Last updated on 19 May 2026

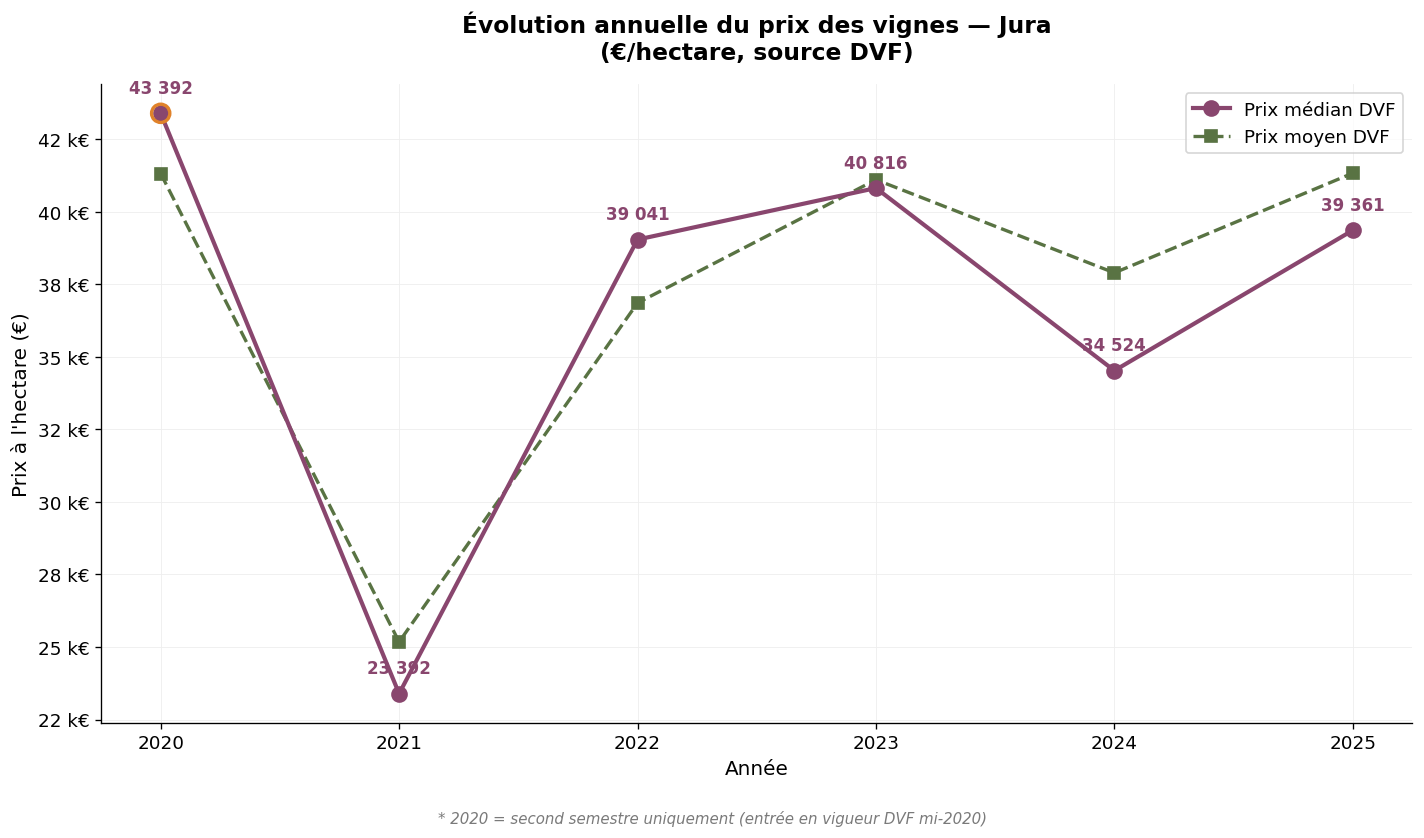

The Jura vineyard is one of the smallest French AOP wine regions — approximately 1,800 planted hectares — yet one of the most distinctive and dynamic. Built around indigenous grape varieties (savagnin, poulsard, trousseau) and varieties shared with Burgundy (chardonnay, pinot noir), it produces a remarkable diversity of wines: straw wines, yellow wines, crémants, and still wines. The quality renaissance that began in the early 2000s, and the international critical acclaim that followed, have underpinned a rising trajectory for vineyard land values. Here we analyse the price of vineyard land in the Jura over the 2020–2025 period, drawing on DVF (Demandes de Valeurs Foncières) data and SAFER benchmarks. The 2025 figures, now complete, constitute our primary reference year; the 2024 figures provide a robust basis for comparison. The 2025 DVF median price stands at €39,361/ha, on a continuous upward trend since 2021 (+68% in four years). Note: 2020 covers the second half only. This article is part of our observatory of vineyard prices in France.

The Jura vineyard is entirely contained within the Jura department (39). It is organised around four geographical AOCs (Arbois, l'Étoile, Château-Chalon, Côtes du Jura) and several product AOCs (Crémant du Jura, Macvin du Jura, Marc du Jura), totalling approximately 1,800 planted hectares. This small size makes the Jura a niche market — illiquid, but with strong heritage investment potential.

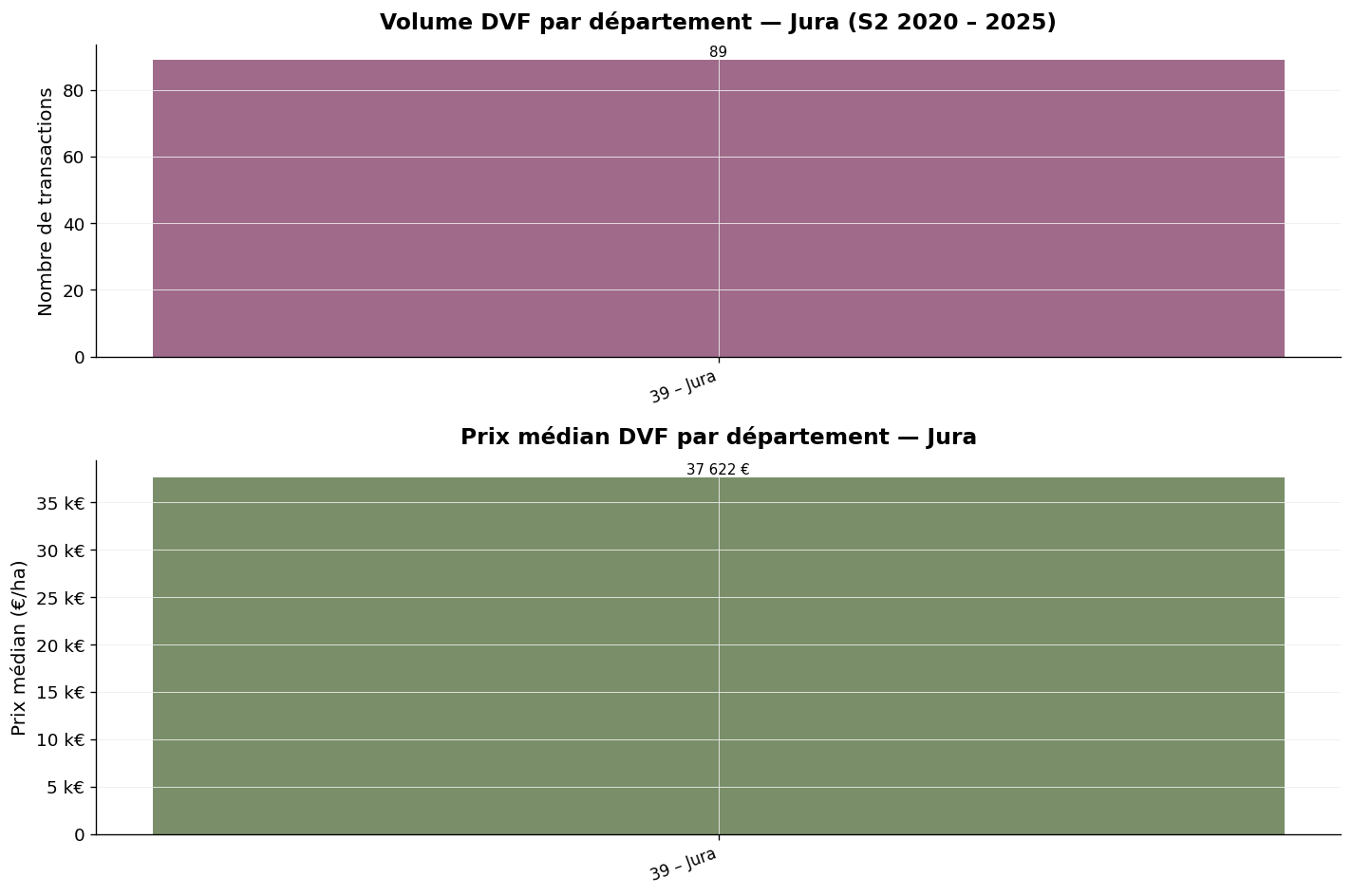

Over the period H2 2020–2025, our observatory recorded 89 vineyard transactions in the Jura. The average price stands at €37,820/ha and the median price at €37,622/ha. The near-perfect alignment between mean and median (1.005×) reflects the remarkable homogeneity of the Jura market: few exceptional transactions, little dispersion, a market anchored to its central values.

| Year | Volume | Average price | Median price | Avg. area (m²) |

|---|---|---|---|---|

| 2020 * | 8 | €41,316/ha | €43,392/ha | 15,548 |

| 2021 | 11 | €25,176/ha | €23,392/ha | 11,265 |

| 2022 | 15 | €36,857/ha | €39,041/ha | 6,838 |

| 2023 | 25 | €41,105/ha | €40,816/ha | 8,429 |

| 2024 | 18 | €37,894/ha | €34,524/ha | 7,380 |

| 2025 | 12 | €41,330/ha | €39,361/ha | 6,881 |

* 2020: second half only.

Annual trend in DVF prices — Jura — Source: DVF, processed by ma-propriete.fr

The trajectory is upward over the period, with a cyclical trough in 2021 (€23,392/ha) followed by a gradual recovery to €39,361/ha in 2025 (+68% from the low point). This dynamic reflects the vineyard's quality renaissance: the establishment of many young winemakers since 2010, widespread conversion to organic and biodynamic farming, and growing international interest in yellow wines and wines aged under a veil of yeast. Transaction volumes remain modest, however (between 8 and 25 per year), which calls for some caution when interpreting annual medians.

The average transacted area tends to decrease (from 15,548 m² in 2020 to 6,881 m² in 2025), reflecting a market in transition: sales of complete estates are giving way to more targeted plot-by-plot transactions, typical of young winemakers progressively building up their holdings one parcel at a time.

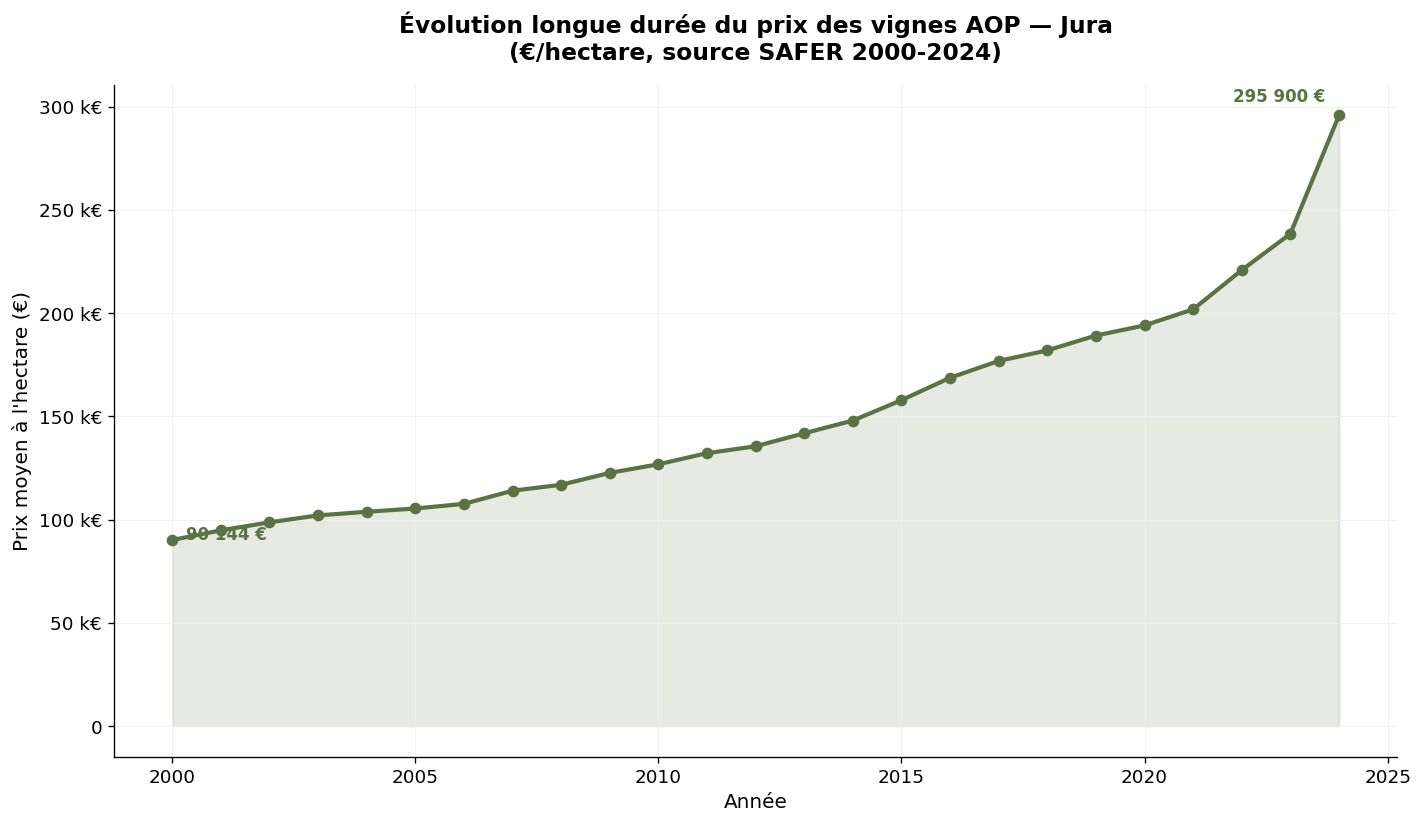

SAFER does not publish statistics specifically for the Jura: this vineyard region is grouped within the broader "Burgundy-Beaujolais-Savoie-Jura" aggregate. The figures below, to be treated as indicative only, reflect the dynamics of this wider grouping.

| Year | Average price (€/ha) | 5-year change |

|---|---|---|

| 2000 | 90,144 | — |

| 2010 | 126,832 | + 41% |

| 2020 | 201,900 | + 59% |

| 2024 | 295,900 | + 47% |

SAFER average price for AOP vineyards in Burgundy-Beaujolais-Savoie-Jura — Source: Ministry of Agriculture / SAFER

The aggregated SAFER trend is not representative of the Jura alone: the average is driven by Burgundy, whose levels far exceed those of the Jura. For the Jura specifically, the 2024 SAFER average can be estimated at a level consistent with the observed DVF average, i.e. around €35,000–45,000/ha.

The Jura vineyard is entirely contained within the Jura department: 89 transactions over the period, average price €37,820/ha, median price €37,622/ha, average area 8,730 m². The observed maximum (€84,507/ha) corresponds to emblematic plots in Château-Chalon or Arbois. The observed minimum (€6,884/ha) reflects the presence of plots in less highly valued areas.

Jura (39) — Annual trend — Source: DVF, processed by ma-propriete.fr

The Jura vineyard is organised around four main geographical appellations. The Côtes du Jura AOC, the largest, covers 80 communes and represents the regional base of the vineyard; land values typically range from €20,000 to €40,000/ha depending on the terroir. The Arbois AOC, covering 13 communes around the eponymous town, commands higher values thanks to its historical renown (Louis Pasteur conducted his work on fermentation there). The l'Étoile AOC, a micro-appellation around the village of l'Étoile, covers 65 hectares and is distinguished by its white wines and straw wines. The Château-Chalon AOC, devoted exclusively to yellow wine, is the most prestigious: the finest plots can exceed €80,000/ha, as illustrated by the observed DVF maximum.

Beyond the geographical AOCs, the Jura also produces "product" AOCs: Crémant du Jura (sparkling), Macvin du Jura (mistelle), Marc du Jura (marc brandy), which can be produced across the entire vineyard territory. This diversity of production represents a strategic opportunity for buyers: a single estate can combine several revenue streams, which strengthens the economic model.

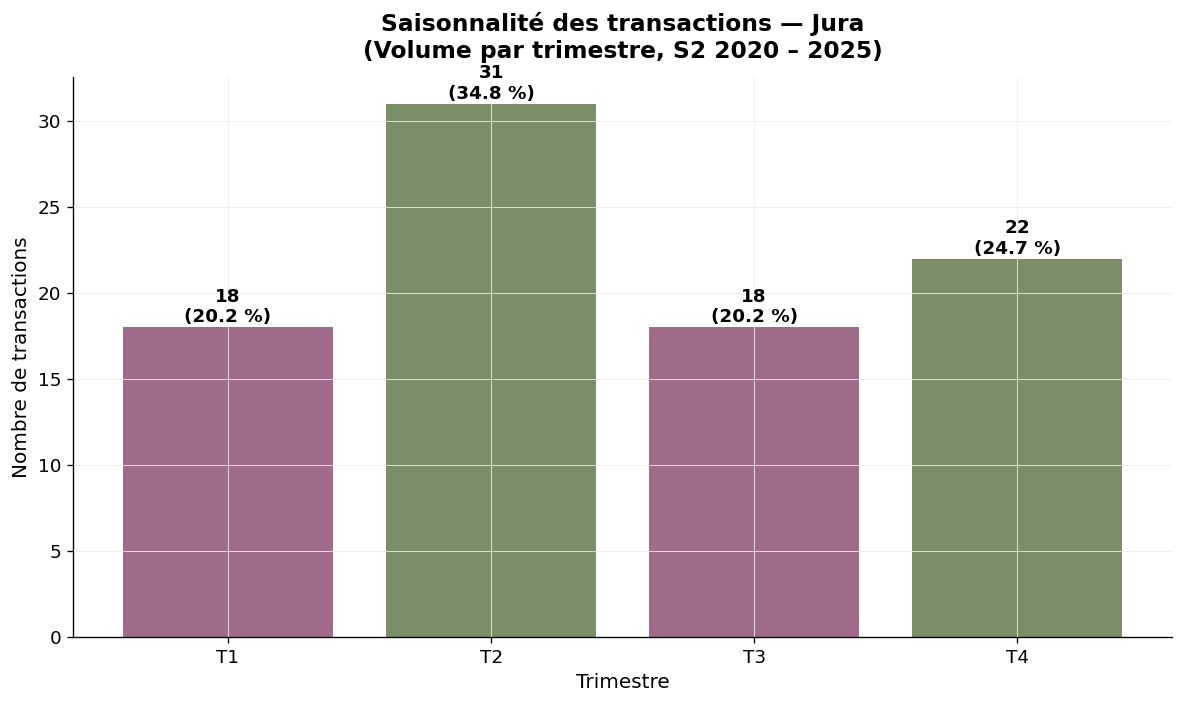

The seasonality of Jura transactions shows a concentration in the second quarter (34.8%), followed by the fourth (24.7%) and the first (20.2%). The third quarter, which corresponds to the harvest and pressing period, is the quietest (20.2%). This distribution is typical of a domain-scale vineyard, where transactions are finalised in spring and autumn, outside periods of intensive agricultural work.

Seasonality — Jura, volume by quarter — Source: DVF, processed by ma-propriete.fr

The DVF database records all real estate transfers for consideration registered by the DGFiP. To isolate vineyard transactions in the Jura, our observatory applies several filters: selection of plots cadastrally classified as "vineyards", cross-referencing with the INAO commune-by-commune register, and elimination of atypical transactions.

The year 2020 covers the second half only. The low volume of the vineyard (89 transactions over six years) calls for cautious interpretation: the annual median is sensitive to the transaction mix, particularly in years with modest volumes (8–12 transactions). Mixed properties (vineyards + farm buildings + wine cellar) are excluded when the value of the built elements represents a significant share, which rules out a portion of complete estate sales.

SAFER aggregates the Jura with Burgundy, Savoie and Beaujolais, which limits its usefulness for a specific analysis. Our DVF approach complements this picture by isolating the Jura alone, despite the low volume.

| Wine region | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Burgundy-Franche-Comté |

| Savoie | 57,216 | Savoie |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Current article |

| Beaujolais | 39,312 | Beaujolais |

| Cognac | 28,636 | Cognac |

| Rhône Valley | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Bordeaux |

| Roussillon | 13,918 | Languedoc-Roussillon |

| Languedoc | 13,531 | Languedoc-Roussillon |

| South-West | 9,205 | South-West |

Over the 2020–2025 period, the Jura offers a vineyard land market in full renaissance, with a sustained upward trajectory (+68% in the median since the 2021 trough) and growing transaction volumes. Values remain accessible (2024 median at €34,524/ha), for a wine region whose international quality recognition continues to grow. Land scarcity (1,800 hectares in total) and rising interest in indigenous grape varieties and distinctive wines (yellow wine, straw wine, biodynamics) underpin a revaluation potential over the medium term. For buyers with a structured project, the Jura represents one of the most compelling entry points in France for combining accessibility, originality and heritage investment potential. To go further, you can browse our wine estate listings, read our other articles on vineyard prices, or download our white paper on creating a wine estate.