/ha | 20,434 |

* 2020: second half only.

Annual trend of DVF prices — Cognac vineyard — Source: DVF, processed by ma-propriete.fr

The main observation is a break in 2025. After four stable years, with a median price oscillating between €42,000 and €50,000/ha, the 2025 median falls to €28,636/ha, a 39% decline compared to 2024. The average follows the same trajectory (-22%), going from €45,169/ha to €35,237/ha. This inflection corresponds to the commercial situation of Cognac: the decline in shipments to China (-43% in value over the 2023-2024 campaign according to BNIC statistics) and the slowdown of the American market have triggered a drop in bulk prices, which is now being transmitted to land values. The transaction volume for 2025 (71 mutations) is also significantly down compared to previous years — a signal of wait-and-see behaviour on both the seller and buyer sides.

For buyers with a structured project and a long-term vision, this correction could represent an interesting entry window into a vineyard whose long-term valuation remains solid (see below, SAFER data). The year 2026 will need to be observed carefully to confirm whether the 2025 decline marks a new regime or a cyclical correction.

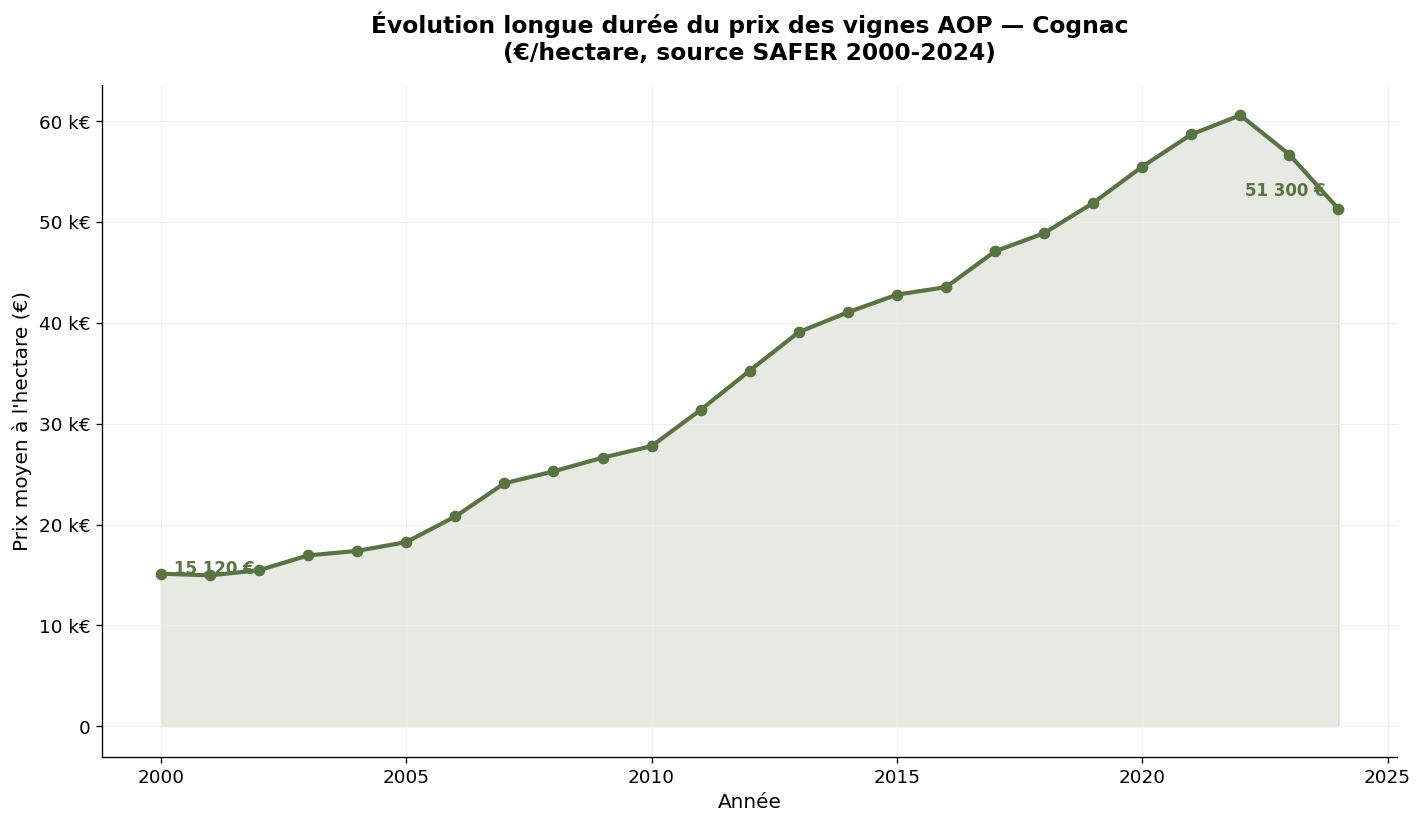

| Year | Average price (€/ha) | 5-year change |

|---|---|---|

| 2000 | 15,120 | — |

| 2010 | 27,779 | + 84% |

| 2015 | 42,805 | + 54% |

| 2020 | 55,500 | + 30% |

| 2023 | 56,700 | + 2% |

| 2024 | 51,300 | - 9.5% |

SAFER average price of AOP Charente-Cognac vineyards — Source: Ministry of Agriculture / SAFER

Over twenty-five years, the SAFER average price of Cognac vineyards has more than tripled, rising from €15,120/ha in 2000 to €51,300/ha in 2024. This is one of the strongest progressions in French wine land over the long term, higher than that observed in Bordeaux and comparable to the Languedoc trajectory in reverse (here upwards). The trajectory reflects the commercial rise of Cognac since the early 2000s, driven by the growth of Asian and North American markets.

The 9.5% decline observed between 2023 and 2024 in the SAFER data, and even more pronounced (-39% on the median) in the 2025 DVF data, confirms the shift. Both sources converge on the direction of the movement, with a stronger amplitude for DVF — which is to be expected: the DVF median incorporates the actual transactional situation of the year, while SAFER smooths out variations.

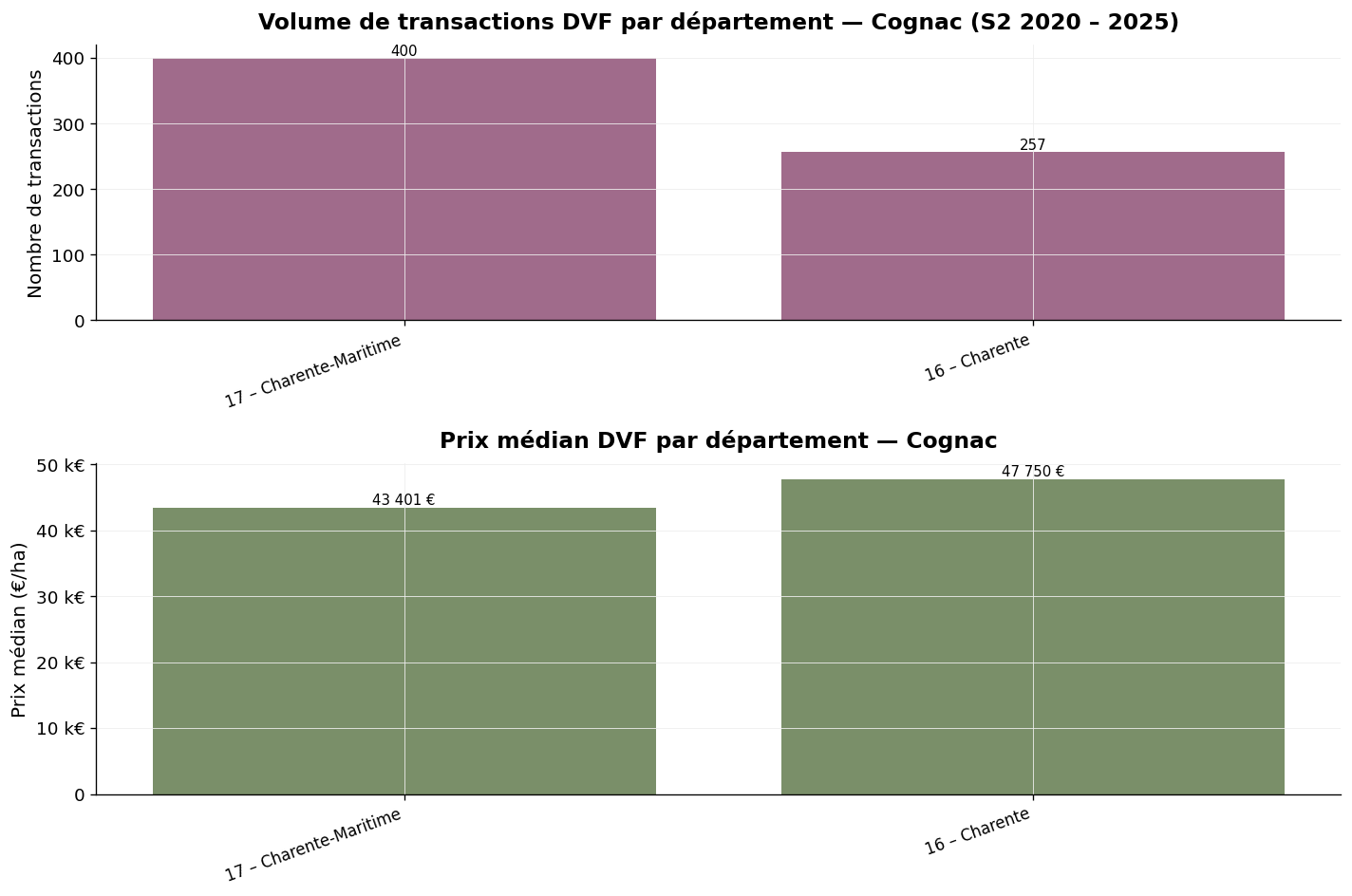

Volume and median price by department — Cognac, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

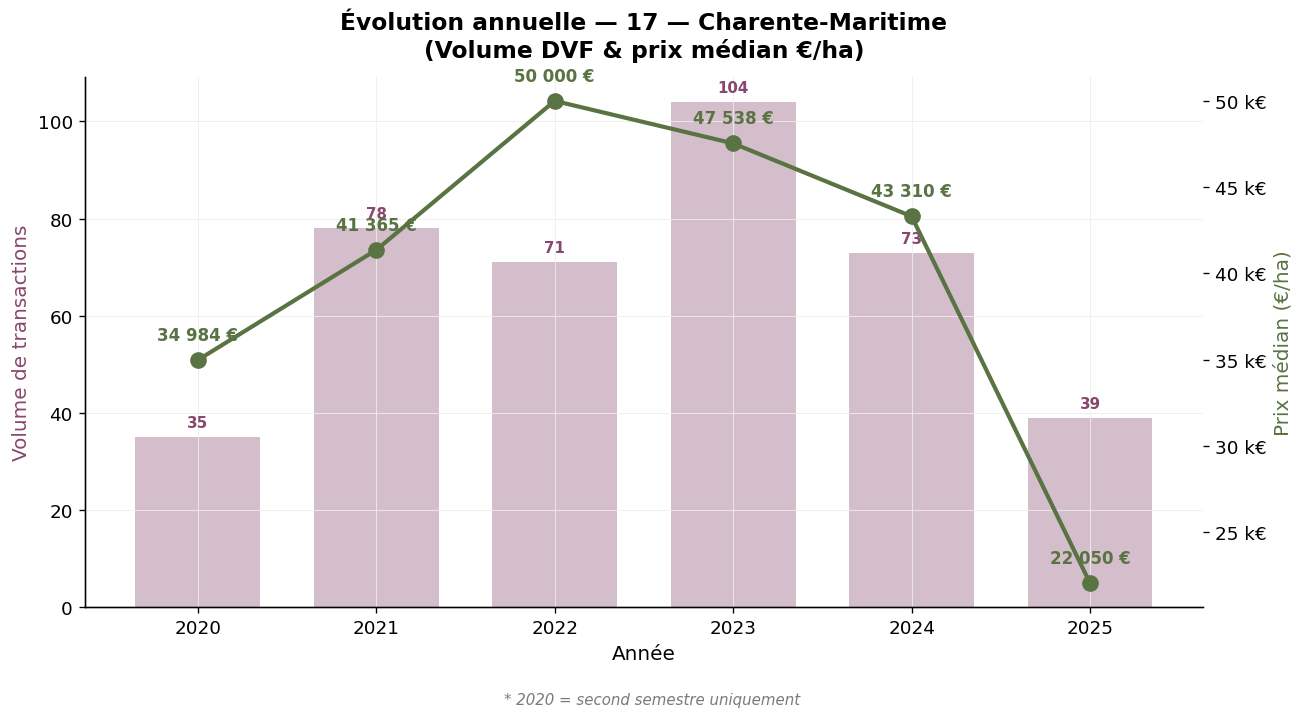

The leading department of the Cognac vineyard by volume (400 transactions), Charente-Maritime covers the Borderies, Fins Bois, Bons Bois and Bois Ordinaires crus. The average price stands at €42,461/ha and the median at €43,401/ha. The average area (18,559 sqm) is consistent with Cognac practices. The annual trend shows a marked decline in 2025 (median at €22,050/ha compared to €43,310/ha in 2024), illustrating the rapid transmission of the commercial situation to land values.

Charente-Maritime (17) — Annual trend — Source: DVF, processed by ma-propriete.fr

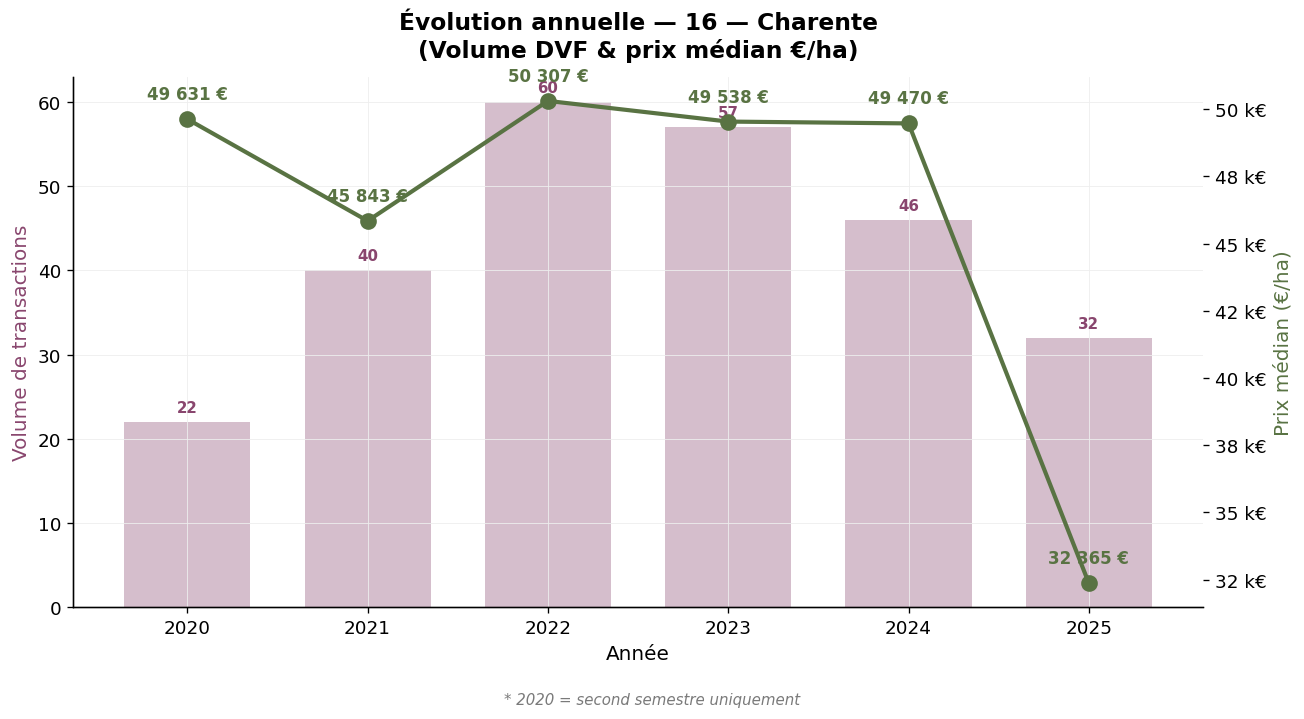

The second department (257 transactions), Charente concentrates the most prestigious crus of the vineyard: Grande Champagne and Petite Champagne. The average price stands at €48,141/ha and the median at €47,750/ha, slightly higher than in Charente-Maritime. The average area (23,022 sqm) is larger, a sign of a more extensive vineyard. The 2025 trend also confirms the decline, with the median dropping from €49,470/ha in 2024 to €32,365/ha in 2025.

Charente (16) — Annual trend — Source: DVF, processed by ma-propriete.fr

The Cognac vineyard is organised around six crus delimited by a 1938 decree, arranged in concentric circles around the town of Cognac. This historical hierarchy remains a major determinant of land value, even though trading practices tend to smooth out, to some extent, the differences. From the most prestigious to the least valued, the crus are as follows: Grande Champagne (Charente, approximately 13,000 hectares), renowned for its finest and longest-aged eaux-de-vie; Petite Champagne (Charente and Charente-Maritime, approximately 16,000 hectares), followed in blending by the famous "Fine Champagne" which combines the two previous crus; Borderies (Charente-Maritime, approximately 4,000 hectares), the smallest cru, sought after for the roundness of its eaux-de-vie; Fins Bois (mainly Charente-Maritime, approximately 33,000 hectares), the largest, which provides the bulk of the trade volume; Bons Bois and Bois Ordinaires (mainly Charente-Maritime, approximately 11,000 hectares in total), the furthest from the heart of the vineyard.

The land value gap between Grande Champagne and Bois Ordinaires can reach a factor of 2 to 3 depending on the transactions. DVF data, aggregated at the department level, does not allow the six crus to be perfectly separated: Charente concentrates Grande Champagne, part of Petite Champagne and Fins Bois; Charente-Maritime mixes Petite Champagne, Borderies, Fins Bois, Bons Bois and Bois Ordinaires. This is why our departmental median (€43,401/ha in Charente-Maritime versus €47,750/ha in Charente) only imperfectly reflects the hierarchy of crus. For an acquisition project targeted at a particular cru, a commune-by-commune cartographic analysis remains essential.

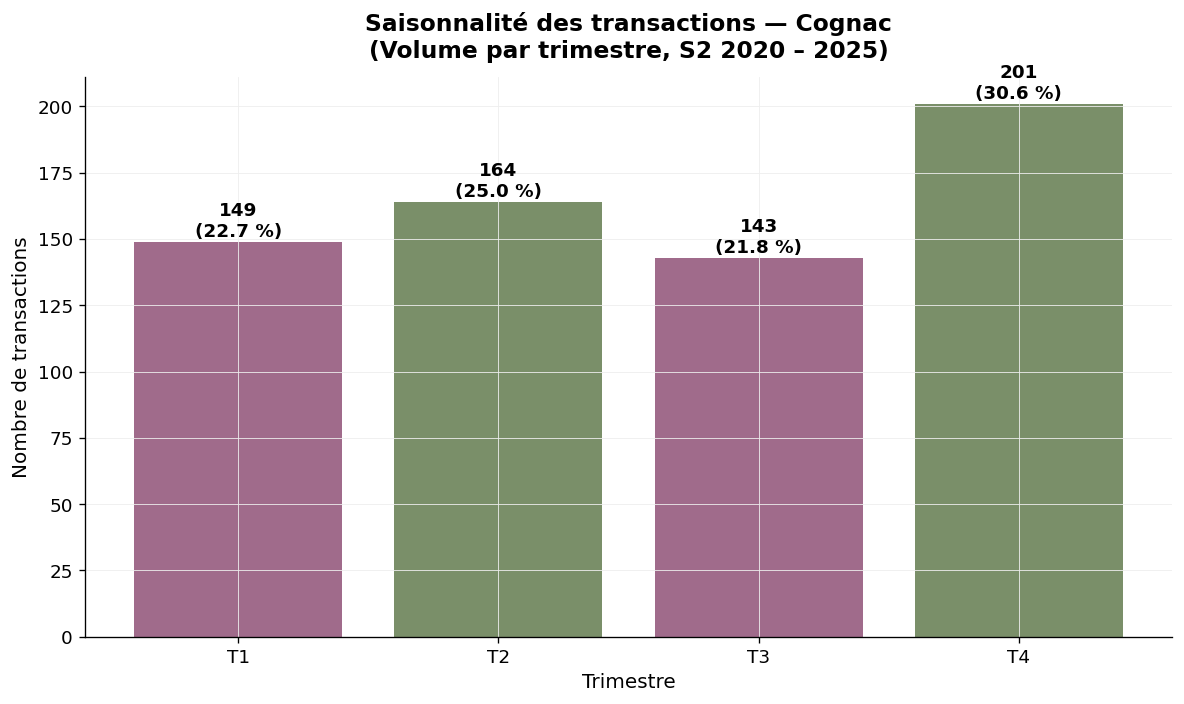

The Cognac market shows a marked seasonality: 52% of transactions are concentrated in the second half of the year, with a peak in the fourth quarter (30.6%). This concentration reflects the classic timetable of vineyard land — fiscal and accounting year-end, freeing up of the calendar after harvest — and the traditional organisation of the eaux-de-vie trade that characterises the Charentes.

Seasonality — Cognac, volume by quarter — Source: DVF, processed by ma-propriete.fr

The DVF database (Land Value Requests) lists all property transfers for valuable consideration recorded by the DGFiP. To isolate vineyard transactions in the Cognac region, our observatory applies several filters: selection of plots registered as "vineyards" in the cadastre, cross-referencing with the INAO repository commune by commune, removal of atypical transactions. The median price, which represents the level at which half of the market is concluded, is our reference indicator.

The year 2020 covers only the second half. Mixed properties (vineyards + operating buildings + on-site distiller) are excluded when the value of the buildings represents a significant share. This last limitation is particularly important for Cognac: a significant number of estate sales with distillation facilities are conducted as part of overall operations that may not be correctly isolated by our method.

SAFER statistics, published by the Ministry of Agriculture, are based on a survey of notaries and a filter of transactions of more than half a hectare in a single block. They provide an annual average price with a remarkable historical depth (since 1991). For the Cognac vineyard, the two sources converge closely, a signal of market homogeneity.

| Vineyard | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Burgundy-Franche-Comté |

| Savoie | 57,216 | Savoie |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Jura |

| Beaujolais | 39,312 | Beaujolais |

| Cognac | 28,636 | Current article |

| Rhône Valle y | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Bordeaux |

| Roussillon | 13,918 | Languedoc-Roussillon |

| Languedoc | 13,531 | Languedoc-Roussillon |

| South-West | 9,205 | South-West |

The Cognac vineyard shows, over the 2020-2025 period, a contrasting profile: great stability until 2024 around a median price of €45,000-50,000/ha, followed by a marked inflection in 2025 with a 39% decline in the median. This correction reflects the market's adjustment to the cyclical deterioration of exports, particularly to China. Charente and Charente-Maritime, despite their appellation specificities, follow a similar trajectory. For buyers, 2025 opens a price window unseen in five years, but one that comes with uncertainty as to the depth and duration of the low cycle. Cognac's capacity to bounce back remains one of the most solid in the French wine sector. To go further, you can consult our vineyard listings category, our other articles on vineyard prices or download our white paper on creating a wine estate.