Updated on May 18, 2026

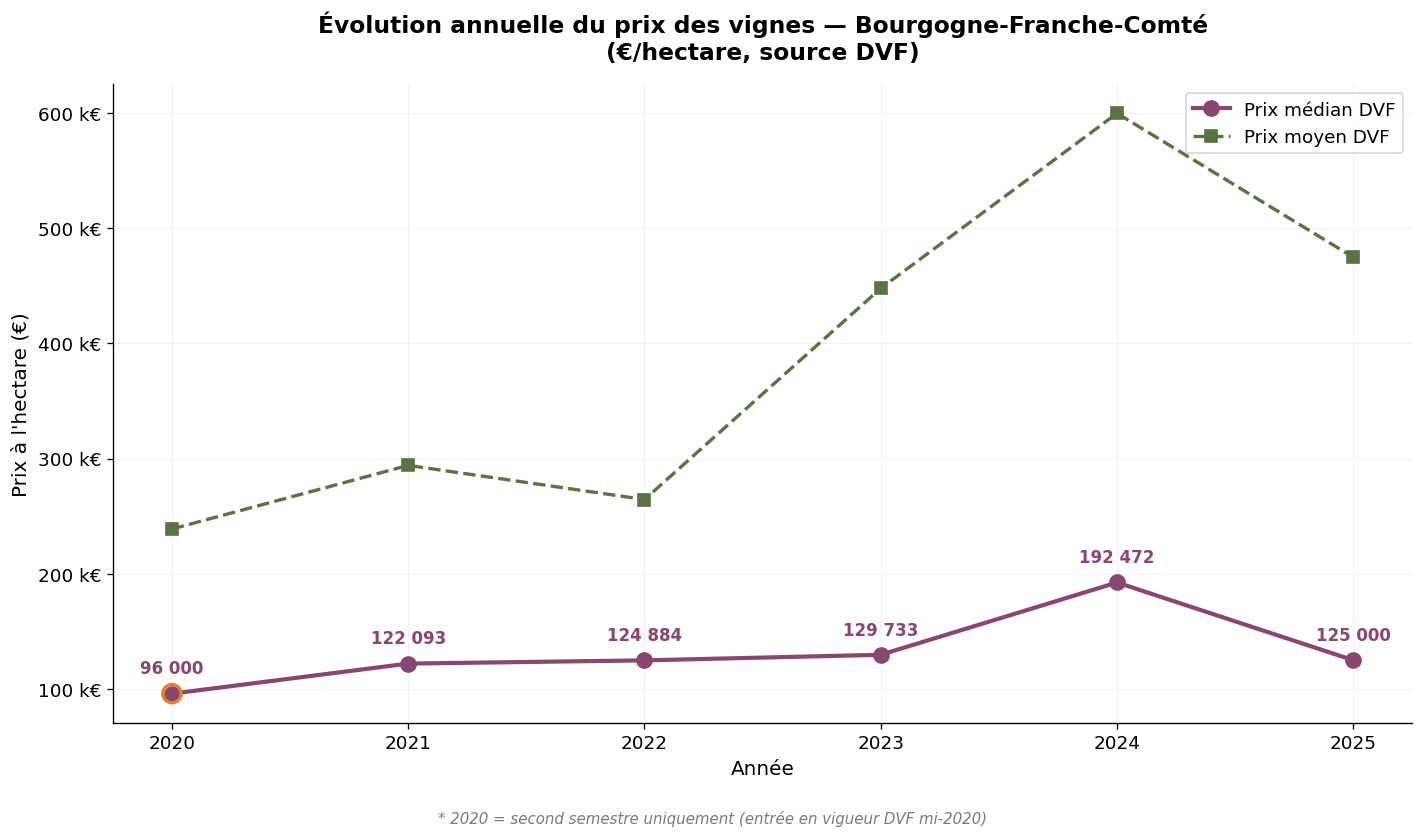

The Burgundy vineyard is one of the most distinctive and highly valued wine regions in France. Organized around a uniquely refined system of parcel-level climats, listed as a UNESCO heritage site since 2015, Burgundy combines limited production with sustained global demand, making it one of the tightest vineyard land markets in the country. Here we analyze the price of wine-producing vineyards in Burgundy-Franche-Comté over the 2020-2025 period, based on DVF (Property Value Requests) data and SAFER references. In accordance with the vineyard's geographical boundaries, the scope covers the three Burgundy departments (Côte-d'Or, Saône-et-Loire, Yonne); the Jura, treated as a separate vineyard in our observatory, is the subject of a specific commentary at the end of the article. The 2025 figures, now complete, constitute our main reference year, while the 2024 figures provide a robust basis for comparison. The 2025 median DVF price stands at €125,000/ha, correcting after the exceptional 2024 peak of €192,472/ha. Please note: 2020 only covers the second half of the year. This article is part of our observatory of vineyard prices in France.

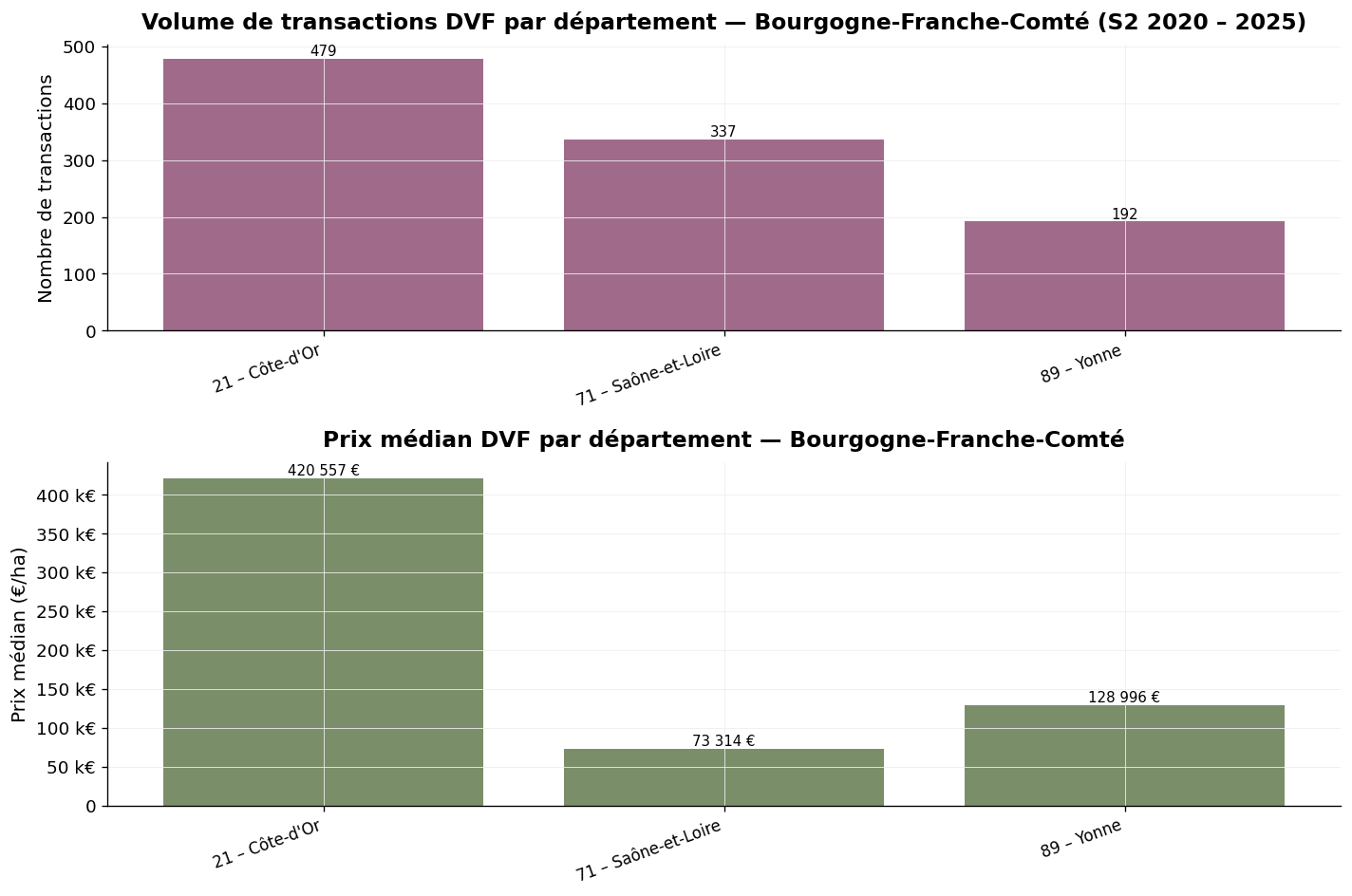

The Burgundy vineyard covers approximately 30,000 hectares classified as AOC, spread from north (Chablis area) to south (Mâconnais), with a historic core in Côte d'Or (Côte de Nuits, Côte de Beaune). It is an extremely fragmented vineyard — a single clos of several hectares may be divided among dozens of owners — where land scarcity takes precedence over surface area. Over the H2 2020 – 2025 period, our observatory records 1,008 vineyard transactions within the three Burgundy departments.

The DVF average price stands at €402,654/ha and the median price at €129,487/ha for the entire period. The gap between average and median — the average representing more than three times the median — illustrates the strong heterogeneity of the Burgundy vineyard, where Vosne-Romanée or Chambertin grand crus (several million euros per hectare) coexist with regional appellations from the Mâconnais or Châtillonnais (a few tens of thousands of euros). The median price therefore constitutes the most representative indicator of the current market, while the average price reflects the range.

| Year | Volume | Average price | Median price | Avg. surface area (m²) |

|---|---|---|---|---|

| 2020 * | 93 | €238,889/ha | €96,000/ha | 8,130 |

| 2021 | 188 | €294,094/ha | €122,093/ha | 7,848 |

| 2022 | 161 | €264,495/ha | €124,884/ha | 7,328 |

| 2023 | 168 | €447,788/ha | €129,733/ha | 8,385 |

| 2024 | 173 | €599,656/ha | €192,472/ha | 8,416 |

| 2025 | 225 | €474,741/ha | €125,000/ha | 10,629 |

* 2020: second half only.

Annual evolution of vineyard prices in Burgundy — Source: DVF, processed by ma-propriete.fr

The trajectory is upward through 2024, with a remarkable peak that year: the median price jumped from €129,733/ha in 2023 to €192,472/ha in 2024, a 48% rise in a single year. This surge is mainly explained by a mix effect: an unusual share of transactions in 2024 involved parcels classified as grands and premiers crus, whose high unit value pulled the median upward. The 2024 maximum — €5,815,726/ha — confirms the intensity of activity at the high end of the market.

The 2025 year, now complete, points to a return to more representative levels: median price at €125,000/ha, which lies between the 2022 and 2023 values. This correction does not signal a market reversal, but rather a rebalancing of the transaction mix after the exceptional 2024 year. Transaction volume reaches its cumulative maximum in 2025 (225 mutations), reflecting high market liquidity.

The average transacted surface area is one of the smallest in France (around 8,500 m² per mutation), a structural feature of the Burgundy vineyard where transmission takes place parcel by parcel, or even climat by climat. The increase to 10,629 m² in 2025 is noteworthy: it could reflect the arrival on the market of larger estates, in a context of accelerated generational transmission.

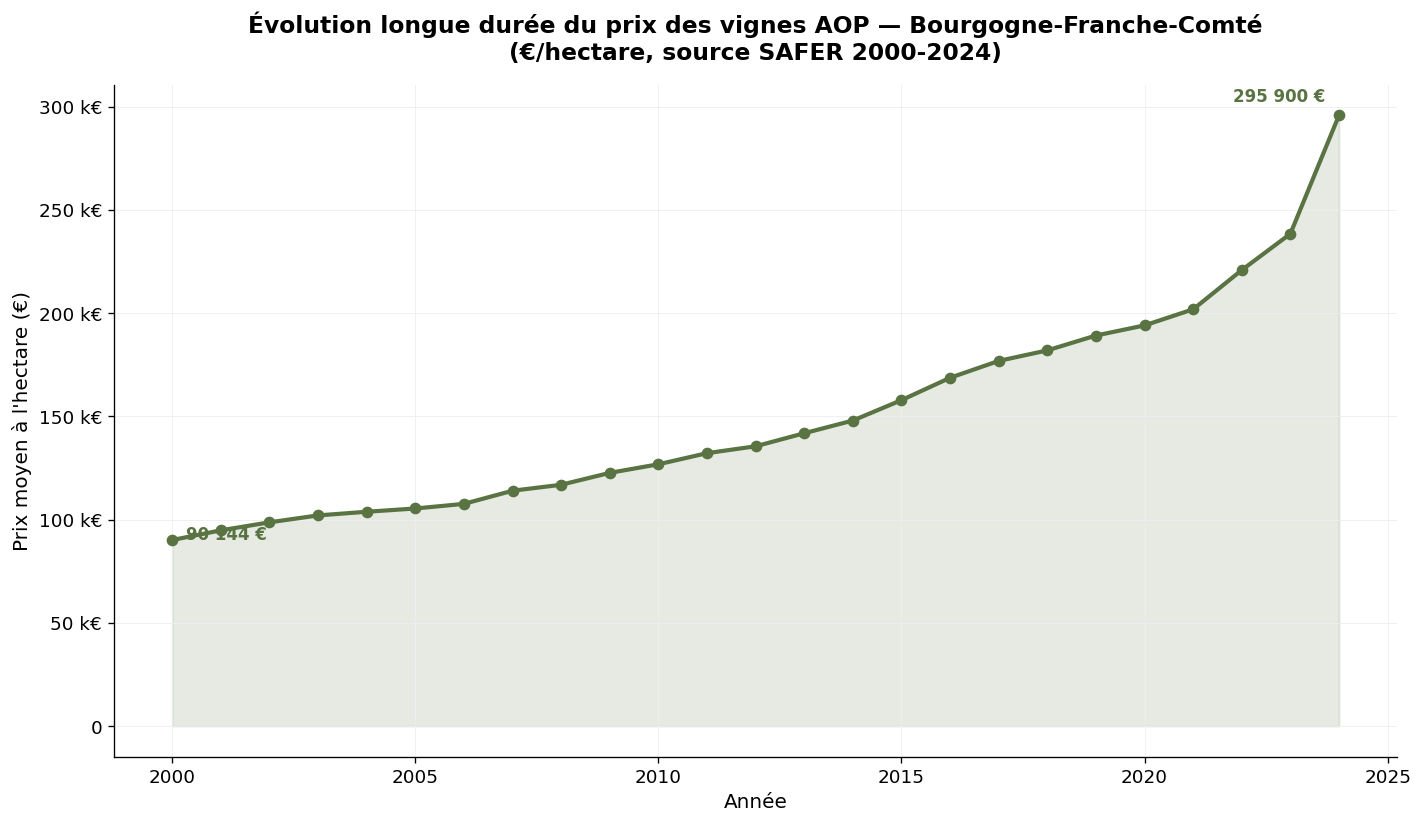

SAFER publishes aggregated statistics for the "Burgundy-Beaujolais-Savoie-Jura" area. This aggregation, broader than our scope, nevertheless provides a valuable indication of the long-term trajectory.

| Year | Average price (€/ha) | 5-year change |

|---|---|---|

| 2000 | 90,144 | — |

| 2005 | 105,421 | + 17% |

| 2010 | 126,832 | + 20% |

| 2015 | 157,891 | + 24% |

| 2020 | 201,900 | + 28% |

| 2024 | 295,900 | + 47% |

SAFER average price of AOP vineyards in Burgundy-Beaujolais-Savoie-Jura — Source: Ministry of Agriculture / SAFER

Over twenty-five years, the SAFER average price of the broader Burgundy area has more than tripled (+228%), with a particularly sharp acceleration starting in 2020. The 47% increase observed between 2019 and 2024 illustrates the tension in the land market, fueled by demand from major houses, wealth investors and family successions seeking to consolidate their holdings. The comparison between the 2024 SAFER average (€295,900/ha) and the 2024 DVF average (€599,656/ha) should be interpreted with caution: the scopes are not identical (SAFER aggregates Beaujolais-Savoie-Jura, which weight downward), and the transactional practices differ (SAFER filters mutations larger than 50 ares as a block, whereas DVF includes all mutations).

Volume and median price by department — Burgundy, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

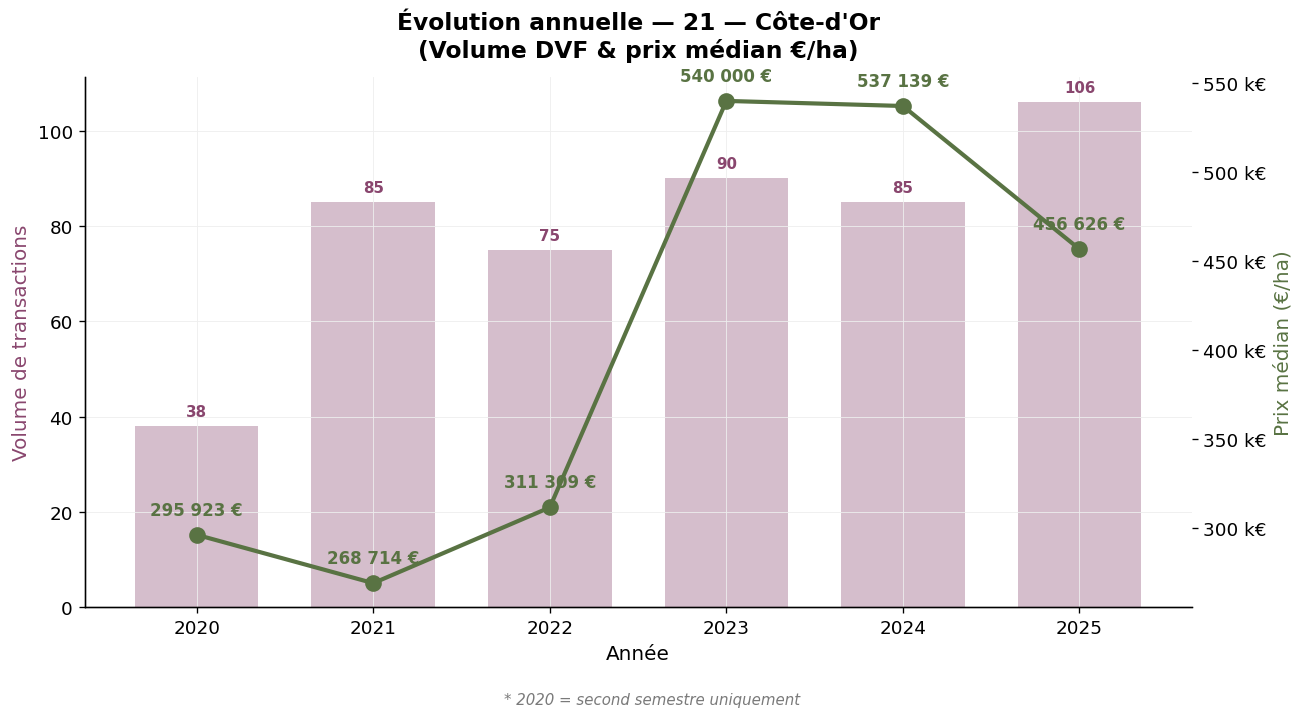

The historic heart of the Burgundy vineyard, Côte-d'Or concentrates 479 transactions and unsurprisingly shows the highest median price in Burgundy: €420,557/ha over the period. The average (€730,937/ha) reflects the presence of grands crus and premiers crus from the Côte de Nuits and the Côte de Beaune. The maximum observed (€5,815,726/ha) illustrates the extreme value reached by certain iconic parcels. The average surface area (7,854 m²) confirms parcel-by-parcel transmission. The annual evolution is equally remarkable: the median price went from €295,923/ha in 2020 to €537,139/ha in 2024, a 82% increase in four years, followed by an adjustment to €456,626/ha in 2025.

Côte-d'Or (21) — Annual evolution, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

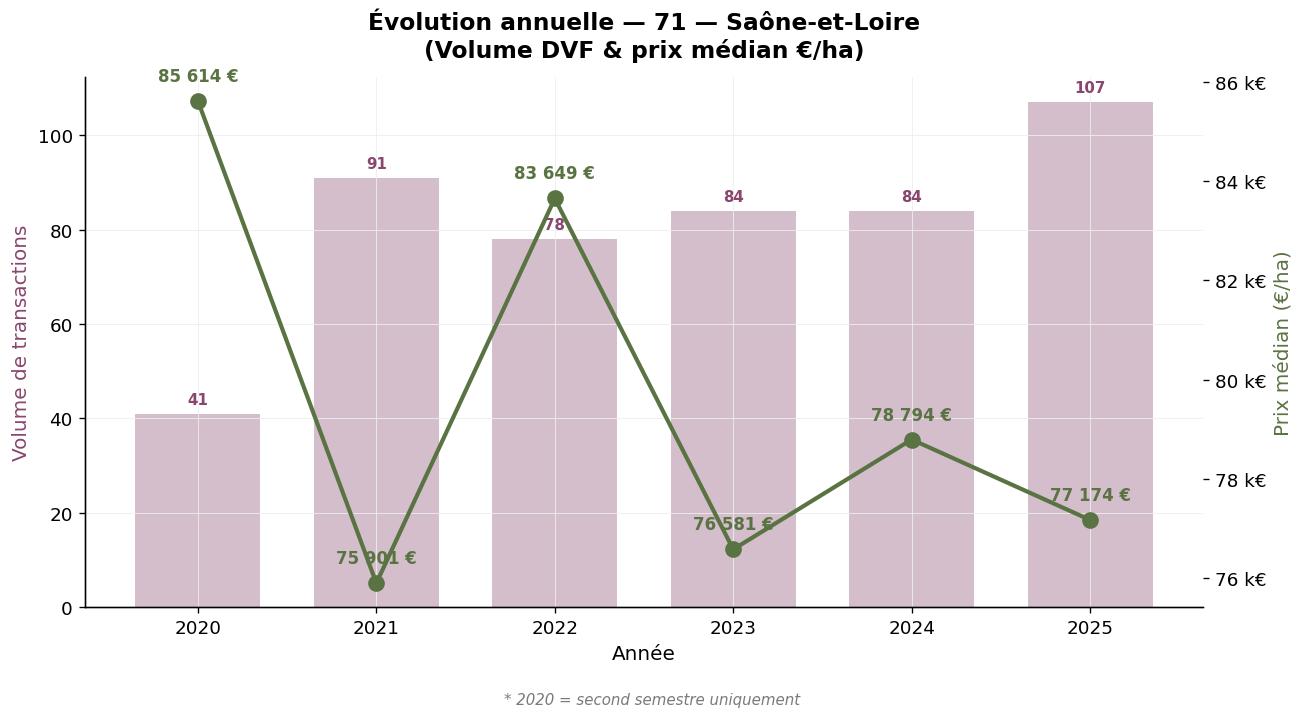

Second most active Burgundy department (337 transactions for Burgundy AOCs alone, excluding Beaujolais AOCs), Saône-et-Loire covers the Côte chalonnaise and the northern Mâconnais. The median price stands at €73,314/ha, significantly lower than Côte-d'Or, reflecting the lesser relative prestige of the Mercurey, Givry, Rully and Saint-Véran AOCs compared with the climats of Côte d'Or. The average (€87,943/ha) remains close to the median, a sign of a more homogeneous market. The average surface area (9,688 m²) is slightly larger than that of Côte-d'Or.

Saône-et-Loire (71) — Annual evolution, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

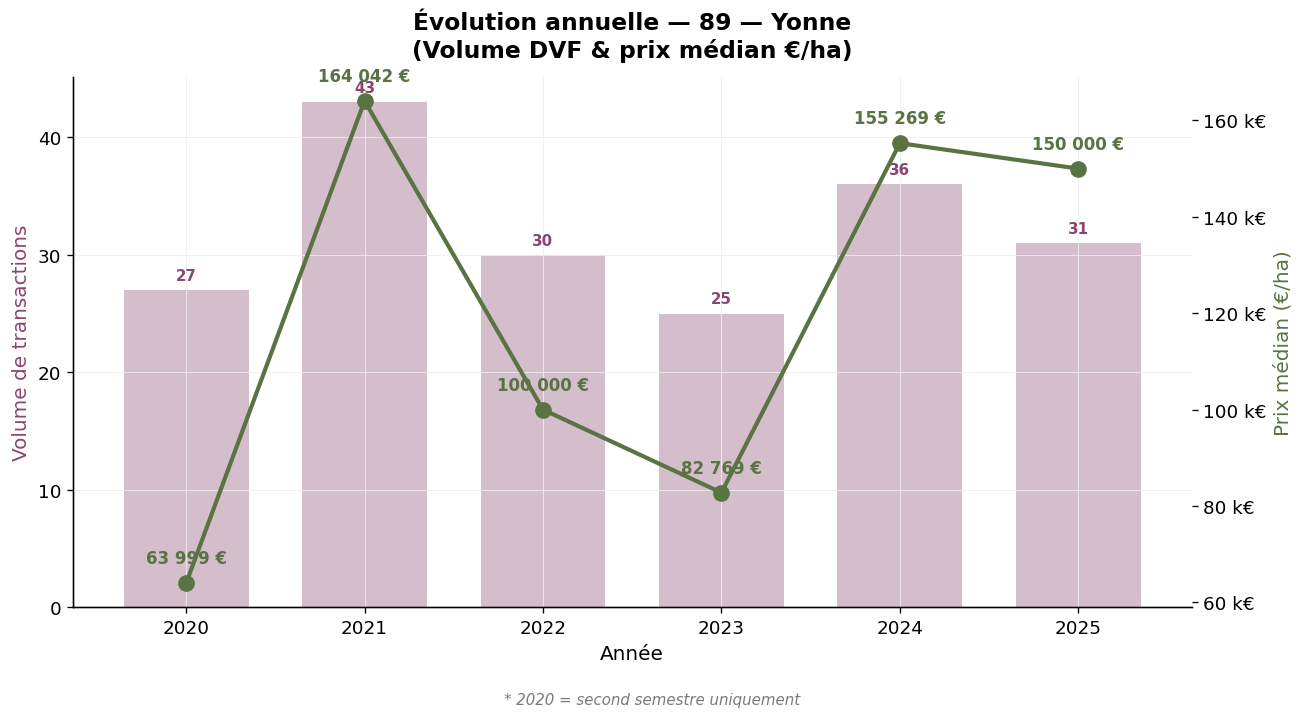

Yonne, the third Burgundy department by volume (192 transactions), essentially covers the Chablis vineyard and the Auxerrois and Tonnerrois vineyards. The median price stands at €128,996/ha, slightly above the overall Burgundy median, reflecting the resilience of the Chablis market in the face of international chardonnay competition. The average (€136,043/ha) is very close to the median, a sign of a homogeneous market. The average surface area (8,543 m²) is in line with Burgundy practices.

Yonne (89) — Annual evolution, H2 2020 – 2025 — Source: DVF, processed by ma-propriete.fr

The Jura department (39), although attached to the Burgundy-Franche-Comté administrative region, constitutes a distinct vineyard in the viticultural sense — with its own grape varieties (savagnin, poulsard, trousseau), its own appellations (Arbois, Château-Chalon, l'Étoile, Côtes du Jura) and its own land market. Over the H2 2020 – 2025 period, our observatory records 89 transactions in the Jura, with a median price of €37,622/ha and an average price of €37,820/ha. The trend is positive: the median rose from €23,392/ha in 2021 to €39,361/ha in 2025, a 68% increase over the period, in a context of renewed interest in distinctive and natural wines. For a more in-depth analysis of the Jura market, see our full observatory.

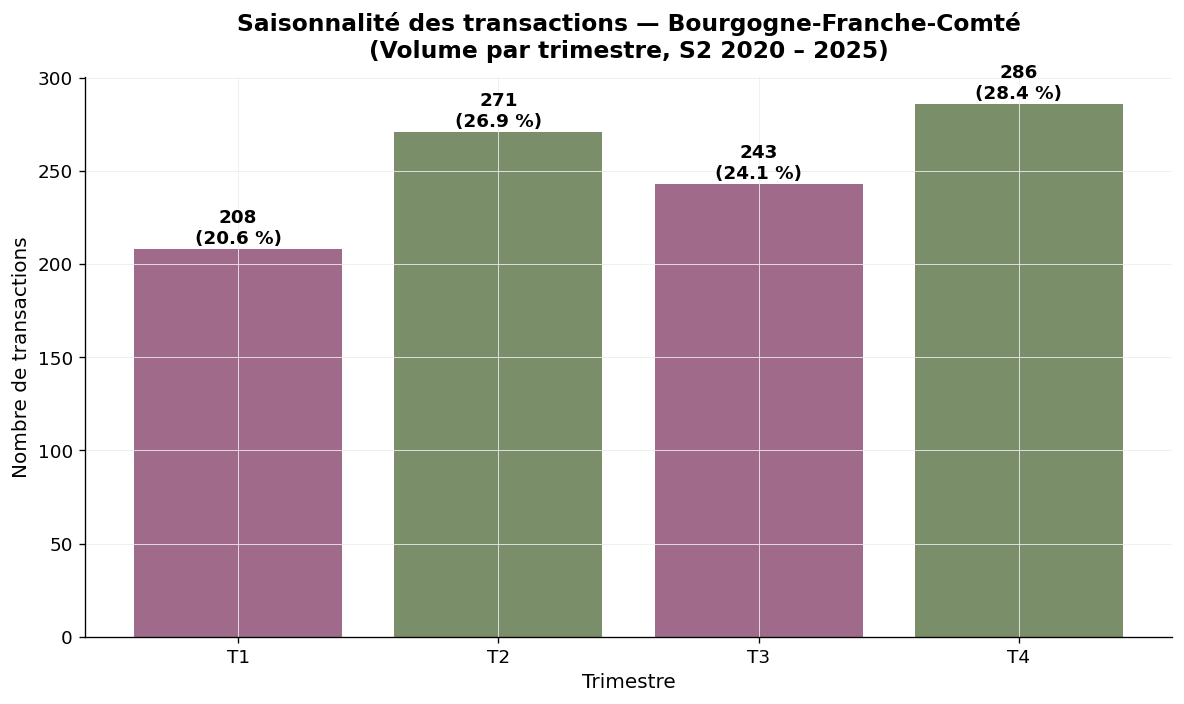

Transactions are distributed relatively evenly throughout the year: Q1 (208 sales, 20.6%), Q2 (271, 26.9%), Q3 (243, 24.1%), Q4 (286, 28.4%). There is a slight concentration in the second and fourth quarters, which correspond respectively to non-harvest periods conducive to finalizing transfers, and to accounting and tax year-ends.

Seasonality — Burgundy, volume by quarter — Source: DVF, processed by ma-propriete.fr

The DVF database (Property Value Requests) records all property transfers for consideration registered by the DGFiP. To isolate vineyard transactions within this database, our observatory applies several filters: selection of parcels cadastrally registered as "vineyards," cross-referencing with the INAO repository commune by commune (to distinguish, in Saône-et-Loire, the Burgundy AOCs from the Beaujolais AOCs), elimination of atypical transactions. For each vineyard, the average price, the median price, the extreme values and the average surface area are calculated. The median price, which represents the level at which half the market is concluded, is our reference indicator; it is less sensitive to exceptional sales than the average.

Three precautions should be taken. The 2020 year only covers the second half. Mixed properties (vineyards + cellar + farm buildings) are excluded when the value of the buildings represents a significant share of the total value; some complete estate sales may thus be excluded, which potentially underrepresents the very high end of the Burgundy market. Finally, the Burgundy market, more than any other in France, lends itself to sales of very small parcels (a few ares), which can introduce statistical volatility into annual medians for a given department. We explicitly flag departments with low transaction volumes.

SAFER statistics, published by the Ministry of Agriculture, are based on a survey of notaries and filter transactions of more than half a hectare as a block. For Burgundy, SAFER aggregates Beaujolais, Savoie and Jura, broadening the scope compared with our DVF approach (limited to the three Burgundy departments strictly speaking). SAFER provides an annual average price with remarkable historical depth (since 1991). Our DVF approach is complementary: it captures all mutations, provides a median price, and enables sub-departmental analysis.

| Wine region | 2025 median price (€/ha) | Detailed article |

|---|---|---|

| Champagne | 1,000,000 | Champagne |

| Burgundy | 125,000 | Current article |

| Savoie | 57,216 | Savoie |

| Provence | 39,864 | Provence |

| Jura | 39,361 | Jura |

| Beaujolais | 39,312 | Beaujolais |

| Cognac | 28,636 | Cognac |

| Rhône Valley | 20,357 | Rhône Valley |

| Loire Valley | 17,000 | Loire Valley |

| Bordeaux | 15,434 | Bordeaux |

| Roussillon | 13,918 | Languedoc-Roussillon |

| Languedoc | 13,531 | Languedoc-Roussillon |

| South-West | 9,205 | South-West |

The Burgundy vineyard market is characterized by land valuations among the highest in France, second only to Champagne, and by a sustained upward trajectory over the long term. The 2024 year marked a spectacular high (median at €192,472/ha), corrected in 2025 to a more representative level (€125,000/ha), while transaction volumes reach their cumulative maximum. Côte-d'Or remains the most valued and most active department, Yonne is positioned at an intermediate level thanks to Chablis, and Saône-et-Loire offers more affordable entry points for the Côte chalonnaise and the Mâconnais. The Jura, treated as a separate vineyard, shows a marked upward trend at much more accessible levels. To go further, you can consult our wine-producing property listings category, our other articles on vineyard prices or download our white paper on creating a wine estate.