Updated on May 18, 2026

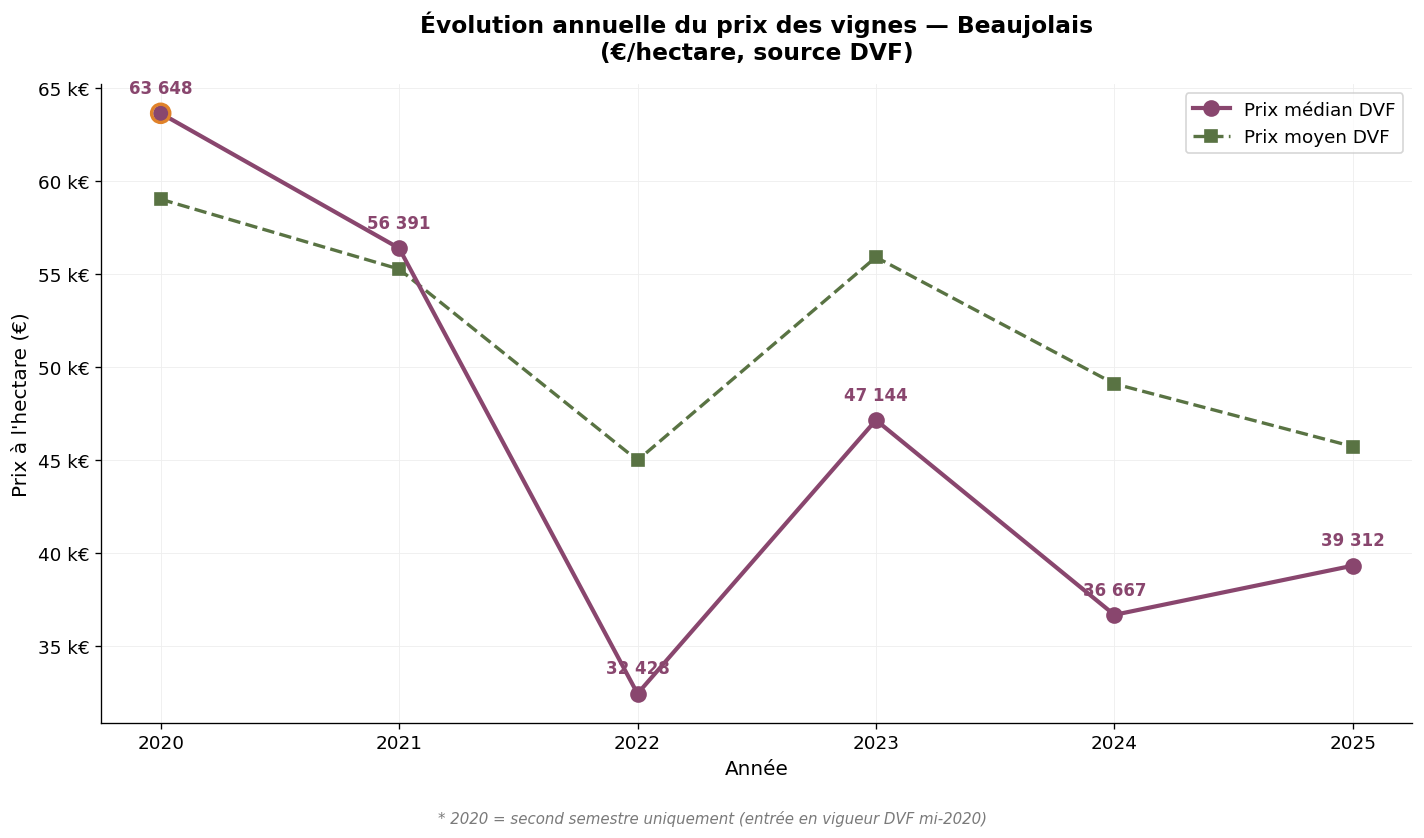

The Beaujolais vineyard occupies a unique position in the French wine landscape: built around a single red grape variety (gamay noir) and structured around twelve appellations (the regional Beaujolais AOC, the Beaujolais-Villages AOC and the ten Beaujolais crus), it has experienced several cycles of growth and decline over the past two decades. Today, the region is once again attracting buyers seeking estates with strong revaluation potential. We analyze here the price of vineyard land in Beaujolais over the 2020-2025 period, based on DVF data (Land Value Requests) and SAFER references. The 2025 figures, now complete, constitute our main reference year; the 2024 figures provide a robust comparison base. The median 2025 DVF price stands at €39,312/ha, sharply down from the 2020 peak but with a slight rebound compared to 2024. Note: the year 2020 only covers the second half. This article is part of our observatory of vineyard prices in France.

The Beaujolais vineyard covers approximately 14,500 hectares planted in AOC, divided between the Rhône department (69) — which covers most of the vineyard — and the south of Saône-et-Loire (71) for the municipalities classified in AOC Beaujolais. The hierarchy of appellations is clear: Beaujolais and Beaujolais Nouveau at the bottom, Beaujolais-Villages in the middle, and at the top the ten Beaujolais crus (Brouilly, Côte-de-Brouilly, Chénas, Chiroubles, Fleurie, Juliénas, Morgon, Moulin-à-Vent, Régnié and Saint-Amour), each with its terroir specificities.

Over the H2 2020 – 2025 period, our observatory recorded 959 vineyard transactions in Beaujolais (INAO cross-referencing applied municipality by municipality to distinguish AOC Beaujolais transactions from AOC Bourgogne transactions in Saône-et-Loire). The average price stands at €51,013/ha and the median price at €42,197/ha. The proximity between average and median (1.21×) reflects a relatively homogeneous market, without the extreme polarization observed in Bordeaux or Burgundy.

| Year | Volume | Average price | Median price | Avg. area (sqm) |

|---|---|---|---|---|

| 2020 * | 82 | €59,027/ha | €63,648/ha | 9,037 |

| 2021 | 184 | €55,268/ha | €56,391/ha | 11,719 |

| 2022 | 190 | €44,981/ha | €32,428/ha | 10,626 |

| 2023 | 174 | €55,909/ha | €47,144/ha | 9,770 |

| 2024 | 176 | €49,098/ha | €36,667/ha | 8,179 |

| 2025 | 153 | €45,722/ha | €39,312/ha | 10,397 |

* 2020: second half only.

Annual evolution of DVF prices — Beaujolais — Source: DVF, processed by ma-propriete.fr

The trajectory is overall downward over the period. The median price fell from €63,648/ha in 2020 to €39,312/ha in 2025, a decline of 38% over five years, with a marked low in 2022 (€32,428/ha). This evolution is part of the context of persistent tensions on bulk Beaujolais prices and the wait-and-see attitude observed since 2022. The partial rebound in 2023 (median €47,144/ha) was not confirmed in 2024 and 2025. The average, more stable, fluctuates around €45,000-55,000/ha, indicating that exceptional transactions on the crus (Moulin-à-Vent, Fleurie, Morgon) maintain a floor.

The average area transacted (around 10,000 sqm) is typical of a vineyard where estate-sized operations remain dominant, but parcel-by-parcel transfers represent a significant share of sales. The transaction volume remains high and stable at around 170-190 per year, indicating good market liquidity.

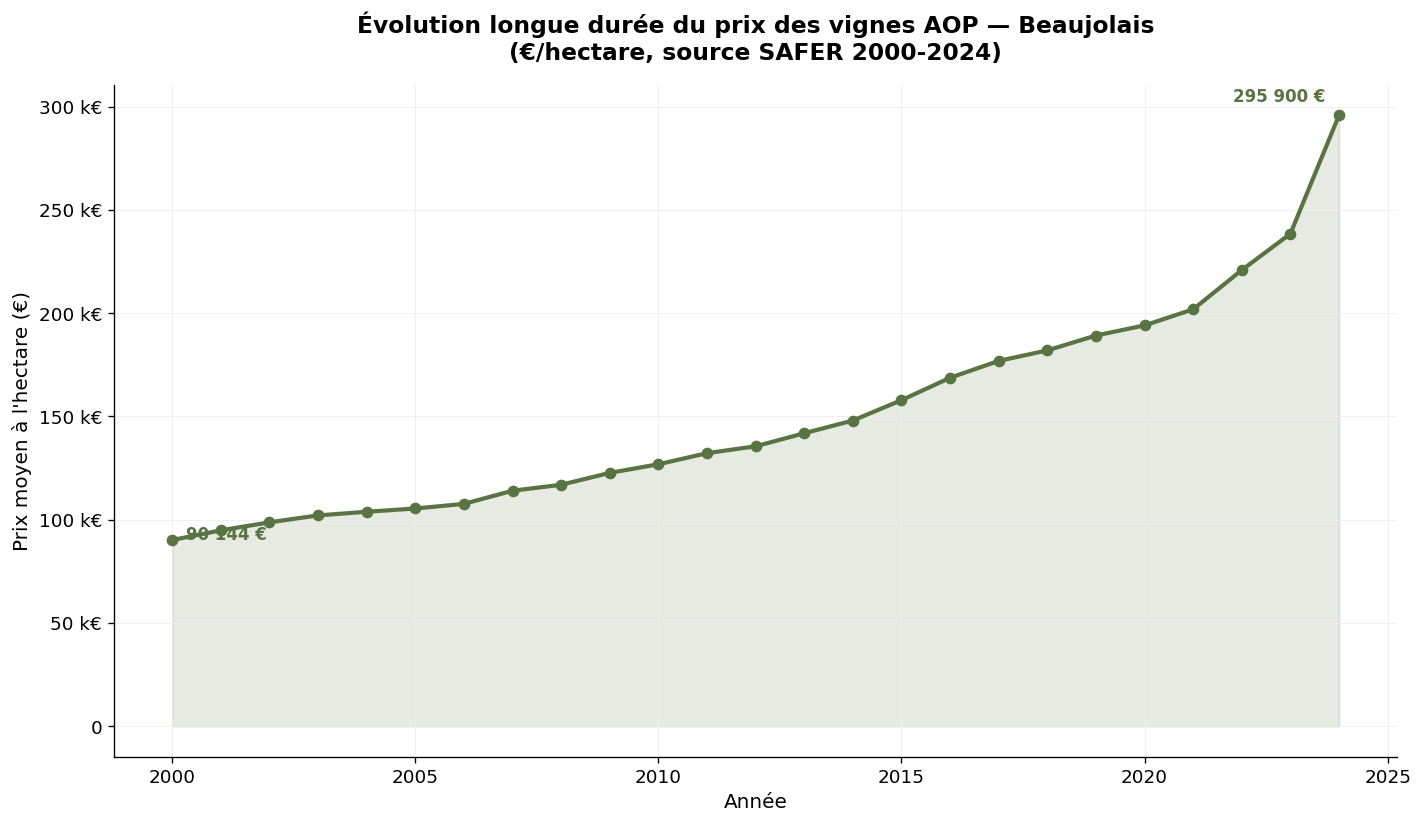

SAFER does not publish specific statistics for Beaujolais: this vineyard is included in the "Burgundy-Beaujolais-Savoie-Jura" aggregate. The figures below therefore reflect the dynamics of this broader group, in which Burgundy weighs heavily.

| Year | Average price (€/ha) | 5-year evolution |

|---|---|---|

| 2000 | 90,144 | — |

| 2010 | 126,832 | + 41% |

| 2020 | 201,900 | + 59% |

| 2024 | 295,900 | + 47% |

SAFER average price of AOP Burgundy-Beaujolais-Savoie-Jura vineyards — Source: Ministry of Agriculture / SAFER

The aggregated SAFER evolution masks the specific trajectory of Beaujolais: the overall progression is indeed driven by Burgundy, whose levels are far higher. For Beaujolais alone, the 2024 SAFER average can be estimated at around €50,000-65,000/ha, a level consistent with the DVF average observed (€49,098/ha in 2024).

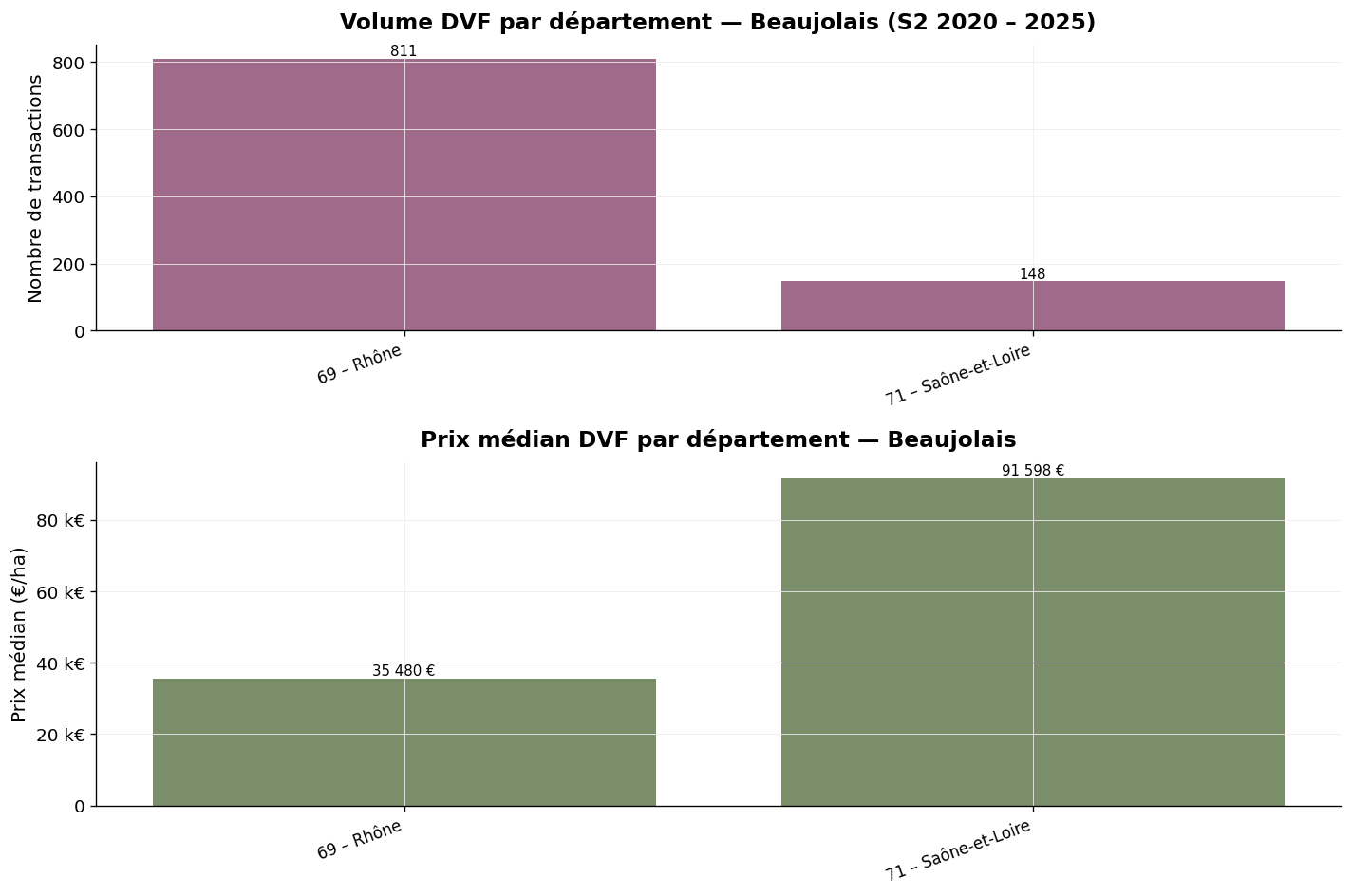

Volume and median price by department — Beaujolais, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

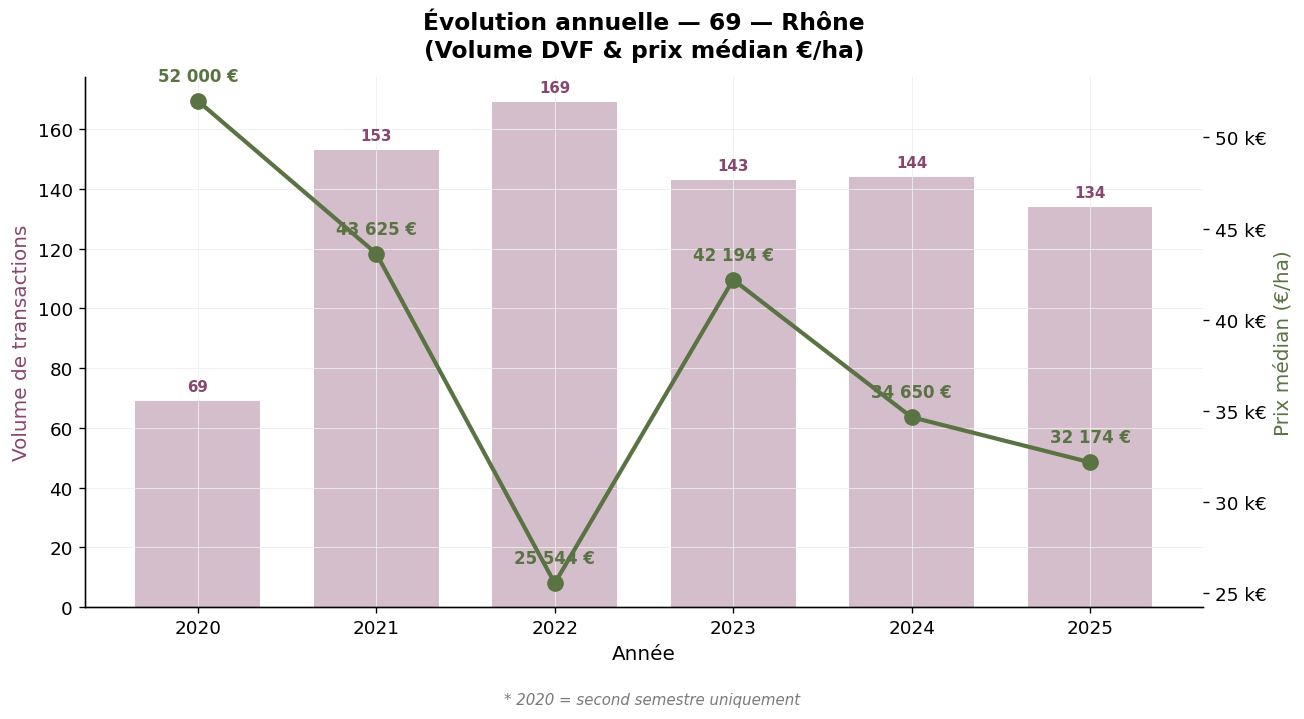

The Rhône department concentrates almost all of the Beaujolais vineyard: 811 transactions over the period, average price €44,634/ha, median price €35,480/ha. The average area (10,637 sqm) is consistent with regional practices. The department covers all the crus (Brouilly, Côte-de-Brouilly, Chénas, Chiroubles, Fleurie, Juliénas, Morgon, Moulin-à-Vent, Régnié, Saint-Amour) and most of the AOC Beaujolais and Beaujolais-Villages. The maximum observed (€350,000/ha) corresponds to emblematic parcels in Moulin-à-Vent or Fleurie.

Rhône (69) — AOC Beaujolais area — Annual evolution — Source: DVF, processed by ma-propriete.fr

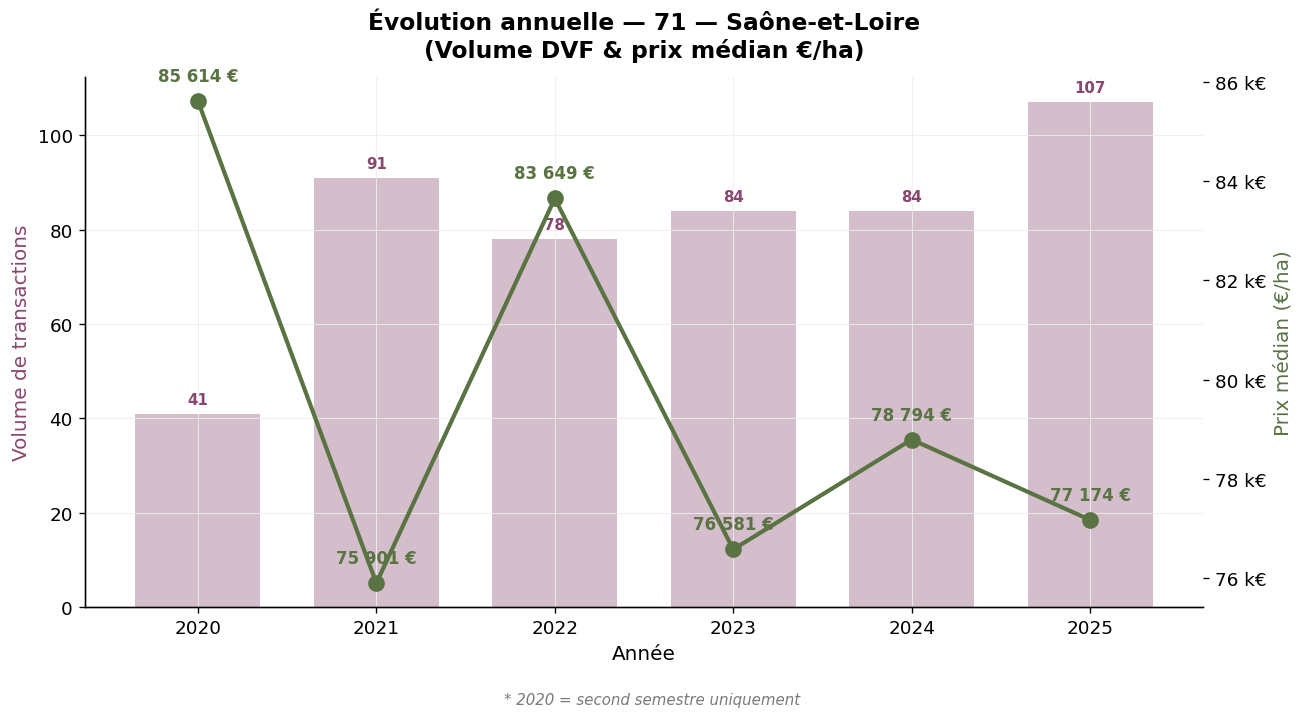

The southern part of Saône-et-Loire is attached to the Beaujolais vineyard for municipalities classified as AOC Beaujolais or Saint-Amour. Our observatory records 148 transactions over the period, for an average price of €85,963/ha and a median of €91,598/ha. These levels, significantly higher than the Rhône AOC Beaujolais average, reflect both the scarcity of transactions (low number of municipalities concerned) and the quality of the Saint-Amour terroirs, one of the northernmost crus of Beaujolais. The average area (6,892 sqm) is smaller than in Rhône.

Saône-et-Loire (71) — AOC Beaujolais area — Annual evolution — Source: DVF, processed by ma-propriete.fr

Beyond the departmental reading, Beaujolais is characterized by a three-tier hierarchy of appellations that strongly determines land values. The regional Beaujolais AOC, which notably produces Beaujolais Nouveau, displays the most modest values, typically between €5,000 and €20,000/ha. The Beaujolais-Villages AOC, covering 38 municipalities in the north of the vineyard, lies between €15,000 and €40,000/ha. The ten Beaujolais crus (Brouilly, Côte-de-Brouilly, Chénas, Chiroubles, Fleurie, Juliénas, Morgon, Moulin-à-Vent, Régnié, Saint-Amour) constitute the top, with values ranging from €40,000 to €350,000/ha depending on the reputation and quality of the terroirs.

This hierarchy is in motion. The qualitative repositioning of Beaujolais begun since the early 2010s — installation of young winemakers, massive organic conversion, rising reputation of single-parcel cuvées — sustainably supports the land value of the best crus, while the regional base suffers from the wait-and-see attitude of the market. For buyers, Beaujolais therefore offers a range of strategies: economic operation on regional Beaujolais, qualitative repositioning in Beaujolais-Villages, heritage project in a cru.

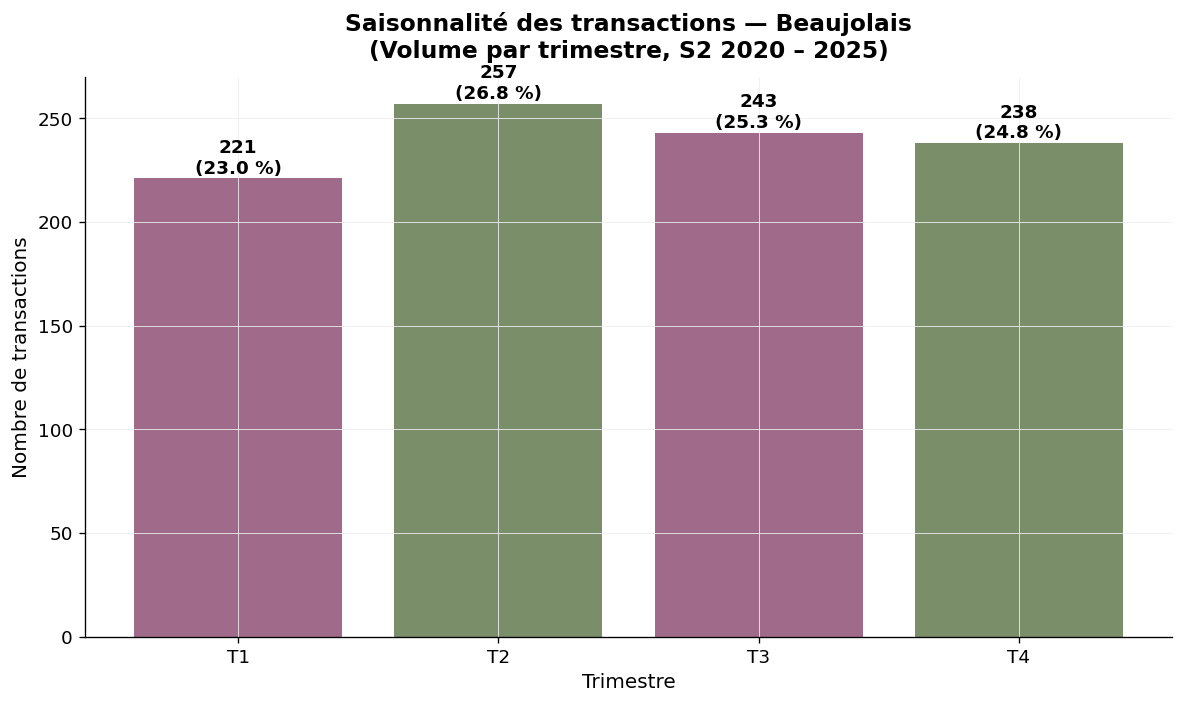

The seasonality of transactions in Beaujolais is relatively balanced: Q1 23.0%, Q2 26.8%, Q3 25.3%, Q4 24.8%. This very flat distribution, compared to the year-end concentration observed in Bordeaux or Cognac, reflects a continuous market, little affected by tax calendars.

Seasonality — Beaujolais, volume by quarter — Source: DVF, processed by ma-propriete.fr

The DVF database lists all paid real estate transfers registered by the DGFiP. To isolate Beaujolais vineyard transactions from this database, our observatory applies several filters: selection of parcels registered as "vineyards", cross-referencing with the INAO repository municipality by municipality (notably to distinguish in Saône-et-Loire AOC Beaujolais transactions from AOC Bourgogne transactions), elimination of atypical transactions.

The year 2020 only covers the second half. Mixed properties (vineyards + farm buildings) are excluded when the value of the buildings represents a significant share. The distinction between the regional Beaujolais AOC, Beaujolais-Villages and the ten crus cannot be made directly in the DVF database: the published statistics aggregate the three levels of appellation.

SAFER aggregates Beaujolais with Burgundy, Savoie and Jura, which limits its usefulness for specific analysis. Our DVF approach complements this view by isolating Beaujolais alone and providing a median price.

| Vineyard | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Burgundy-Franche-Comté |

| Savoie | 57,216 | Savoie |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Jura |

| Beaujolais | 39,312 | Current article |

| Cognac | 28,636 | Cognac |

| Rhône Valley | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Bordeaux |

| Roussillon | 13,918 | Languedoc-Roussillon |

| Languedoc | 13,531 | Languedoc-Roussillon |

| South-West | 9,205 | South-West |

Beaujolais offers, over the 2020-2025 period, a vineyard land market in decline but with strong heritage potential. The median DVF price lost nearly 40% between 2020 and 2025, reflecting the adjustment to bulk price conditions, while exceptional transactions on the crus maintain a stable average. The Rhône department concentrates most of the activity; the southern Saône-et-Loire area (Saint-Amour) offers higher values for a limited number of sales. For buyers, the situation opens up acquisition opportunities at historically low levels, particularly on Beaujolais and Beaujolais-Villages. The qualitative repositioning undertaken by the profession supports a medium-term revaluation potential on the best terroirs and well-positioned estates. To go further, you can consult our wine-growing listings category, our other articles on vineyard prices or download our white paper dedicated to creating a wine estate.