Updated on May 19, 2026

The leading French wine region in terms of DVF transaction volume, the Languedoc-Roussillon basin constitutes the most liquid wine-growing land market in the country. With over 5,200 transactions recorded during the H2 2020 – 2025 period, it represents nearly 30% of the national vineyard market. This transactional intensity, combined with accessible unit prices, makes it a leading territory for buyers wishing to establish or expand a wine estate. Here we analyze the price of wine-growing vineyards in Languedoc-Roussillon over the 2020-2025 period, based on DVF (Land Value Requests) data and SAFER references. The 2024 figures serve as a robust reference year, and the 2025 figures are now complete. The 2025 DVF median prices stand at €13,531/ha in Languedoc and €13,918/ha in Roussillon, confirming a stable and accessible market. Please note: the year 2020 only covers the second half. This article is part of our observatory of vineyard prices in France.

For analytical purposes, we distinguish two groups: Languedoc (Hérault, Aude, the AOC Languedoc part of Gard), which covers nearly 220,000 hectares of planted vineyards and 4,169 DVF transactions over the period; and Roussillon (Pyrénées-Orientales), which covers approximately 18,000 hectares and 1,041 transactions. This distinction is important: while price levels are similar, the appellation dynamics and farming structures differ.

Over the entire H2 2020 – 2025 period, the average DVF price of vineyards in Languedoc stands at €17,731/ha and the median price at €13,845/ha. The gap between the average and the median is moderate (average = 1.28 × median), reflecting the remarkable homogeneity of the Languedoc market — a result of the unification of regional AOCs, the relative weight of IGPs and vins de France, and the accelerated transformation of the vineyard toward the professional estate format.

| Year | Volume | Average price | Median price | Avg. area (m²) |

|---|---|---|---|---|

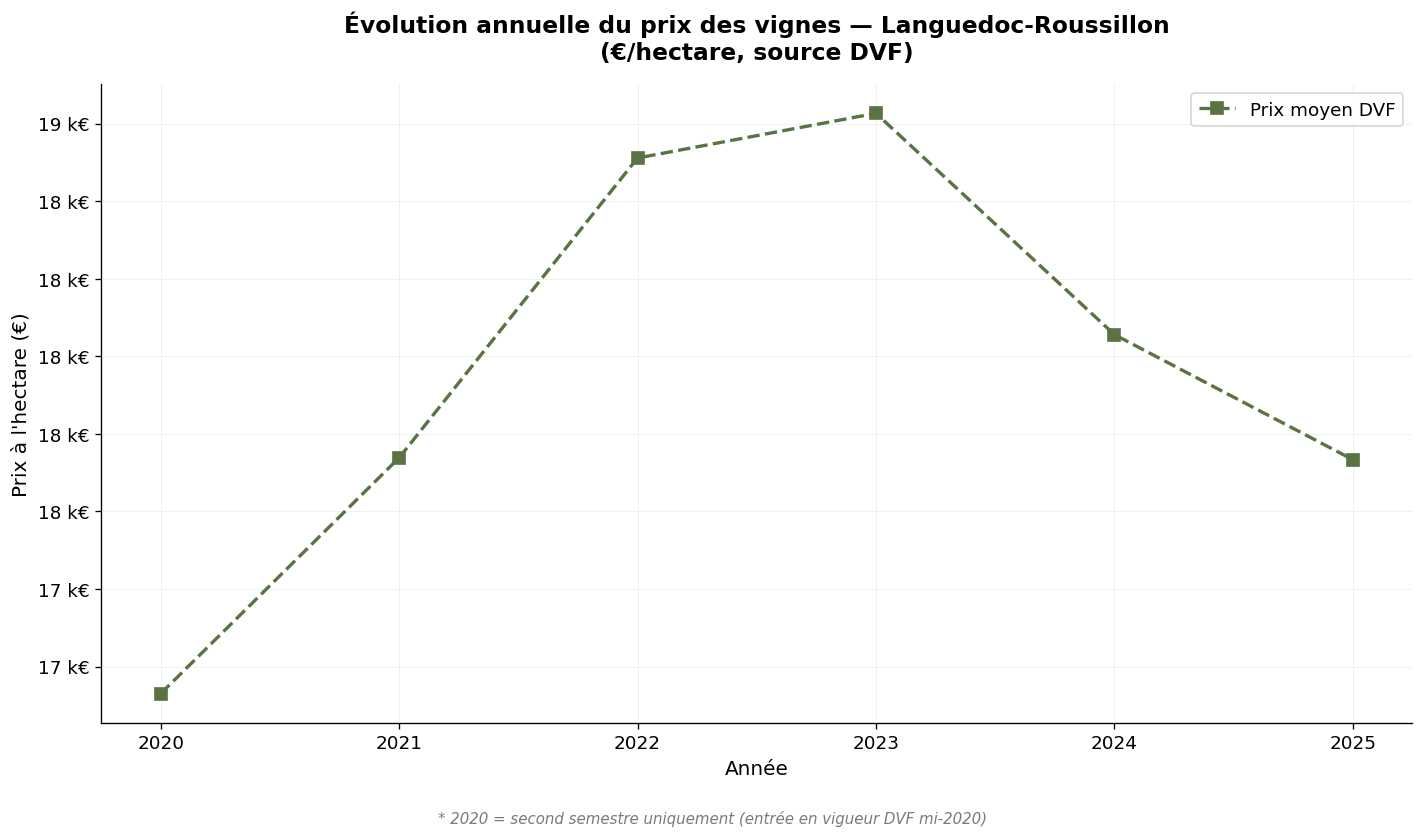

| 2020 * | 418 | €16,100/ha | €13,000/ha | 20,029 |

| 2021 | 823 | €17,621/ha | €13,529/ha | 18,397 |

| 2022 | 807 | €18,564/ha | €14,436/ha | 19,066 |

| 2023 | 774 | €18,307/ha | €14,253/ha | 17,945 |

| 2024 | 682 | €17,879/ha | €13,603/ha | 18,656 |

| 2025 | 665 | €17,060/ha | €13,531/ha | 19,540 |

* 2020: second half only.

Annual evolution of DVF prices — Languedoc-Roussillon — Source: DVF, processing by ma-propriete.fr

The observation is one of remarkable stability. The Languedoc median price has fluctuated within a narrow band of €13,000 to €14,500/ha over the entire period, with no pronounced upward or downward trend. The year 2025 confirms this point of equilibrium at €13,531/ha. The contraction in volumes, however, is notable: from 823 transactions in 2021 to 665 in 2025, representing a drop of nearly 20% in annual flow. This evolution reflects the gradual depletion of the sales flow linked to the 2017-2018 grubbing-up plan and the wait-and-see attitude of some sellers in a context of depressed bulk prices.

Over the same period, Roussillon recorded 1,041 transactions with an average DVF price of €19,372/ha and a median of €13,175/ha. Price levels are close to those of Languedoc, but the volume dynamic is more sustained: 172 transactions in 2025 versus 83 in 2020, over six fiscal years, illustrating a market that is not slowing down. The median price experienced a slight surge in 2023 (€14,954/ha) before returning to its point of equilibrium in 2024-2025 (around €13,500/ha).

| Year | Volume | Average price | Median price | Avg. area (m²) |

|---|---|---|---|---|

| 2020 * | 83 | €21,005/ha | €13,279/ha | 18,673 |

| 2021 | 214 | €17,874/ha | €11,093/ha | 15,613 |

| 2022 | 210 | €18,926/ha | €13,567/ha | 15,569 |

| 2023 | 199 | €20,632/ha | €14,954/ha | 17,464 |

| 2024 | 163 | €18,867/ha | €13,003/ha | 16,368 |

| 2025 | 172 | €20,013/ha | €13,918/ha | 13,916 |

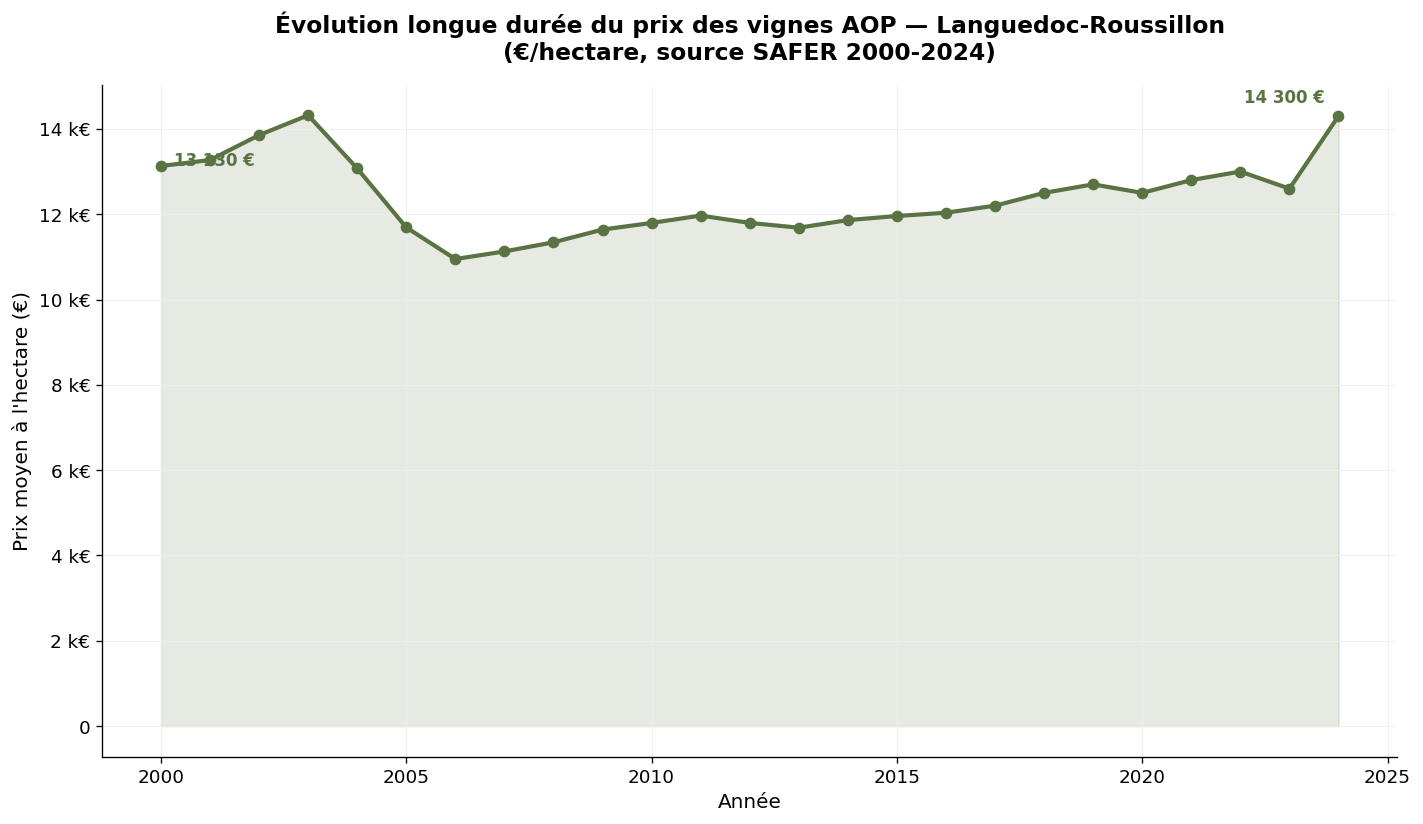

SAFER publishes aggregated statistics for the entire "Languedoc-Roussillon" region. Over the long term, the observation is one of great market inertia.

| Year | Average price (€/ha) | 5-year change |

|---|---|---|

| 2000 | 13,130 | — |

| 2010 | 11,796 | - 10 % |

| 2015 | 11,958 | + 1 % |

| 2020 | 12,800 | + 7 % |

| 2024 | 14,300 | + 12 % |

SAFER average price of AOP vineyards in Languedoc-Roussillon — Source: Ministry of Agriculture / SAFER

Over twenty-five years, the SAFER average price for the entire Languedoc-Roussillon region has risen by only 9%, a pace well below inflation. This is the most moderate evolution of any major French wine region. It reflects the persistence of a duality: a dynamic high-end segment on a few identity-defining appellations (Pic Saint-Loup, Faugères, Terrasses du Larzac, Maury, Banyuls, Collioure), which is seeing its prices rise, and a core market of IGPs and vins de France stable at structurally low levels. The convergence between the 2024 SAFER average (€14,300/ha) and the 2024 DVF median (€13,603/ha) is a strong indicator of consistency between the two reference systems in this region.

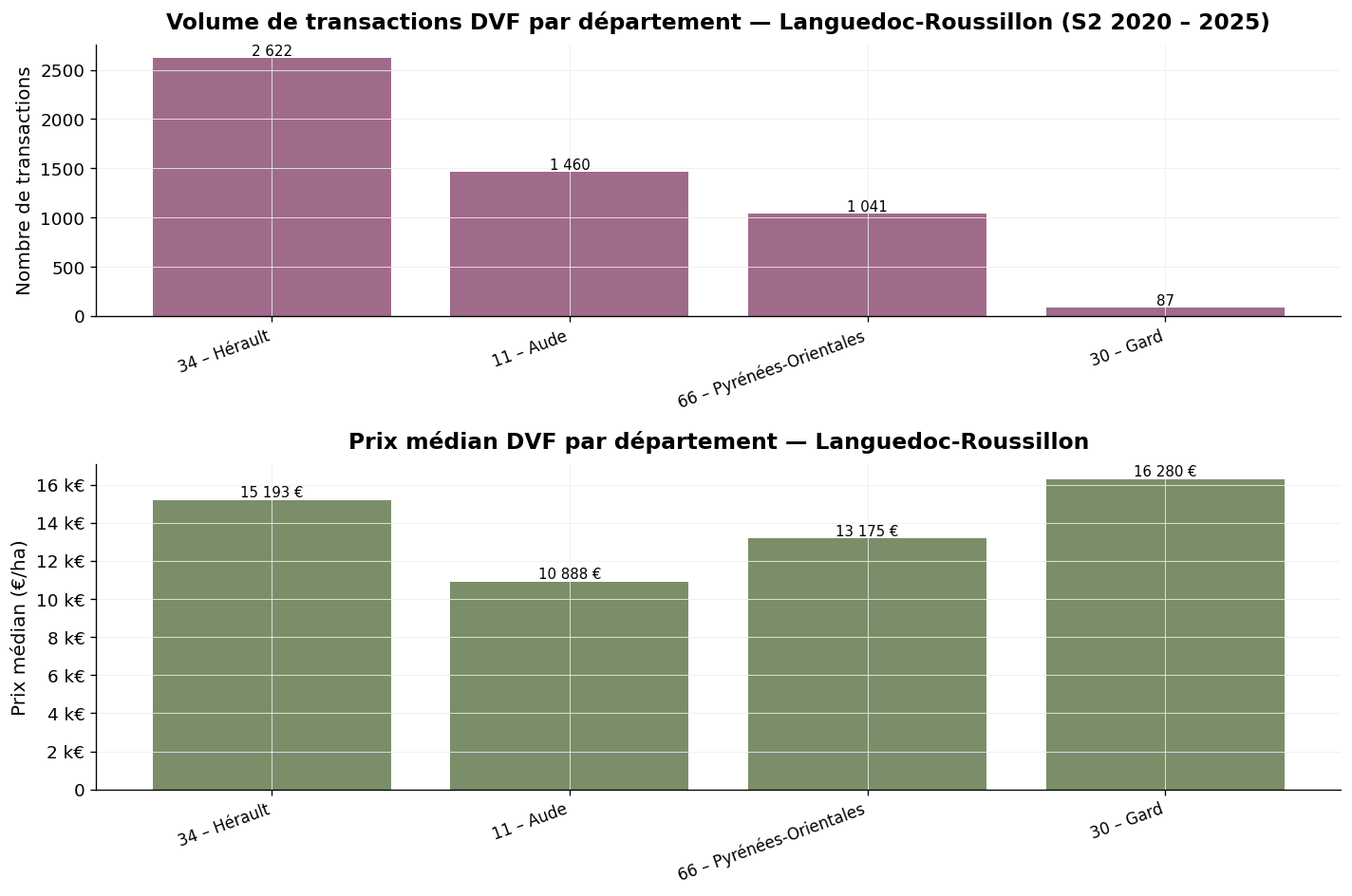

Volume and median price by department — Languedoc-Roussillon, H2 2020 – 2025 — Source: DVF, processing by ma-propriete.fr

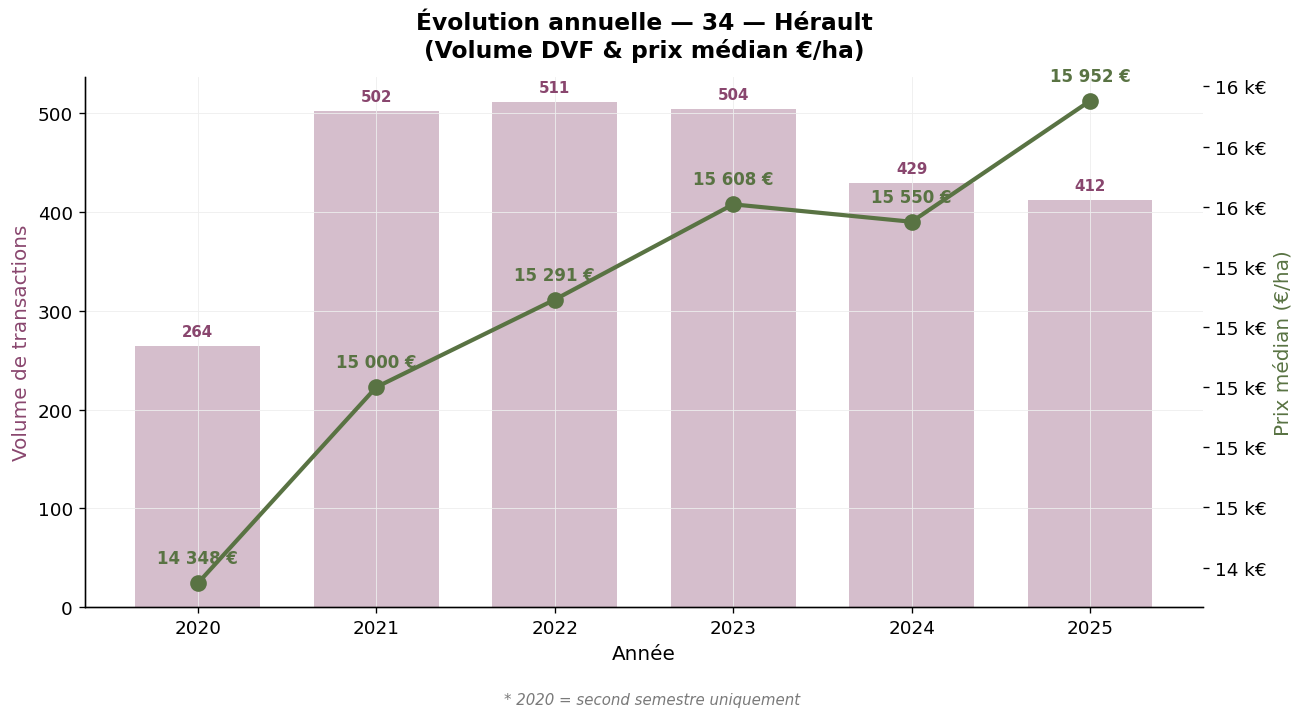

The leading wine-growing department in France by surface area, Hérault concentrates 2,622 DVF vineyard transactions (filtered AOC Languedoc) over the period, the highest volume in the entire observatory. The median price stands at €15,193/ha and the average at €20,061/ha. The dispersion is contained: between €6,242/ha for plots in less valued areas and €120,000/ha for the finest plots in Pic Saint-Loup or Terrasses du Larzac. The average transacted area (16,577 m²) is high compared to the national median, reflecting the estate dimension of the Hérault vineyard.

Hérault (34) — Annual evolution — Source: DVF, processing by ma-propriete.fr

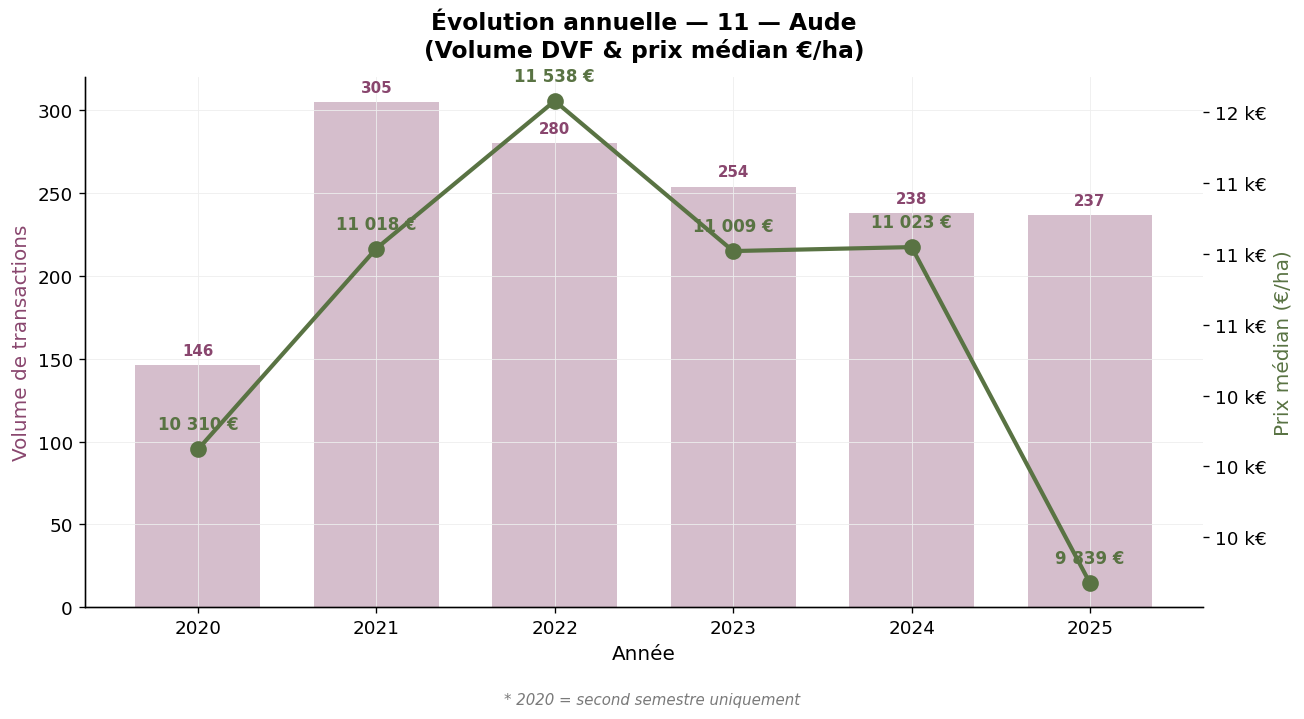

The second Languedoc department (1,460 transactions), Aude presents the lowest median price in the regional group: €10,888/ha, with an average of €13,296/ha. The average area (22,813 m²) is one of the highest in France, a sign of a vineyard where estate farming remains a dominant format. The observed maximum (€79,940/ha) corresponds to plots in AOC Corbières-Boutenac or Minervois la Livinière, segments undergoing qualitative repositioning. The median evolution is marked by a slight decline in 2025 (€9,839/ha versus €11,023/ha in 2024), linked to the context of overproduction and tensions on regional bulk prices.

Aude (11) — Annual evolution — Source: DVF, processing by ma-propriete.fr

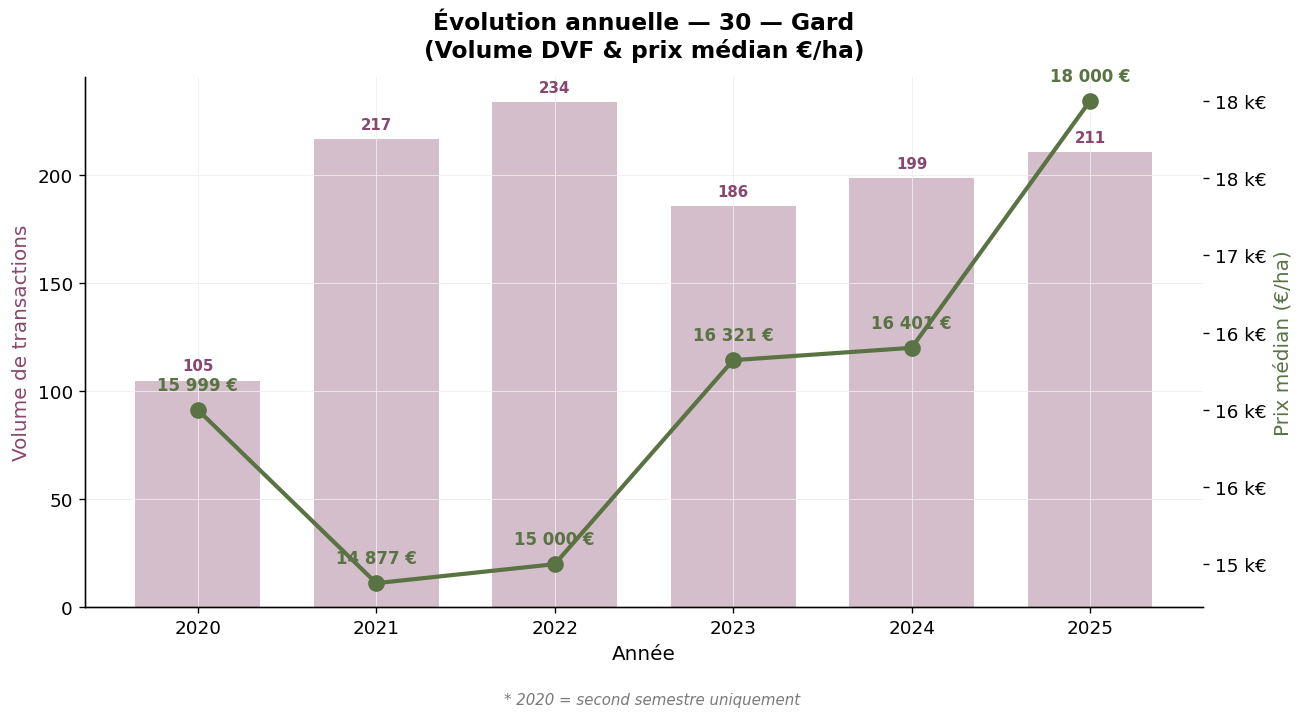

Gard is a border department between the Rhône Valley and Languedoc. Our observatory distinguishes transactions according to their AOC appellation: the AOC Languedoc part counts 87 transactions over the period, for a median price of €16,280/ha and an average of €21,931/ha. These levels, significantly higher than the Languedoc average, reflect the quality of Gard's terroirs in AOC Costières de Nîmes, Duché d'Uzès and Pic Saint-Loup. The Rhône Valley part of Gard is covered in our article dedicated to the Rhône Valley-Provence.

Gard (30) — Annual evolution — Source: DVF, processing by ma-propriete.fr

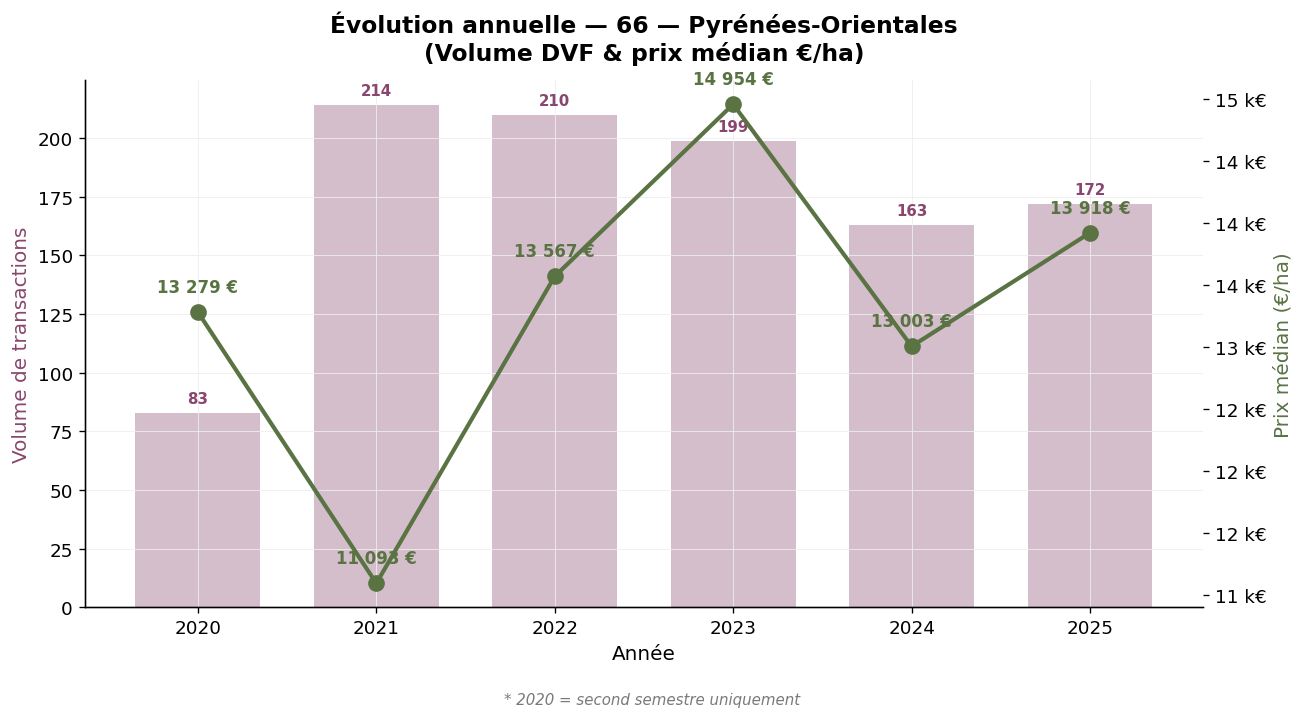

The unique heart of the Roussillon vineyard, Pyrénées-Orientales concentrates 1,041 transactions over the period, making it the fourth wine-growing department in France by volume. The median price stands at €13,175/ha and the average at €19,372/ha. The average area (16,040 m²) is in line with the Roussillon format. The trajectory is interesting: after a trough in 2021 (median €11,093/ha), the market gradually firmed up to reach €14,954/ha in 2023, before a slight adjustment in 2024-2025. The observed maximum (€83,492/ha) corresponds to plots in AOC Banyuls, Maury or Côtes du Roussillon Villages where the land value of natural sweet wines and old black grenaches remains strong.

Pyrénées-Orientales (66) — Annual evolution — Source: DVF, processing by ma-propriete.fr

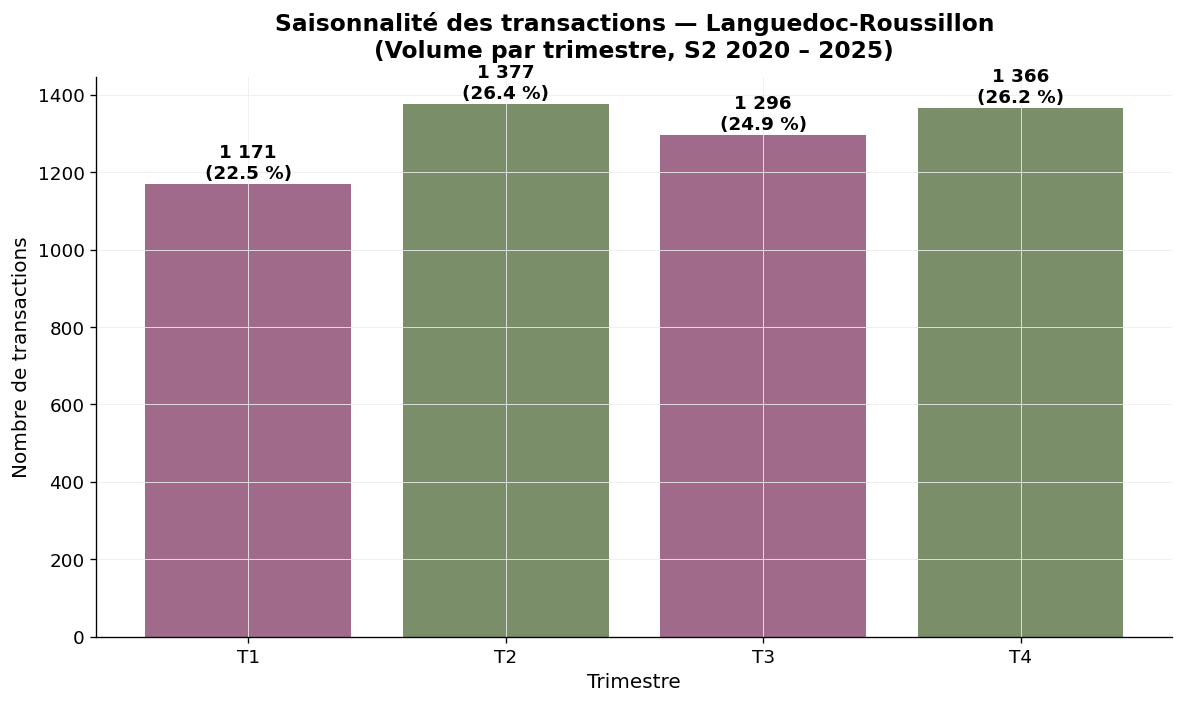

Across the entire Languedoc-Roussillon region, transaction seasonality is one of the most balanced in France, with a slight peak in the second and fourth quarters. Q1 represents 22.4% of transactions, Q2 26.3%, Q3 24.8% and Q4 26.6%. This relatively flat distribution, compared to the year-end concentration observed in Bordeaux, reflects a continuous market, with little seasonality, where transactions follow one another without any dominant fiscal or calendar logic.

Seasonality — Languedoc-Roussillon, volume by quarter — Source: DVF, processing by ma-propriete.fr

The DVF (Land Value Requests) database lists all real estate transfers for valuable consideration recorded by the DGFiP. To isolate vineyard transactions from this database, our observatory applies several filters: selection of plots registered in the cadastre as "vineyards", cross-referencing with the INAO repository commune by commune (to distinguish in Gard the AOC Languedoc from the AOC Côtes du Rhône), elimination of atypical transactions. For each wine region, the average price, median price, extreme values and average area are calculated.

The year 2020 only covers the second half. Mixed properties (vineyards + farm buildings) are excluded when the value of the buildings represents a significant share. The relevance of the data is very high in Languedoc and Roussillon due to the large volume of transactions; for the Languedoc part of Gard, the more limited volume (87 transactions) calls for cautious interpretation.

SAFER statistics are based on a survey of notaries and a filtering of transactions of more than half a hectare in one block. They provide an annual average price with remarkable historical depth (since 1991), aggregated for the entire Languedoc-Roussillon region. Our DVF approach complements this view by providing a median price, departmental granularity and seasonality.

With a 2024 DVF median price of around €13,300/ha, Languedoc-Roussillon is positioned at the bottom of the national hierarchy, just ahead of the South-West. This position paradoxically makes it the most attractive market for new entrants: financial accessibility allows for the establishment of an estate of several dozen hectares at a land acquisition cost that would remain that of a single plot in Champagne or Burgundy. It is precisely this equation that has fueled, over the past twenty years, a wave of new winegrower settlements, foreign investors and buyers in search of revaluation potential.

| Wine region | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Burgundy-Franche-Comté |

| Savoie | 57,216 | Savoie |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Jura |

| Beaujolais | 39,312 | Beaujolais |

| Cognac | 28,636 | Cognac |

| Rhône Valley | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Bordeaux |

| Roussillon | 13,918 | Current article |

| Languedoc | 13,531 | Current article |

| South-West | 9,205 | South-West |

Languedoc-Roussillon offers, in 2024 and 2025, a stable, accessible and liquid land market. The DVF median remains around €13,000-14,000/ha, with no short-term signal of reversal. Hérault concentrates the volume, Aude offers the most accessible entry points, Roussillon presents a qualitative dynamic supported by the natural sweet wine and black grenache appellations. The contraction in volumes observed since 2021 reflects the gradual slowdown of the grubbing-up flow and cyclical wait-and-see attitudes, but does not signal a price reversal. For a buyer with a structured project, the region remains the most favorable French territory for a significant winegrowing settlement. To go further, you can consult our category of wine-growing listings, our other articles on vineyard prices or download our white paper on creating a wine estate.