Last updated on 19 May 2026

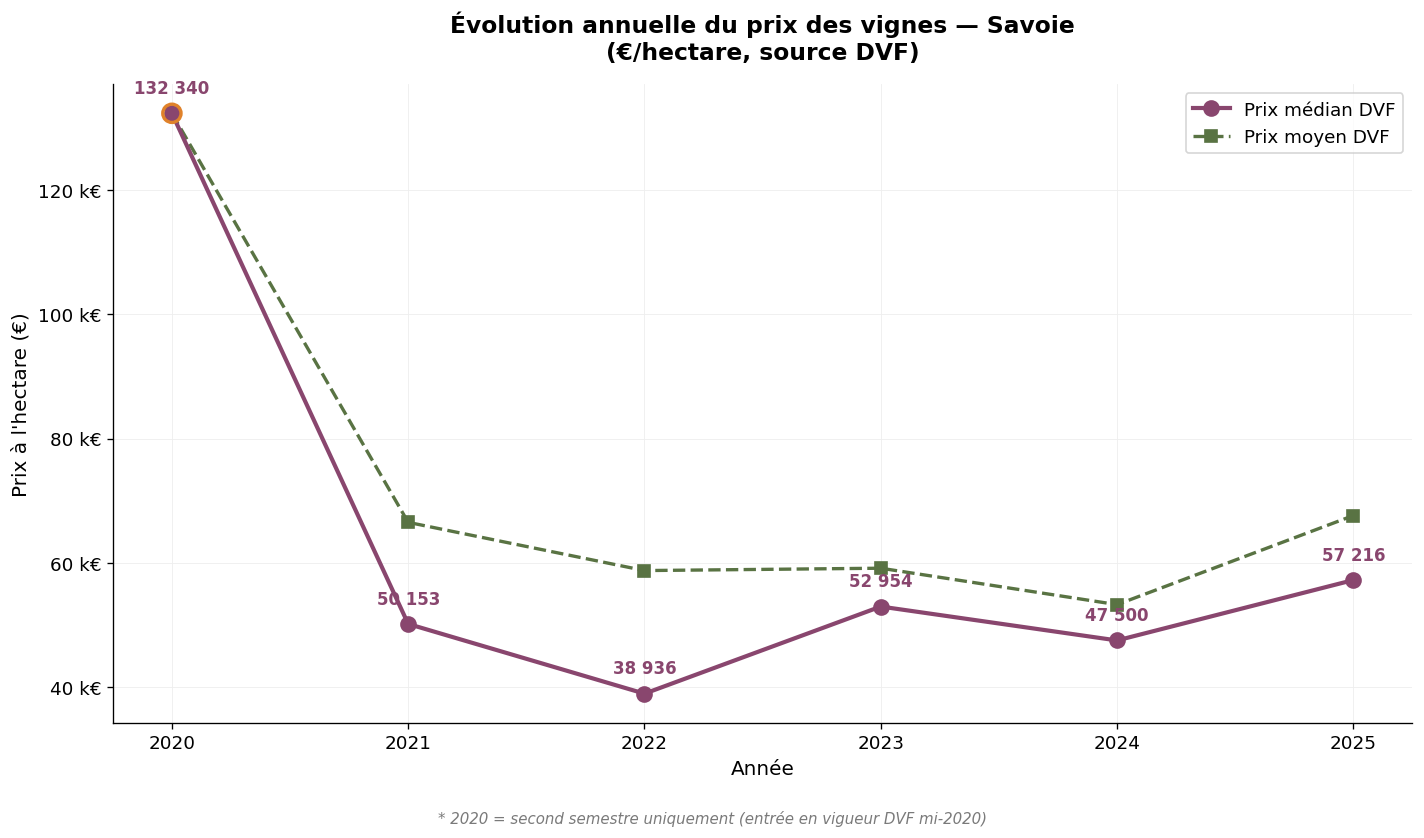

The Savoie vineyard is one of the smallest AOP vineyards in France — around 2,200 hectares planted — but also one of the most distinctive, built on native grape varieties (jacquère, altesse, mondeuse, persan) and closely tied to the mountain and tourist identity of its territory. The vineyard land market here is limited but dynamic, supported by heritage and tourist pressure. We analyse here the price of vineyards in Savoie over the 2020-2025 period, based on DVF data (Demandes de Valeurs Foncières — French land transaction records) and SAFER references. The 2025 figures, now complete, serve as our main reference year; the 2024 figures provide a robust basis for comparison. The 2025 DVF median price reaches €57,216/ha, showing marked growth since 2022 (+47%). Note: the year 2020 only covers the second half. This article is part of our observatory of vineyard prices in France.

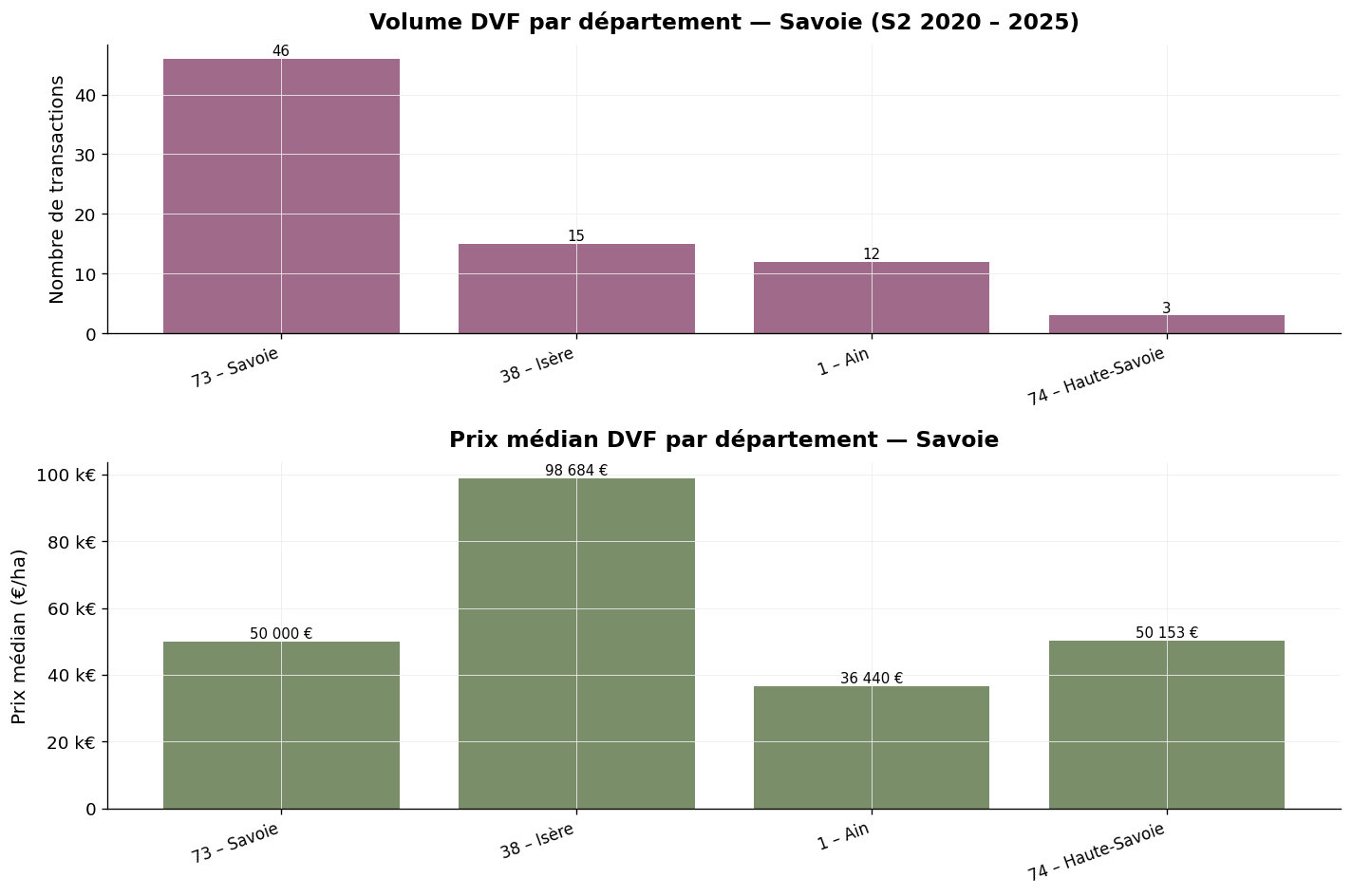

The Savoyard vineyard spans four departments: Savoie (73), which covers the majority of the vineyard (around Lake Bourget, in the Combe de Savoie and the Chambéry basin), Isère (38) for the part of the Vin de Savoie AOC located in the foothills of Grenoble, Ain (1) for the Bugey and Roussette du Bugey AOC enclaves, and more marginally Haute-Savoie (74) for the vineyards of the Lake Geneva Chablais area. The vineyard is organised around several AOCs: Vin de Savoie (and its geographical designations Apremont, Abymes, Chignin, Chignin-Bergeron, Arbin, Jongieux, Cruet, Saint-Jean-de-la-Porte, Chautagne, Crépy, Marin, Marignan, Ripaille), Roussette de Savoie, Crémant de Savoie, Seyssel, Bugey, Roussette du Bugey.

Over the H2 2020 – 2025 period, our observatory has identified 76 vineyard transactions in wine-growing Savoie, making it one of the least liquid markets in France. The average price stands at €61,915/ha and the median price at €50,000/ha. The gap between the average and the median (1.24×) reflects relative moderation, despite the presence of a few exceptional transactions. The maximum observed (€253,659/ha) corresponds to emblematic plots in the Roussette de Savoie AOC or near tourist areas.

| Year | Volume | Average price | Median price | Avg. area (m²) |

|---|---|---|---|---|

| 2020 * | 2 | €132,340/ha | €132,340/ha | 2,850 |

| 2021 | 9 | €66,507/ha | €50,153/ha | 10,805 |

| 2022 | 23 | €58,746/ha | €38,936/ha | 4,850 |

| 2023 | 14 | €59,125/ha | €52,954/ha | 5,178 |

| 2024 | 16 | €53,264/ha | €47,500/ha | 3,861 |

| 2025 | 12 | €67,599/ha | €57,216/ha | 5,766 |

* 2020: second half only (2 transactions, to be interpreted with caution).

Annual price trend from DVF — Savoie — Source: DVF, processed by ma-propriete.fr

The trajectory has been upward since 2022, with a low of €38,936/ha that year, followed by a gradual rise to €57,216/ha in 2025 (+47% in three years). This dynamic reflects both the scarcity of land in the Savoyard vineyard, the growing interest in Alpine grape varieties, and the heritage-tourist pressure sustained by ski resort traffic and the development of Alpine wine tourism. The low volume (76 transactions over six years) nonetheless calls for cautious interpretation: the annual median is sensitive to the transaction mix on small samples.

The average transaction area is one of the smallest in France (between 4,000 and 11,000 m² depending on the year), a structural feature of a fragmented vineyard largely organised around small family farms.

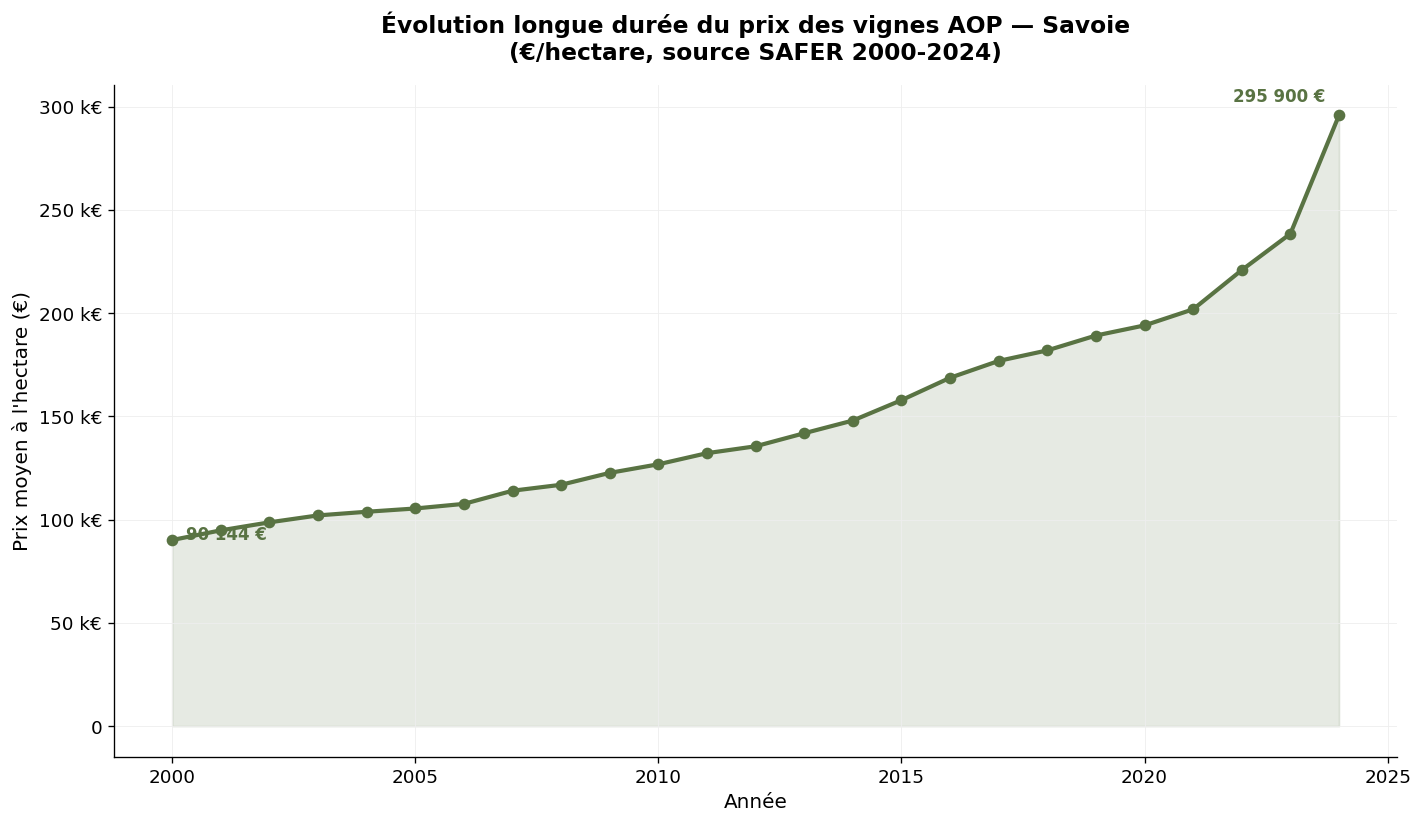

SAFER does not publish a specific statistic for Savoie: this vineyard is integrated into the "Burgundy-Beaujolais-Savoie-Jura" group. The figures below, to be interpreted as indicative, reflect the dynamics of this broader group.

| Year | Average price (€/ha) | 5-year change |

|---|---|---|

| 2000 | 90,144 | — |

| 2010 | 126,832 | + 41% |

| 2020 | 201,900 | + 59% |

| 2024 | 295,900 | + 47% |

SAFER average price for Burgundy-Beaujolais-Savoie-Jura AOP vineyards — Source: Ministry of Agriculture / SAFER

The aggregated SAFER trend is not representative of Savoie alone: the average is pulled up by Burgundy, whose levels far exceed those of Savoie. For Savoie alone, the 2024 SAFER average can be estimated at a level consistent with the observed DVF average, i.e. around €50,000-65,000/ha.

Volume and median price by department — wine-growing Savoie, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

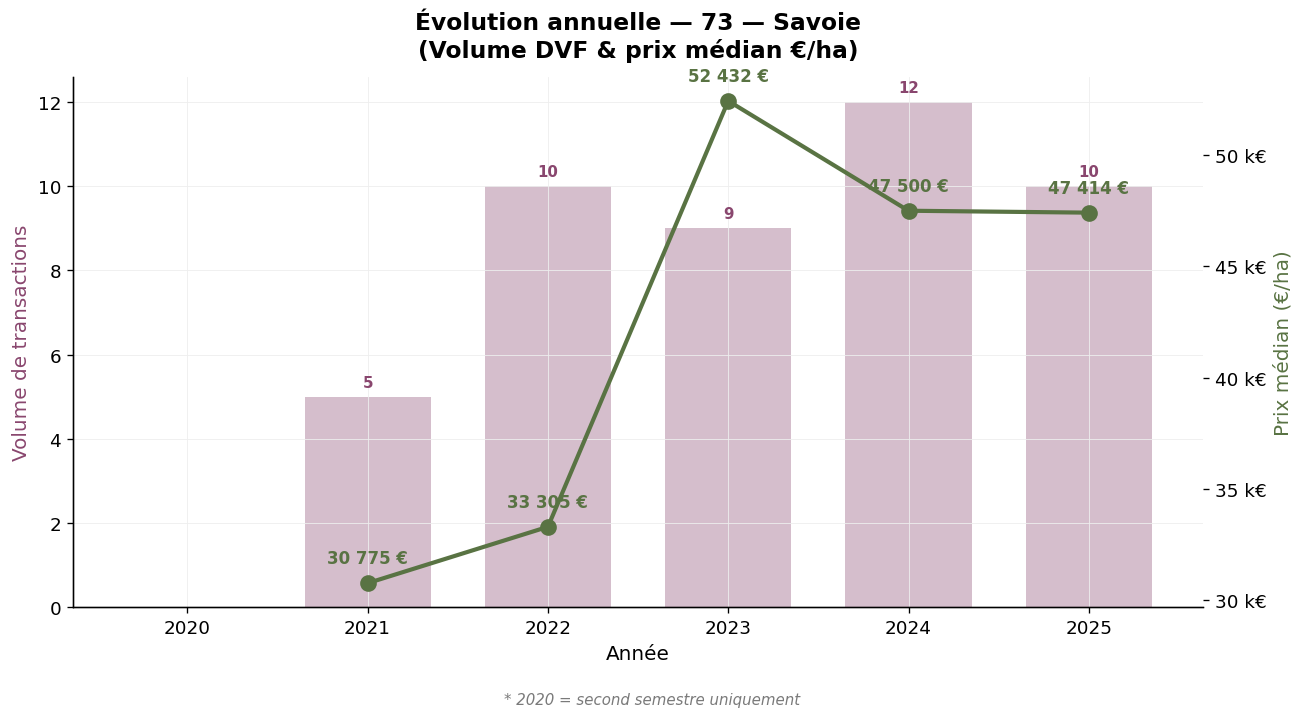

The historic heart of the vineyard (46 transactions), the Savoie department shows an average price of €48,240/ha and a median of €50,000/ha. The average area (5,867 m²) is typical of a vineyard fragmented into family plots. The department covers the main geographical designations of the Vin de Savoie AOC (Apremont, Abymes, Chignin, Chignin-Bergeron, Arbin, Jongieux, Cruet, Chautagne) as well as the best plots of Roussette de Savoie.

Savoie (73) — Annual trend — Source: DVF, processed by ma-propriete.fr

Isère covers the part of the Vin de Savoie AOC located in the foothills of Grenoble (Saint-Jean-de-la-Porte on the Savoie side lies just on the border). 15 transactions over the period, median price €98,684/ha, average price €123,940/ha. These levels, significantly higher than those of Savoie, reflect the scarcity of land in this narrow perimeter and the heritage-tourist pressure linked to the proximity of Grenoble. The average area (2,090 m²) is very small.

Ain covers the Bugey and Roussette du Bugey AOCs, in the south of the department (around Belley and Cerdon). 12 transactions over the period, median price €36,440/ha, average price €39,735/ha. Levels are contained, reflecting a less well-known vineyard and a less stretched market. The average area (6,104 m²) is consistent with Alpine practices.

Haute-Savoie covers the rare vineyards of the Lake Geneva Chablais area (Crépy, Marignan, Marin, Ripaille). 3 transactions over the period, median price €50,153/ha. The low volume calls for cautious interpretation.

Wine-growing Savoie presents a specific market profile. The modest size of the vineyard (2,200 hectares), the rarity of sales and the heritage-tourist pressure converge to support price levels higher than what agricultural economics alone would justify. The proximity of ski resorts and major Alpine cities (Annecy, Chambéry, Grenoble) creates lasting heritage demand. For buyers, Savoie therefore offers a niche market, with low liquidity, where it is essential to position oneself on opportunities as they arise.

The diversity of native grape varieties (jacquère, altesse, mondeuse, persan, gringet) and the specificity of mountain terroirs also constitute a particularly interesting differentiation lever at a time when consumption is shifting towards identity-driven wines, expressive of their terroirs and stemming from sustainable viticulture. Organic and biodynamic conversion is progressing rapidly in the Savoyard vineyard.

The seasonality of Savoyard transactions shows a concentration in the first half of the year: Q1 27.6%, Q2 26.3%, Q3 27.6%, Q4 18.4%. This relatively balanced distribution, without marked year-end concentration, reflects a market where heritage and tourism-driven operations weigh more heavily than accounting-related year-end considerations.

Seasonality — wine-growing Savoie, volume by quarter — Source: DVF, processed by ma-propriete.fr

The DVF database lists all property transfers for valuable consideration recorded by the DGFiP (French tax authority). To isolate vineyard transactions in wine-growing Savoie, our observatory applies several filters: selection of plots registered as "vineyards" in the land registry, cross-referencing with the INAO reference database commune by commune, and elimination of atypical transactions.

The year 2020 only covers the second half. The low volume of the vineyard (76 transactions over six years) calls for cautious interpretation, particularly at the departmental level or for departments with very low volume (Haute-Savoie, Ain). Mixed properties (vineyards + farm buildings) are excluded when the value of the buildings represents a significant share.

SAFER aggregates Savoie with Burgundy, Beaujolais and Jura, which limits its usefulness for a specific analysis. Our DVF approach complements this view by isolating wine-growing Savoie alone.

| Vineyard | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Burgundy-Franche-Comté |

| Savoie | 57,216 | Current article |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Jura |

| Beaujolais | 39,312 | Beaujolais |

| Cognac | 28,636 | Cognac |

| Rhône Valley | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Bordeaux |

| Roussillon | 13,918 | Languedoc-Roussillon |

| Languedoc | 13,531 | Languedoc-Roussillon |

| South-West | 9,205 | South-West |

Over the 2020-2025 period, wine-growing Savoie offers a niche land market with a unique profile: low transaction volume, median price around €47,500-57,000/ha, and an upward trajectory supported by land scarcity and heritage-tourist pressure. The diversity of AOCs, the specificity of Alpine grape varieties and the growing interest in identity-driven wines support medium-term revaluation potential. For buyers, Savoie represents an original heritage entry point, provided one accepts the low liquidity of the market and seizes opportunities as they arise. To go further, you can consult our winegrowing property listings category, our other articles on vineyard prices or download our white paper on creating a wine estate.