Last updated on May 18, 2026

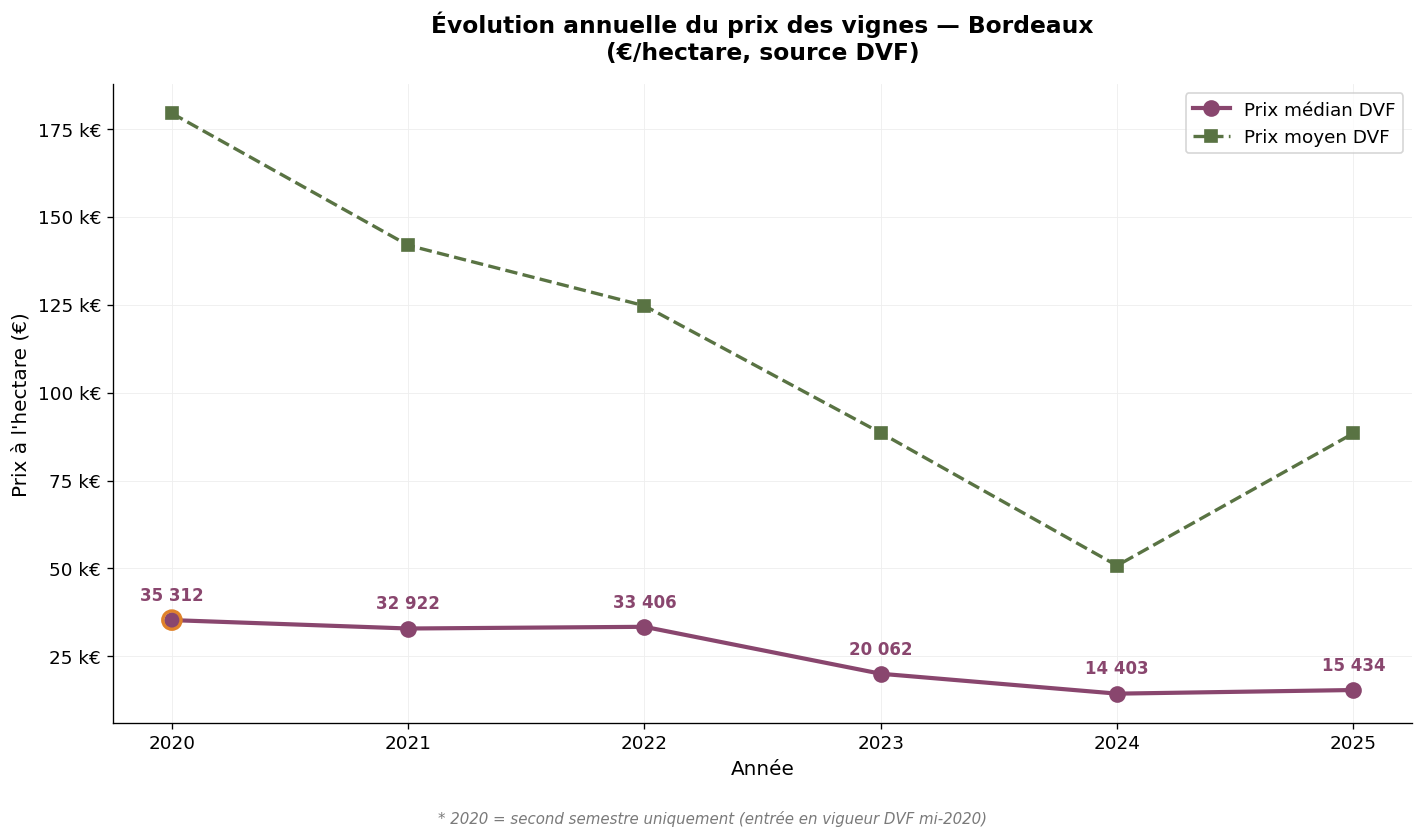

France's largest PDO vineyard by surface area, the Bordeaux wine region is going through a pivotal period. Between scheduled vine-pulling, declining bulk wine prices and a repositioning of supply, the land value of Gironde vineyards is evolving at a pace that deserves precise documentation. We propose here a detailed reading of vineyard prices in Bordeaux over the 2020-2025 period, based on DVF (Real Estate Value Requests) data and SAFER references. The year 2025, now closed, constitutes our reference year; the year 2024 provides the structural comparison point. The 2025 DVF median price stands at €15,434/ha, stabilising after a 56% decline over five years. Note: the DVF database was only activated in the second half of 2020, which makes that year partial. This article is part of our observatory of vineyard prices in France.

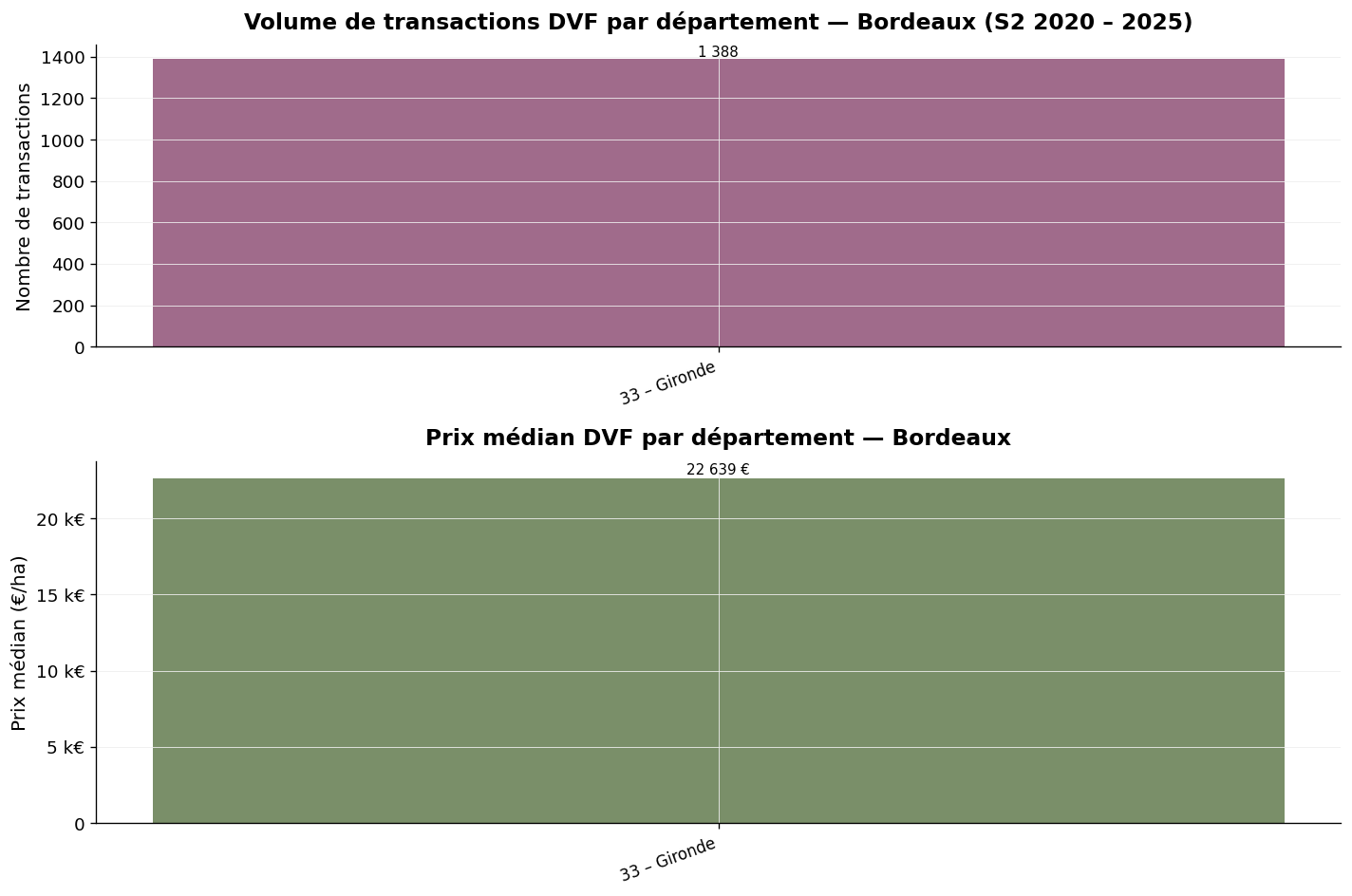

The Bordeaux vineyard is limited, in terms of appellations, to the Gironde (33) department. This is a unique feature among the major French wine-growing basins: a vineyard of approximately 105,000 hectares, organised around sixty-five appellations and structured by a historic wine trade. Land transactions there are dense and continuous, which allows the DVF database to offer a particularly fine-grained view of the market.

Our observatory has identified, after cleansing and cross-referencing with the INAO reference list, 1,388 vineyard transactions in Gironde over the H2 2020 – 2025 period. The average price stands at €110,193/ha and the median price at €22,639/ha. The gap between these two indicators — the average being nearly five times the median — reflects a polarisation of the Bordeaux market: alongside a broad base of plots transferred at modest prices, a few sales of prestigious growths strongly pull the average upwards.

The median price is, in this context, the indicator most representative of the current market: it represents the level at which half of the transactions are concluded. The average price, more sensitive to exceptional sales, reflects the market's amplitude. Reading these two indicators together is essential for correctly interpreting Bordeaux dynamics.

The annual evolution is eloquent. The table below summarises the main statistics by year.

| Year | Volume | Average price | Median price | Avg. surface (m²) |

|---|---|---|---|---|

| 2020 * | 165 | €179,389/ha | €35,312/ha | 16,701 |

| 2021 | 267 | €141,861/ha | €32,922/ha | 18,615 |

| 2022 | 294 | €124,673/ha | €33,406/ha | 17,622 |

| 2023 | 233 | €88,535/ha | €20,062/ha | 22,027 |

| 2024 | 259 | €50,809/ha | €14,403/ha | 22,190 |

| 2025 | 170 | €88,412/ha | €15,434/ha | 24,286 |

* 2020: second half only, DVF database activated mid-2020.

Evolution of median and average vineyard prices in Bordeaux — Source: DVF, processed by ma-propriete.fr

Reading the table and graph reveals a marked and continuous decline in the median price between 2020 and 2024: from €35,312/ha to €14,403/ha, a drop of nearly 60% in four complete financial years. The year 2025, now complete, stabilises the indicators at a historic low: median at €15,434/ha and average at €88,412/ha. The cumulative decline over five years is 56% on the median (from €35,312 to €15,434/ha) and the average has partially recovered in 2025 (vs €50,809/ha in 2024), reflecting the return of prestige transactions without reversing the general trend. The rise in the average in 2025 is partly due to the return of transactions involving prestigious properties (2025 maximum at €1,027,703/ha compared to €549,872/ha in 2024).

The evolution of the average transacted surface deserves specific comment. From an average of 1.67 hectares in 2020, it rose to 2.43 hectares in 2025, an increase of more than 45%. This increase reflects the appearance, on the market, of larger plots, a direct consequence of vine-pulling plans and the sale of estates in difficulty.

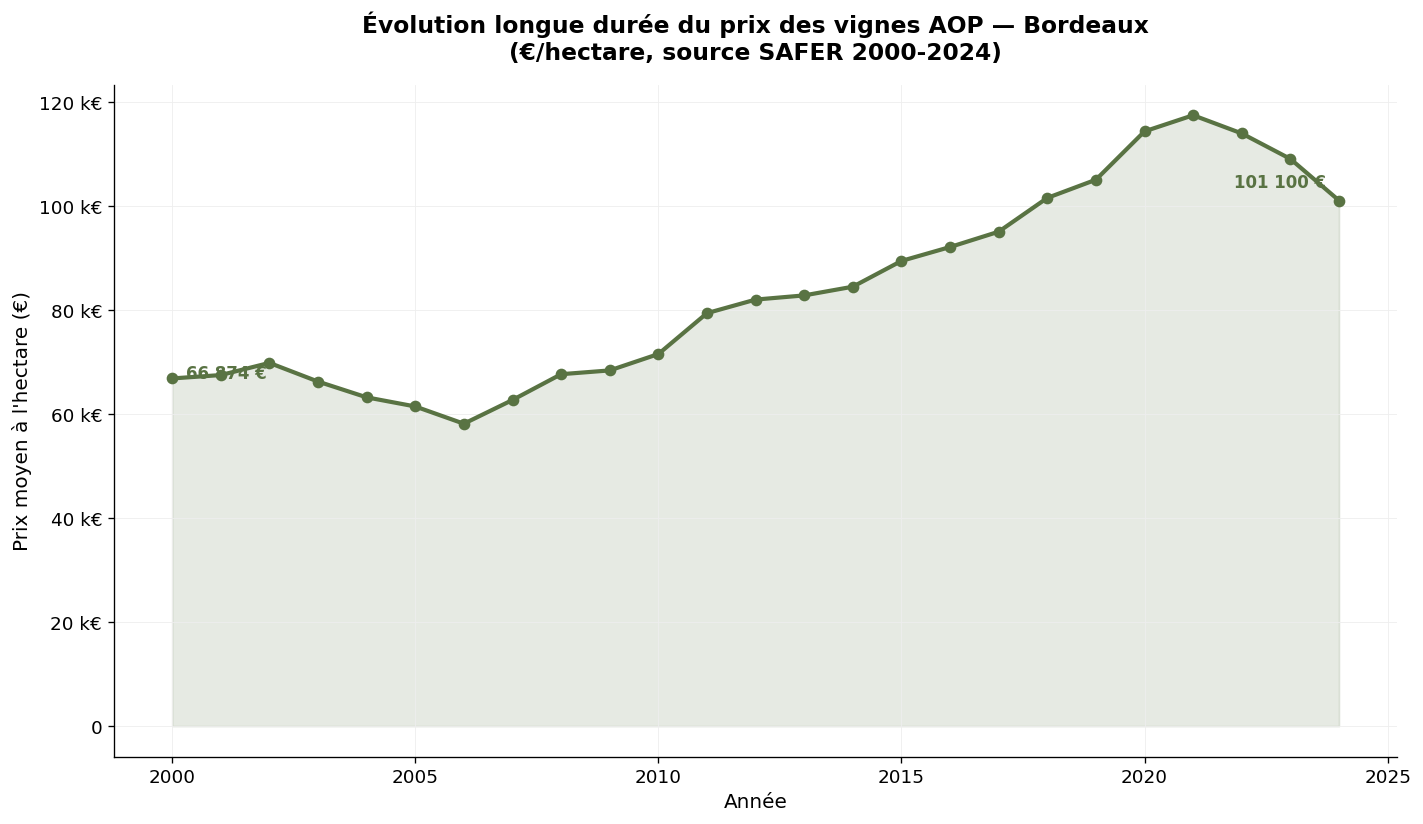

SAFER data, published annually by the Ministry of Agriculture, offers a long-term perspective — over nearly a quarter of a century — and constitutes the official reference for PDO vineyard land. For the Bordeaux-Aquitaine area, the evolution is as follows.

| Year | Average price (€/ha) | Annual evolution |

|---|---|---|

| 2000 | 66,874 | — |

| 2010 | 71,567 | + 7 % |

| 2015 | 89,477 | + 25 % |

| 2020 | 117,500 | + 31 % |

| 2022 | 109,100 | - 7 % |

| 2023 | 101,100 | - 7 % |

| 2024 | 117,000 | + 16 % |

Average price of Bordeaux-Aquitaine PDO vineyards — Source: SAFER / Ministry of Agriculture

The SAFER trajectory appears at first sight to diverge from the DVF: while the notarial database records a collapse in the median price since 2020, the 2024 SAFER average (€117,000/ha) remains close to the historic peak of 2020. This divergence is only apparent. It can be explained by three factors. First, SAFER aggregates a reduced sample of filtered transactions (notably block sales of more than half a hectare) and expresses a weighted average price that over-represents the most prestigious appellations. Conversely, the DVF includes all transfers, including the numerous small plots in generic PDOs. Second, the segments of the Bordeaux market evolve at radically different speeds. The classified growths segment resists, and even progresses — it is what structures the SAFER average. The generic and satellite PDO segment is collapsing — it is what weighs on the DVF median. Finally, SAFER smooths annual variations through its survey methodology, whereas the DVF reflects the actual transactional situation of the year.

Gironde concentrates all transactions of the Bordeaux vineyard. This singularity — a vineyard backed by a single department — makes the analysis particularly clear.

| Indicator | Gironde (33) |

|---|---|

| Total volume 2020-2025 | 1,388 transactions |

| Average price | €110,193/ha |

| Median price | €22,639/ha |

| Minimum observed | €4,376/ha |

| Maximum observed | €1,319,948/ha |

| Average surface | 2.01 ha |

Gironde — Transaction volume and median price, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

Detailed analysis of the Gironde market confirms the segment divergence mentioned above. Transactions range across a spectrum from €4,376/ha (plots in PDO Bordeaux or satellite, in low-value areas) to more than one million euros per hectare (classified growths of Médoc, Saint-Émilion, Pomerol). The median at €22,639/ha indicates that half of the market is concluded at relatively modest levels, with a marked decline since 2020.

This dynamic is part of a well-identified sector context. French consumption of still wine is declining structurally, exports are contracting in key markets (United States, China), and the profession has launched a subsidised vine-pulling plan covering several thousand hectares from 2023. The land market is progressively integrating these signals: discounting of less sought-after PDOs, weakened estates being put on the market, repositioning towards other agricultural uses or alternative productions.

For buyers, this context opens a window of opportunity. Values offered on the generic PDO segment are at a historic low, and market liquidity remains high (between 233 and 294 transactions per complete financial year). The largest sales now concern coherent operational units, conducive to the constitution or strengthening of an estate. To go further, you can consult our wine-growing category.

The amplitude observed in Bordeaux — from the minimum at €4,376/ha to the maximum above one million euros — is not a statistical artifact. It reflects the very structure of the vineyard, which combines, within the same administrative territory, radically different land markets.

The first segment, in volume, is that of generic Bordeaux and Bordeaux supérieur, which covers half the vineyard's surface. On this segment, prices are frequently concluded between €5,000 and €15,000/ha, sometimes less when the plot is isolated or when its replanting is considered uncertain. This segment is bearing the full brunt of the contraction of outlets.

The second segment groups together the communal and satellite appellations (Médoc, Haut-Médoc, Listrac, Moulis, Côtes de Bordeaux, Saint-Émilion satellites, Fronsac, etc.) where transactions are typically between €20,000 and €80,000/ha. Resistance varies according to the notoriety and quality of the terroirs.

The third segment, marginal in volume but structuring for the average, is that of the grand crus classés of Médoc, Saint-Émilion and Pomerol, where transactions can exceed one million euros per hectare. This segment is driven by patrimonial and international demand that remains dynamic. It represents a limited fraction of DVF transactions but explains the major gap between median and average.

This segmentation has a practical consequence for the buyer: a national or regional average price has no operational meaning for targeting a project. It is the targeted appellation, the quality of the terroirs and the valuation of bulk wine that determine the achievable land value upon resale. As an indication, on the basis of SAFER 2024 by major appellation category, the gap between a high-end Pessac-Léognan and a generic Bordeaux exceeds a factor of 20.

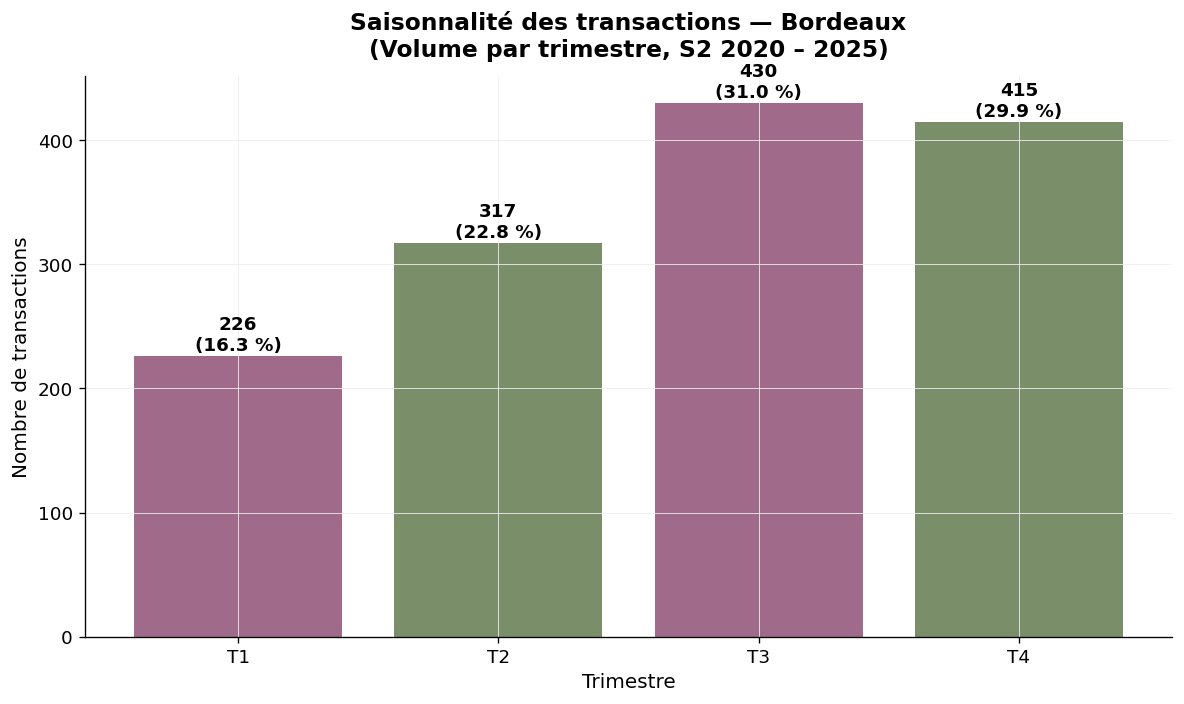

The distribution of transactions by quarter is enlightening. Q1 concentrates 226 sales (16.3%), Q2 317 sales (22.8%), Q3 430 sales (31.0%) and Q4 415 sales (29.9%). The concentration of the market in the second half — nearly 61% of transactions — confirms a classic calendar for vineyard land: schedule freed up after the harvest, accounting and tax organisation of sellers at year-end, and notarial processing time that pushes a significant portion of preliminary contracts signed in summer to the end of the year.

Seasonality — Bordeaux, volume by quarter — Source: DVF, processed by ma-propriete.fr

For a buyer, knowledge of this seasonality has practical implications: the first half-year, structurally less competitive, often offers better negotiation conditions, whereas the fourth quarter concentrates transactions with fiscal stakes for the seller. Beyond this calendar, the 2025 dynamic deserves particular attention. Over the full financial year, 170 transactions were recorded, a pace consistent with previous years. The maintenance of volumes testifies to preserved liquidity in the Bordeaux market.

The DVF database (Real Estate Value Requests) lists all real estate transfers for valuable consideration registered by the DGFiP since 2014. To isolate vineyard transactions, our observatory applies several successive filters: selection of plots cadastrally registered as "vineyards", cross-referencing with the INAO reference list commune by commune to link each plot to its appellation, elimination of atypical transactions (mixed properties combining housing + vineyards, intra-family sales at convenience prices, transfers to companies). The final perimeter covers nearly 17,600 vineyard transactions between the second half of 2020 and the end of 2025. For each vineyard, we publish the average price, the median price, the extreme values and the average transacted surface.

Three precautions must be taken. The year 2020 only covers the second half, which makes it a partial reference. Mixed properties (vineyards + operational buildings) are excluded from our perimeter. Finally, the Alsace-Moselle departments are not covered by the DVF database due to the land registry regime.

SAFER statistics are based on a survey of notaries and a filtering of block transactions of more than half a hectare. They provide an annual average price over a remarkable historical depth (since 1991). Our DVF approach complements this view by providing a median price and fine granularity.

The comparative table below repositions Bordeaux within the national hierarchy of 2024 median DVF prices. Champagne occupies a place apart. Burgundy and Provence are above the national median. Bordeaux, the Loire Valley, Languedoc-Roussillon, the South-West and the Rhône Valley form a group where the median remains contained.

| Vineyard | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Burgundy-Franche-Comté |

| Savoie | 57,216 | Savoie |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Jura |

| Beaujolais | 39,312 | Beaujolais |

| Cognac | 28,636 | Cognac |

| Rhône Valley | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Current article |

| Roussillon | 13,918 | Languedoc-Roussillon |

| Languedoc | 13,531 | Languedoc-Roussillon |

| South-West | 9,205 | South-West |

The Bordeaux vineyard market is going through a marked phase of land transition. The DVF median price has lost nearly 60% between 2020 and 2024, reflecting the decline of generic PDOs in a context of overproduction and contraction of outlets. The year 2025, complete and now robust, confirms the stabilisation at a low point, without any sign of a general recovery. The high-end segment (classified growths) remains, for its part, supported — but represents a very small fraction of transactions. For buyers with a structured project, the situation opens up acquisition opportunities at levels not seen for fifteen years. To deepen the comparative analysis by vineyard, you can consult the other articles in our series on vineyard prices in France or download our white paper on creating a wine estate.