Occitanie is one of the major forest regions in France. With approximately 2.6 million hectares of woodland, forests cover more than a third of its territory, from the Pyrenean foothills to the edges of the Massif Central, including Mediterranean scrublands (garrigues). The species are highly diverse: pubescent and holm oaks on the causses and garrigues, beeches and firs on the mountain slopes, maritime and Scots pines on intermediate reliefs, and chestnut trees in the Cévennes. This landscape mosaic results in a forest real estate market that is very heterogeneous from one department to another.

The Occitan forest-wood sector employs more than 30,000 people and fuels a significant local economy, ranging from timber harvesting and wood energy to estate management. For both buyers and sellers, knowing market prices is an indispensable prerequisite for any transaction.

This article presents the results of our analysis of 3,347 forest transactions recorded in Occitanie between July 2020 and June 2025, based on the DVF (Demandes de Valeurs Foncières) database from the Ministry of the Economy. Data for the first half of 2025 are available but partial: they must be interpreted with caution and cannot be directly compared to full years. The year 2024, being complete, serves as our primary reference.

For a national view of the market, consult our observatory of forest prices in France. You can also find forests for sale listings on our platform, specifically forests for sale in Occitanie.

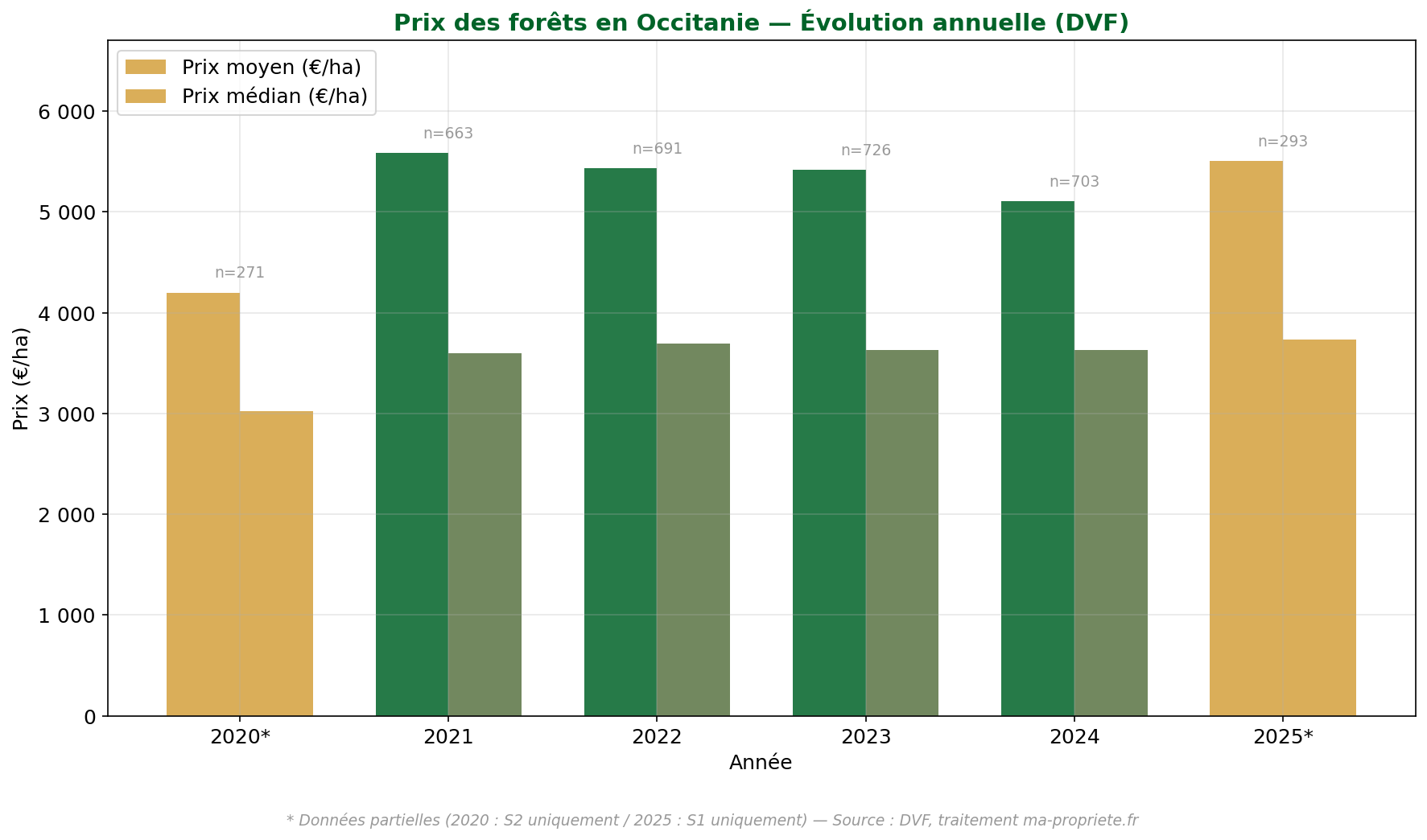

For the first half of 2025 (partial data, to be interpreted with caution), the median price of a hectare of forest in Occitanie stands at €3,731/ha, with an average price of €5,503/ha. These figures are based on only 293 transactions, a reduced sample compared to a full year.

For the year 2024, the full reference year, the median price is €3,632/ha with an average price of €5,109/ha, based on 703 transactions. Occitanie thus positions itself among the most accessible regions in metropolitan France, with a median price significantly lower than the national average (€4,846/ha in 2024).

The significant gap between the average and median prices (around €1,400/ha in 2024) reflects the presence of some transactions with high unit prices — often small peri-urban plots or exceptional forests in mountain zones — which pull the average up without reflecting the reality of the majority of sales.

Over the entire 2020-2025 period, Occitanie totaled 3,347 transactions for an exchanged volume of over 31,000 hectares and a median surface area of 3.47 hectares per sale.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price (€/ha) | Max price (€/ha) | Median area (ha) |

|---|---|---|---|---|---|---|

| 2020* | 271 | 4,200 | 3,021 | 536 | 27,360 | 4.33 |

| 2021 | 663 | 5,584 | 3,600 | 825 | 51,047 | 3.49 |

| 2022 | 691 | 5,433 | 3,691 | 887 | 45,637 | 3.66 |

| 2023 | 726 | 5,417 | 3,627 | 588 | 33,000 | 3.23 |

| 2024 | 703 | 5,109 | 3,632 | 654 | 59,292 | 3.30 |

| 2025* | 293 | 5,503 | 3,731 | 759 | 53,252 | 3.65 |

* 2020: H2 data only / 2025: H1 data only (partial). Source: DVF, ma-propriete.fr processing.

Annual evolution of forest prices in Occitanie (2020-2025) — Source: DVF, ma-propriete.fr processing

Over the four full years (2021-2024), the median price in Occitanie fluctuated within a narrow range, between €3,600 and €3,700/ha. This relative stability contrasts with the slight increase observed at the national level over the same period. The number of annual transactions is regular, around 700 sales per year, testifying to an active and relatively fluid market.

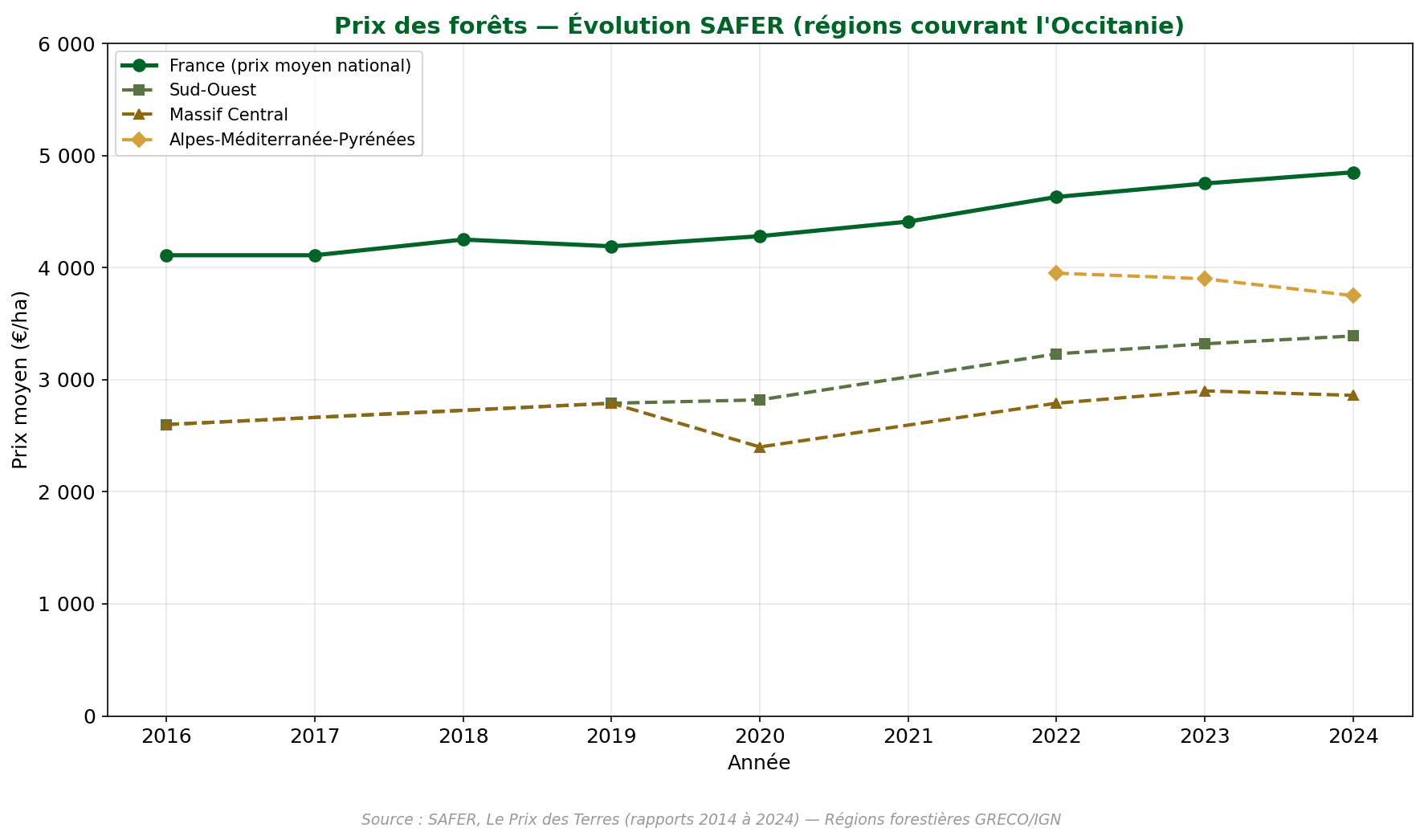

Data published annually by the SAFER Group in their "Le Prix des Terres" report allow the Occitan market to be placed in a multi-year perspective. SAFER's forest regions do not correspond to administrative regions: Occitanie covers territories belonging mainly to three SAFER forest regions: "Sud-Ouest", "Massif Central", and "Alpes-Méditerranée-Pyrénées".

| SAFER Forest Region | 2019 | 2020 | 2022 | 2023 | 2024 | Evol. 2019-2024 |

|---|---|---|---|---|---|---|

| Sud-Ouest | 2,790 €/ha | 2,820 €/ha | 3,230 €/ha | 3,320 €/ha | 3,390 €/ha | +21.5% |

| Massif Central | 2,790 €/ha | 2,400 €/ha | 2,790 €/ha | 2,900 €/ha | 2,860 €/ha | +2.5% |

| Alpes-Méditerranée-Pyrénées | — | — | 3,950 €/ha | 3,900 €/ha | 3,750 €/ha | — |

| France (national average price) | 4,190 €/ha | 4,280 €/ha | 4,630 €/ha | 4,750 €/ha | 4,850 €/ha | +15.8% |

Source: SAFER, Le Prix des Terres (2014 to 2024 reports). Forest regions based on GRECO/IGN divisions.

Evolution of forest prices — SAFER, regions covering Occitanie — Source: SAFER, Le Prix des Terres

The three forest regions covering Occitanie show price levels significantly lower than the national SAFER average (€4,850/ha in 2024). The "Sud-Ouest" is the most dynamic area with a progression of +21.5% between 2019 and 2024. The "Massif Central", which covers Lozère, Aveyron, and part of Lot, remains the most accessible area with an average price of €2,860/ha in 2024. The "Alpes-Méditerranée-Pyrénées" zone, which includes the Pyrenean and Mediterranean departments, shows a recent decline (from €3,950 to €3,750/ha between 2022 and 2024).

Discrepancies between DVF figures (analyzed by ma-propriete.fr) and SAFER prices are expected: the two sources use different methodologies, geographical scopes, and filters. Nevertheless, major trends converge: Occitanie remains one of the French regions where forest prices are most affordable.

Occitanie has thirteen departments with very varied forest characteristics. From the Pyrenean foothills to the Lot causses, from the Mediterranean garrigues to the plain forests of Gers, prices reflect this geographical and silvicultural diversity. Here is the detail of statistics by department.

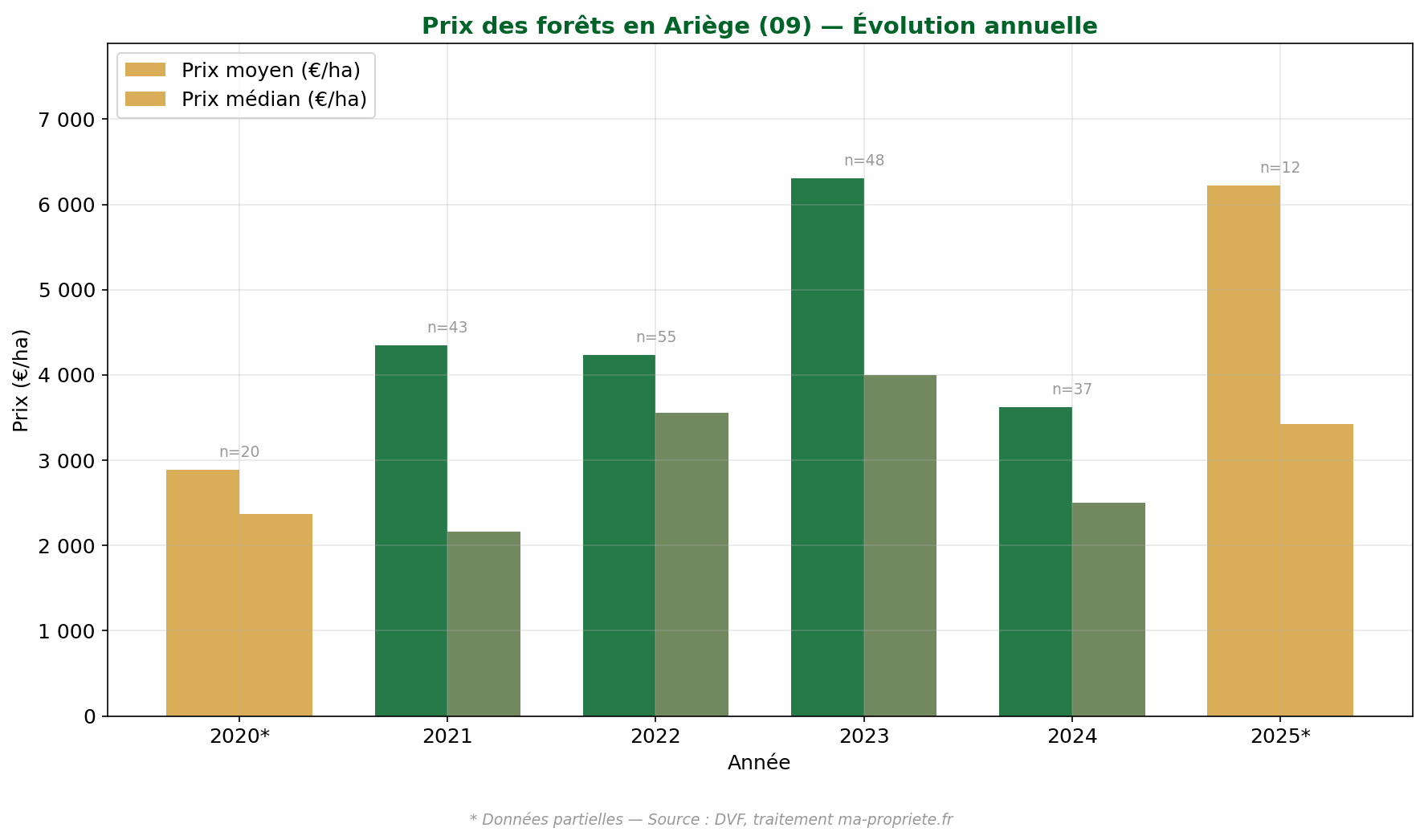

In the first half of 2025 (partial data, interpret with caution), the median price in Ariège stands at €3,429/ha for 12 transactions. This low number of sales limits the statistical significance of this figure.

In 2024 (full reference year), the median price was €2,505/ha for 37 transactions, with an average price of €3,623/ha. Ariège ranks among the most accessible departments in the region. This price level is explained by the predominance of mountain forests (beech-fir forests of the central Pyrenees), often located in areas with steep terrain, making them less easy to harvest. The median surface area of sold plots is 3.41 hectares, slightly lower than the regional median.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 20 | 2,888 | 2,366 | 967 | 9,363 |

| 2021 | 43 | 4,345 | 2,167 | 1,037 | 22,563 |

| 2022 | 55 | 4,239 | 3,558 | 1,054 | 13,800 |

| 2023 | 48 | 6,312 | 4,004 | 1,103 | 25,397 |

| 2024 | 37 | 3,623 | 2,505 | 1,165 | 11,821 |

| 2025* | 12 | 6,220 | 3,429 | 1,308 | 23,341 |

* Partial data. Source: DVF, ma-propriete.fr processing.

Forest prices in Ariège (09) — Source: DVF, ma-propriete.fr processing

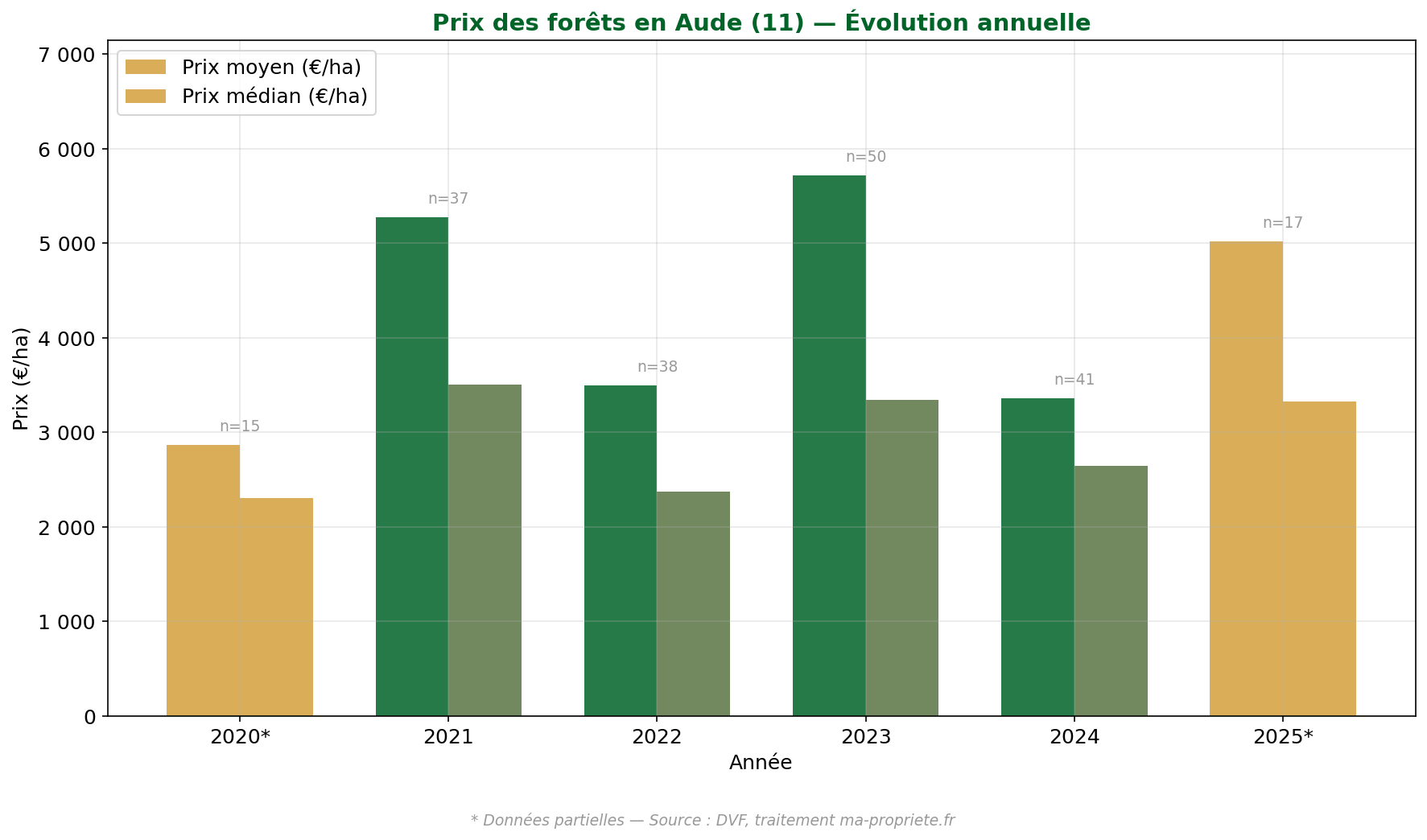

In the first half of 2025 (partial data, interpret with caution), the median price in Aude reached €3,327/ha for 17 transactions.

In 2024, the median price was €2,646/ha for 41 sales, with an average price of €3,356/ha. Aude is among the most affordable departments in Occitanie. Its forest massif is divided between the resinous forests of the Corbières and the Montagne Noire, and the drier scrublands of the coastal hinterland. The median surface area of 5.84 hectares in 2024 is significantly higher than the regional median, reflecting a market oriented towards larger plots.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 15 | 2,863 | 2,305 | 536 | 6,590 |

| 2021 | 37 | 5,277 | 3,500 | 1,039 | 23,532 |

| 2022 | 38 | 3,496 | 2,375 | 1,111 | 11,543 |

| 2023 | 50 | 5,714 | 3,340 | 588 | 31,176 |

| 2024 | 41 | 3,356 | 2,646 | 900 | 8,364 |

| 2025* | 17 | 5,020 | 3,327 | 986 | 18,963 |

* Partial data. Source: DVF, ma-propriete.fr processing.

Forest prices in Aude (11) — Source: DVF, ma-propriete.fr processing

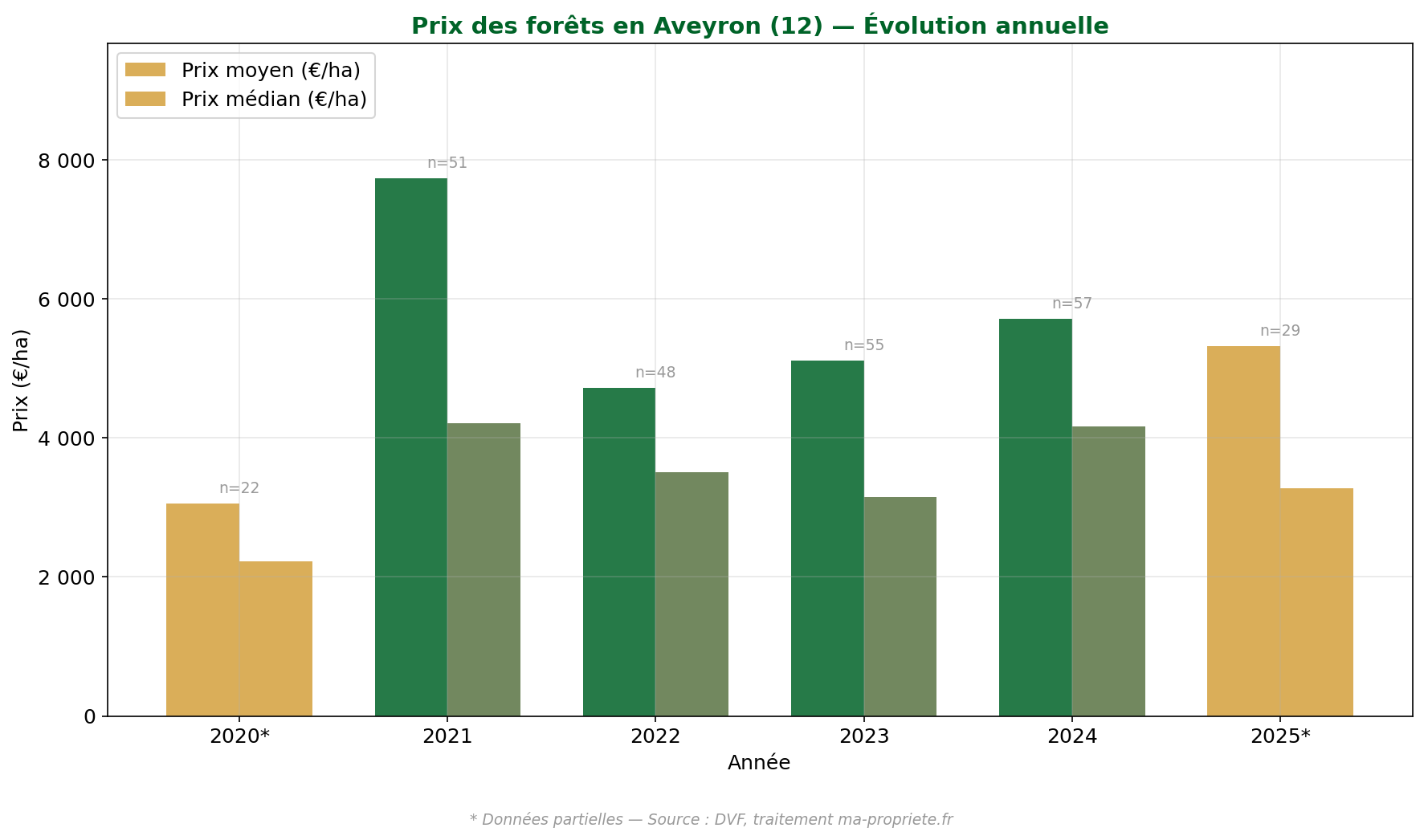

In the first half of 2025 (partial data, interpret with caution), the median price in Aveyron was €3,274/ha for 29 transactions.

In 2024, the median price stood at €4,160/ha for 57 sales, with an average price of €5,716/ha. Aveyron presents a relatively dynamic market, driven by the diversity of its forest environments: limestone causses covered with oak forests, Ségala and Lévézou plateaus dominated by conifers, and more productive valleys. The department totaled 262 transactions over the 2020-2025 period, a respectable volume given the market size.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 22 | 3,056 | 2,224 | 788 | 7,181 |

| 2021 | 51 | 7,740 | 4,214 | 936 | 38,995 |

| 2022 | 48 | 4,719 | 3,504 | 894 | 15,556 |

| 2023 | 55 | 5,118 | 3,151 | 944 | 33,000 |

| 2024 | 57 | 5,716 | 4,160 | 1,004 | 21,891 |

| 2025* | 29 | 5,325 | 3,274 | 803 | 18,928 |

* Partial data. Source: DVF, ma-propriete.fr processing.

Forest prices in Aveyron (12) — Source: DVF, ma-propriete.fr processing

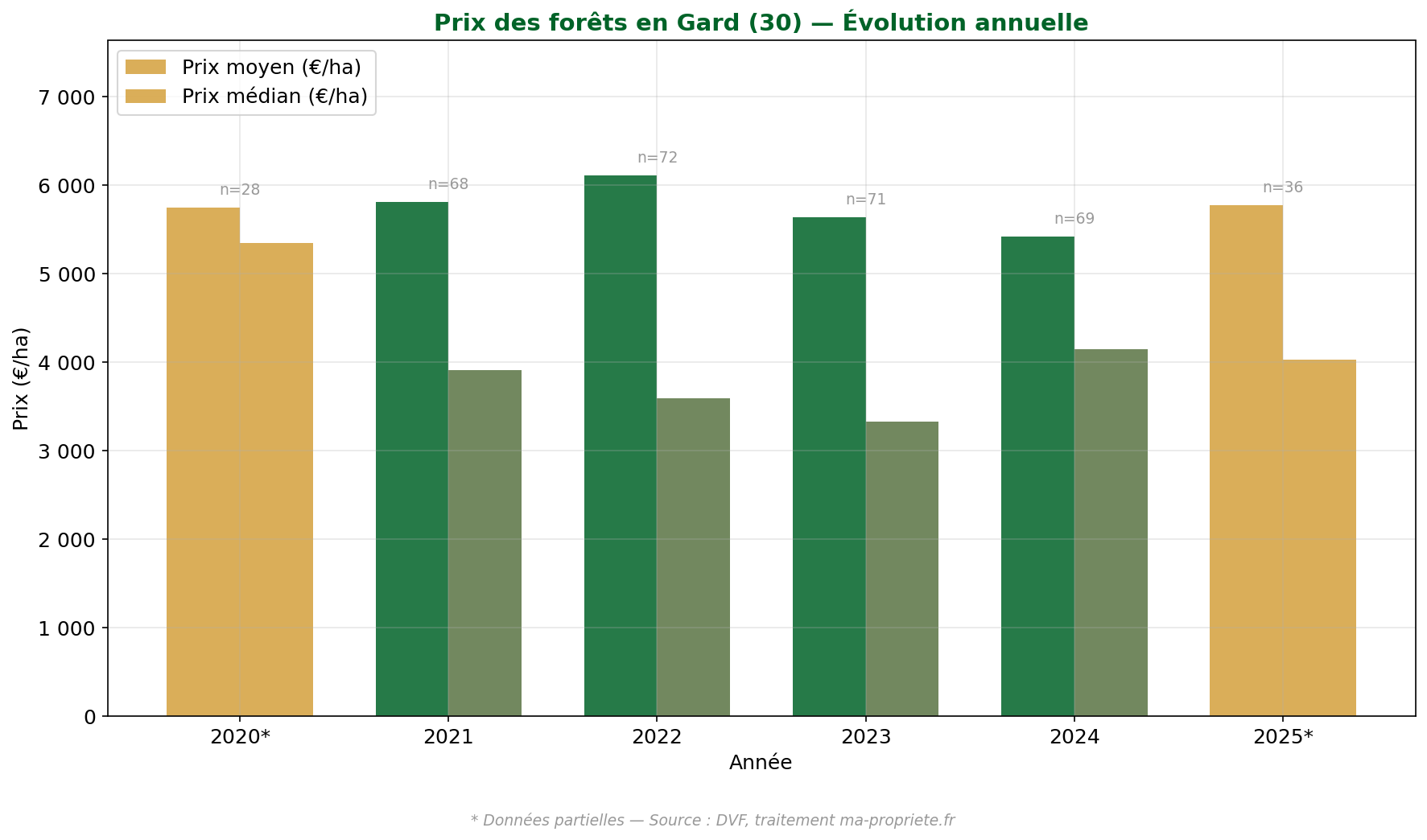

In the first half of 2025 (partial data, interpret with caution), the median price in Gard stands at €4,025/ha for 36 transactions.

In 2024, the median price was €4,146/ha for 69 sales, with an average price of €5,421/ha. Gard is in the upper part of the regional ranking. Its forest heritage is marked by holm oak and kermes oak scrublands in the south, and by denser forests of chestnut and conifers in the Gard Cévennes to the north. Proximity to Nîmes and coastal urban areas exerts noticeable land pressure on certain plots, contributing to higher prices. The department totaled 344 sales over the period, one of the highest volumes in the region.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 28 | 5,744 | 5,349 | 1,004 | 14,845 |

| 2021 | 68 | 5,808 | 3,907 | 872 | 21,442 |

| 2022 | 72 | 6,106 | 3,591 | 1,024 | 37,463 |

| 2023 | 71 | 5,633 | 3,328 | 1,026 | 29,104 |

| 2024 | 69 | 5,421 | 4,146 | 654 | 15,286 |

| 2025* | 36 | 5,775 | 4,025 | 800 | 20,374 |

* Partial data. Source: DVF, ma-propriete.fr processing.

Forest prices in Gard (30) — Source: DVF, ma-propriete.fr processing

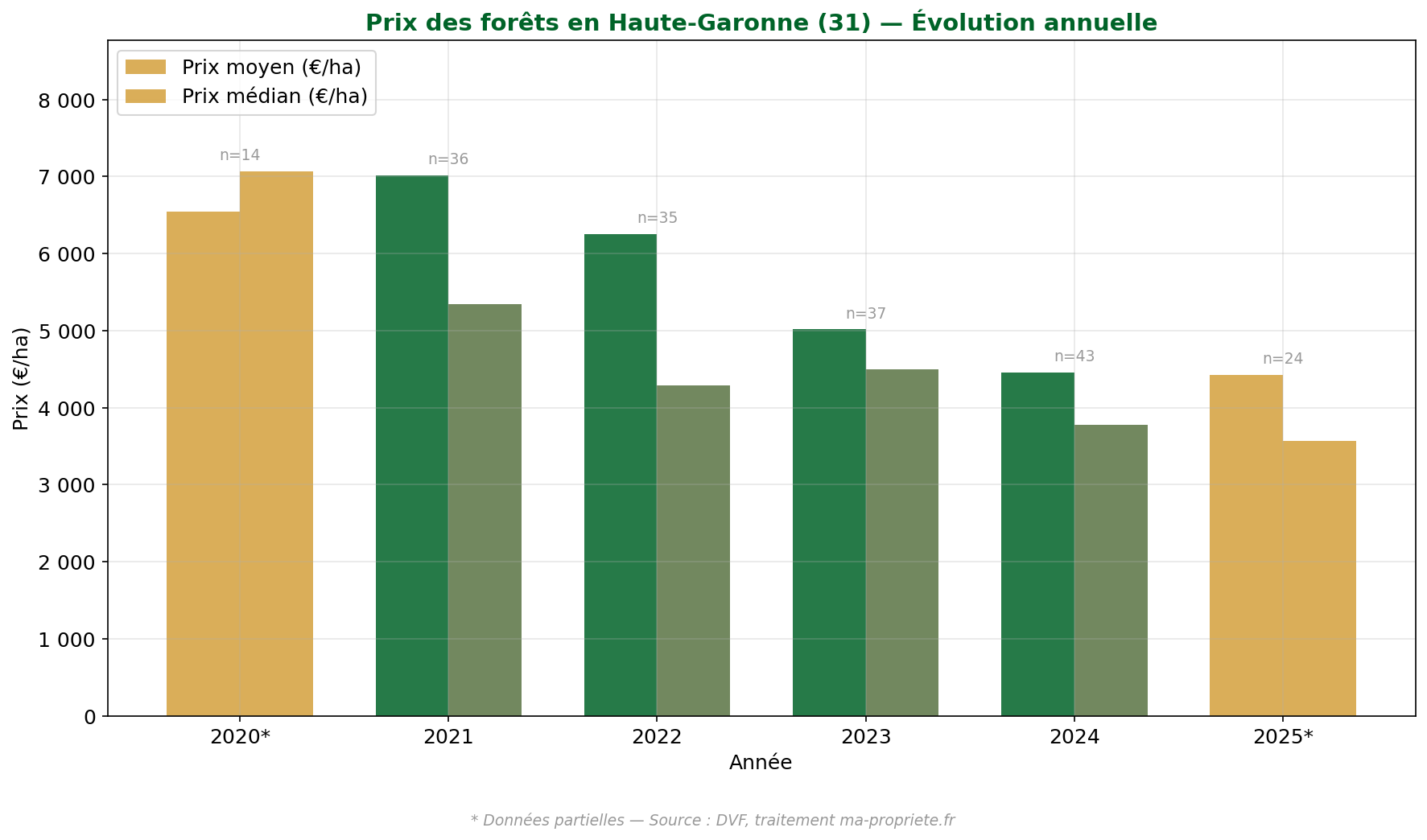

In the first half of 2025 (partial data, interpret with caution), the median price in Haute-Garonne was €3,567/ha for 24 transactions.

In 2024, the median price stood at €3,776/ha for 43 sales, with an average price of €4,458/ha. Haute-Garonne presents an atypical profile for Occitanie: land pressure from the Toulouse urban area is felt on plain and hillside woodlands, while mountain forests in Comminges (beech, fir) remain more accessible. The department shows a marked downward trend over the analyzed period: the median price fell from €7,068/ha in 2020 to €3,776/ha in 2024, although the low number of transactions in 2020 (14) limits the robustness of this comparison.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 14 | 6,542 | 7,068 | 1,386 | 13,085 |

| 2021 | 36 | 7,010 | 5,342 | 2,110 | 30,000 |

| 2022 | 35 | 6,255 | 4,292 | 1,000 | 34,485 |

| 2023 | 37 | 5,014 | 4,500 | 1,504 | 13,391 |

| 2024 | 43 | 4,458 | 3,776 | 1,402 | 11,820 |

| 2025* | 24 | 4,425 | 3,567 | 1,567 | 10,000 |

* Partial data. Source: DVF, ma-propriete.fr processing.

Forest prices in Haute-Garonne (31) — Source: DVF, ma-propriete.fr processing

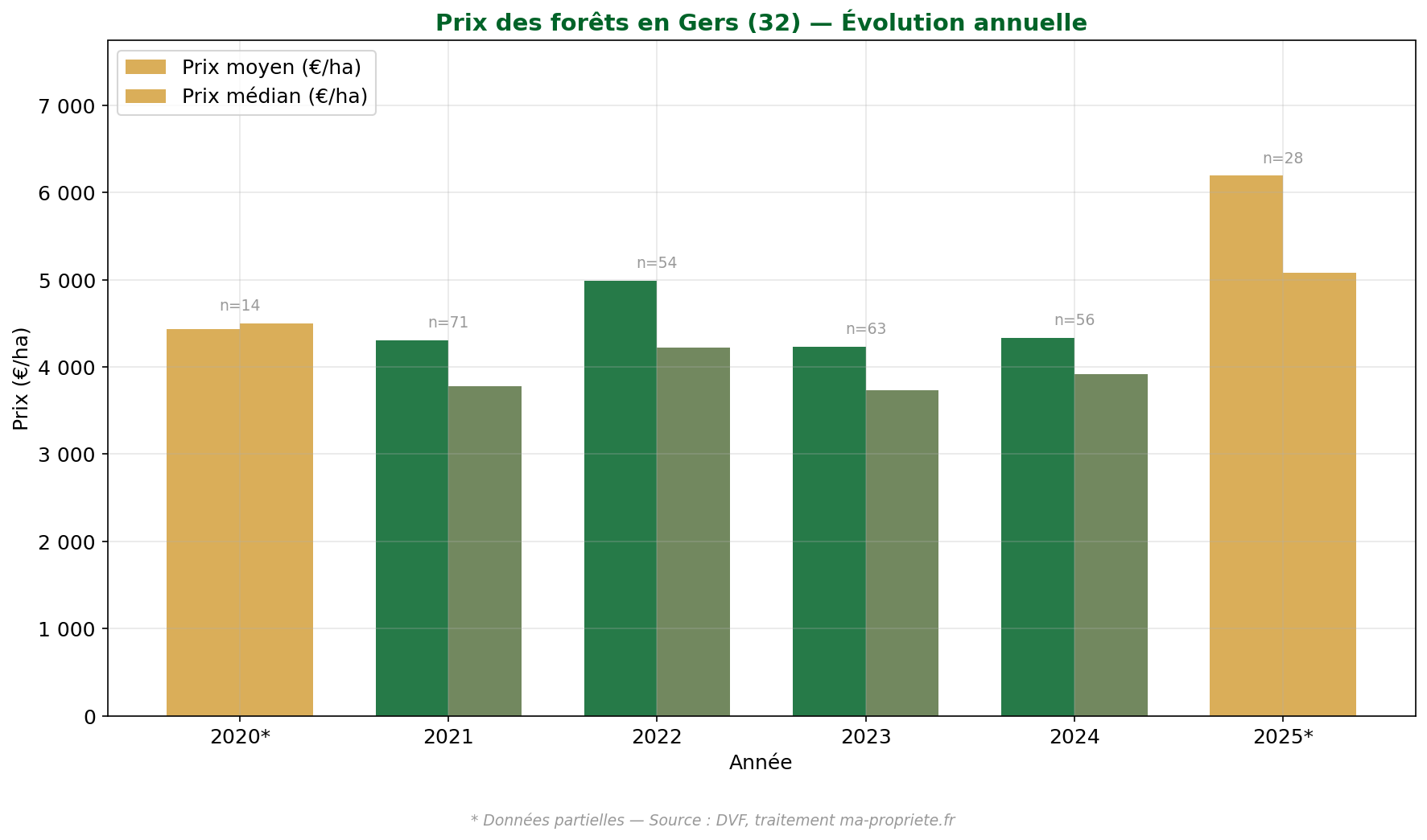

In the first half of 2025 (partial data, interpret with caution), the median price in Gers reached €5,076/ha for 28 transactions, a level significantly higher than previous years.

In 2024, the median price was €3,912/ha for 56 sales, with an average price of €4,335/ha. Gers is a department of hills whose woodlands, consisting mainly of oak forests and coppice, remain modest in size. The minimum observed price is high (€1,800/ha in 2024), reflecting a relatively homogeneous market with few very low-priced plots. Gers totaled 286 sales over the 2020-2025 period, a significant figure relative to the department's forest area.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 14 | 4,431 | 4,501 | 1,792 | 7,937 |

| 2021 | 71 | 4,306 | 3,780 | 1,583 | 11,881 |

| 2022 | 54 | 4,991 | 4,217 | 1,552 | 14,567 |

| 2023 | 63 | 4,230 | 3,734 | 1,500 | 10,713 |

| 2024 | 56 | 4,335 | 3,912 | 1,800 | 8,694 |

| 2025* | 28 | 6,192 | 5,076 | 2,110 | 12,682 |

* Partial data. Source: DVF, ma-propriete.fr processing.

Forest prices in Gers (32) — Source: DVF, ma-propriete.fr processing

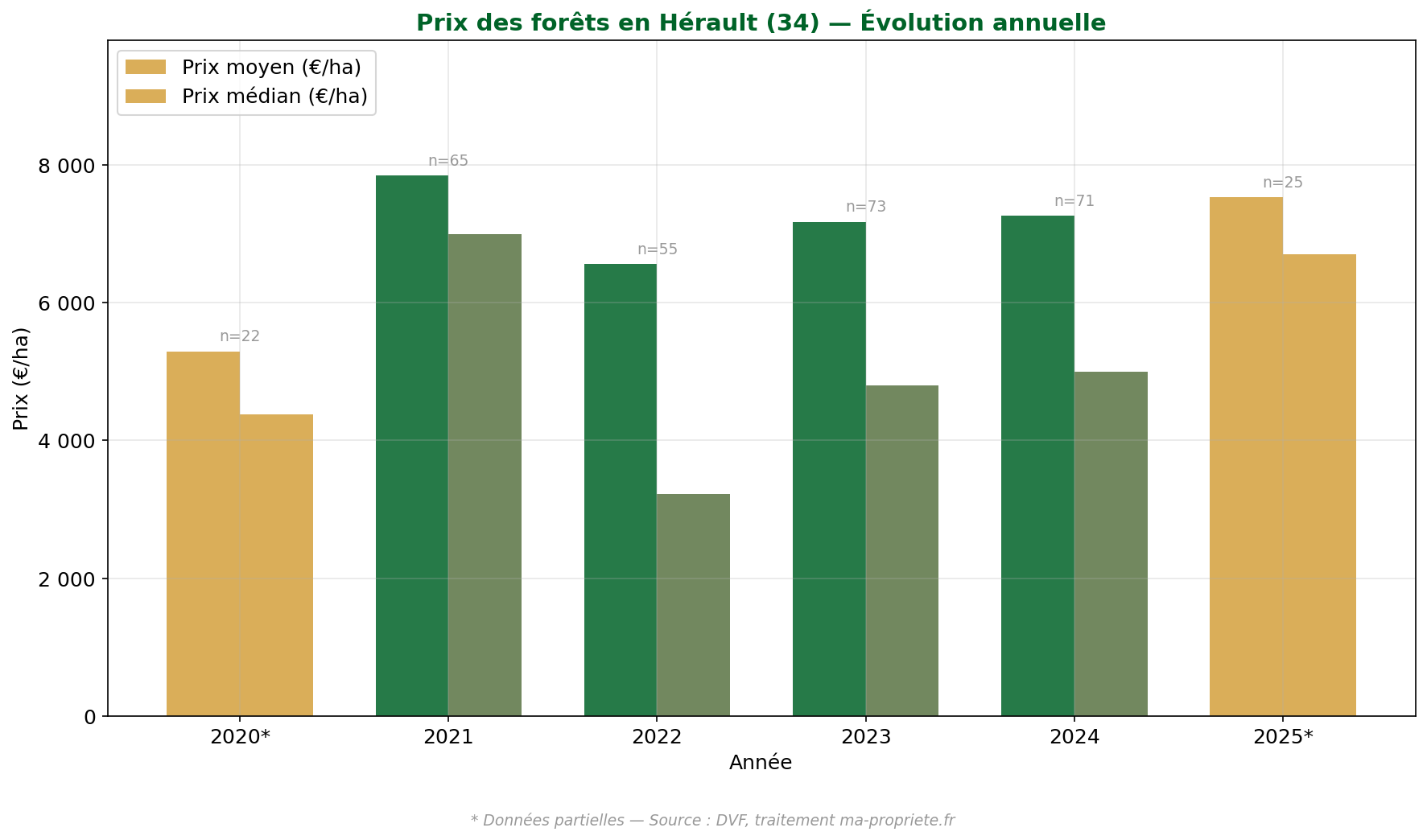

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Hérault reached €6,711/ha for 25 transactions, confirming the high market positioning of this department.

In 2024, the median price was €5,000/ha for 71 sales, with an average price of €7,270/ha. Hérault is the most expensive department in Occitanie for purchasing a forest. This price level is explained by land pressure from the Montpellier metropolitan area and the coastline, which increases the value of wooded plots as leisure or protection land. Holm oak scrubland (garrigues) dominates the forest cover, but the north of the department (Espinouse mountains, Haut-Languedoc) also houses more productive forests of beech and conifers.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 22 | 5,297 | 4,379 | 1,016 | 16,644 |

| 2021 | 65 | 7,849 | 7,000 | 1,392 | 28,895 |

| 2022 | 55 | 6,564 | 3,222 | 988 | 29,596 |

| 2023 | 73 | 7,177 | 4,804 | 1,002 | 25,000 |

| 2024 | 71 | 7,270 | 5,000 | 789 | 36,036 |

| 2025* | 25 | 7,534 | 6,711 | 1,057 | 17,953 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Hérault (34) — Source: DVF, processed by ma-propriete.fr

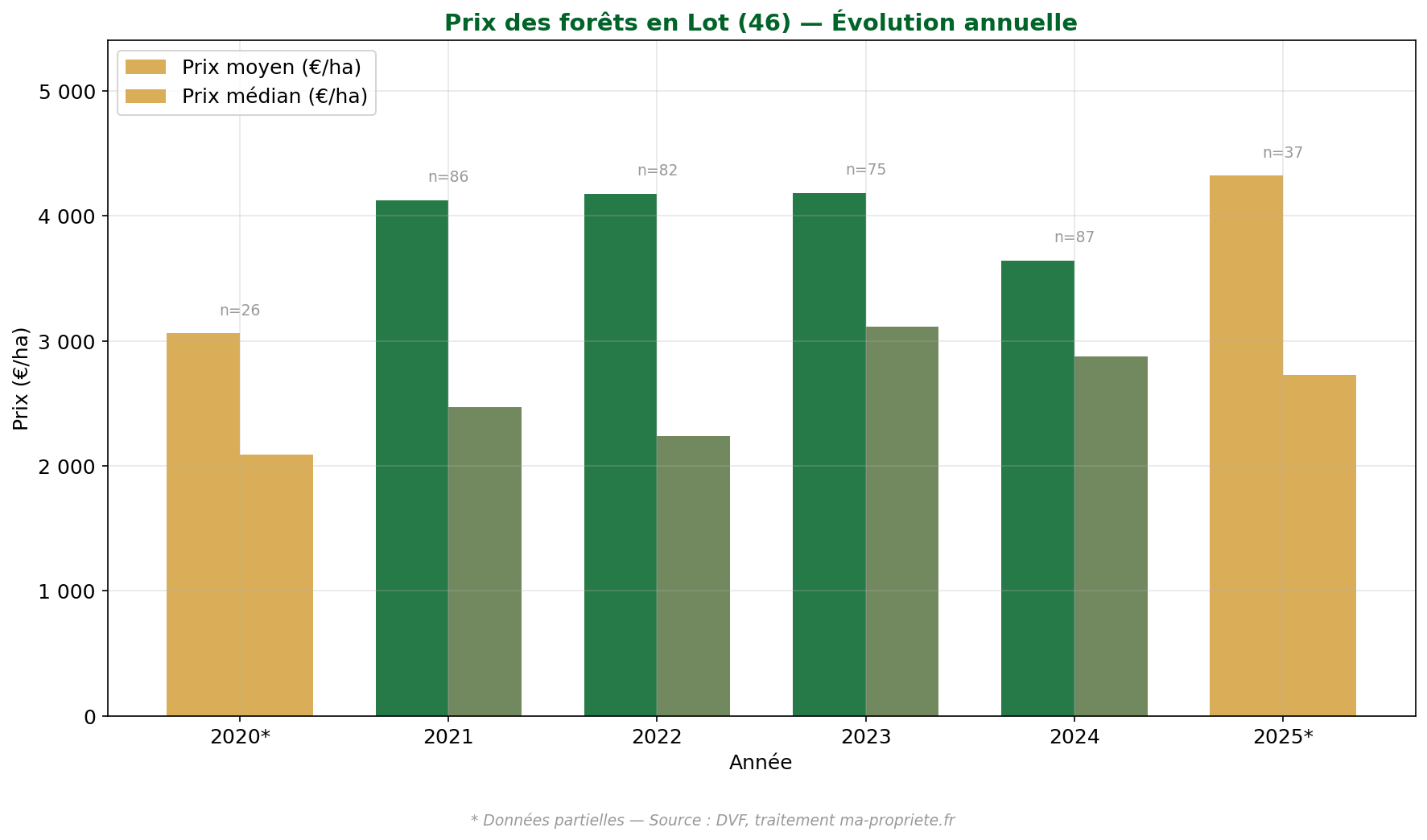

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Lot was €2,728/ha for 37 transactions.

In 2024, the median price stood at €2,873/ha for 87 sales, with an average price of €3,644/ha. Lot is one of the most active departments in the region in terms of the number of sales (393 over the period). Its landscape of limestone plateaus (causses) is covered with pubescent oak forests and coppice, often low-yielding in terms of timber. These forests nevertheless attract a diverse buyer profile, including hunting estate owners, secondary residents, and long-term investors. Price levels remain among the most accessible in the region.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 26 | 3,059 | 2,089 | 886 | 11,621 |

| 2021 | 86 | 4,127 | 2,472 | 825 | 20,537 |

| 2022 | 82 | 4,177 | 2,235 | 887 | 19,390 |

| 2023 | 75 | 4,184 | 3,114 | 819 | 21,070 |

| 2024 | 87 | 3,644 | 2,873 | 755 | 28,215 |

| 2025* | 37 | 4,322 | 2,728 | 759 | 14,299 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Lot (46) — Source: DVF, processed by ma-propriete.fr

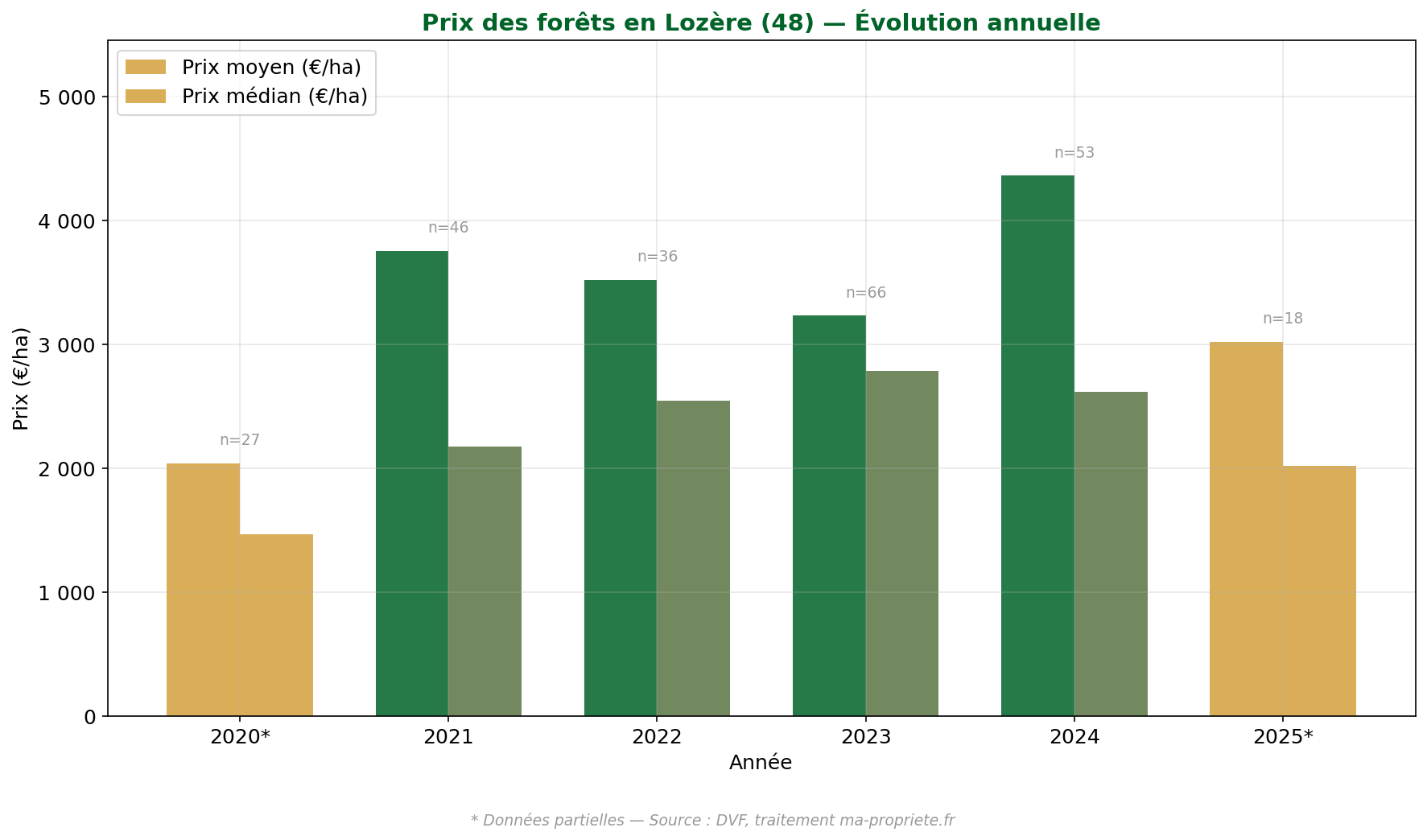

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Lozère was €2,017/ha for 18 transactions.

In 2024, the median price stood at €2,616/ha for 53 sales, with an average price of €4,359/ha. Lozère is the cheapest department in Occitanie — and one of the most affordable in France — for purchasing a hectare of forest. This positioning is explained by the distance from major urban centers, the very rugged terrain (Cévennes, Margeride, Aubrac), and the predominance of mountain conifers (spruce, Scots pine, fir) or chestnut trees. The areas sold are the largest in the region, with a median of 5.16 hectares over the entire period, reflecting a market focused on silvicultural management.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 27 | 2,037 | 1,465 | 755 | 5,397 |

| 2021 | 46 | 3,752 | 2,175 | 920 | 23,189 |

| 2022 | 36 | 3,520 | 2,544 | 1,032 | 12,819 |

| 2023 | 66 | 3,229 | 2,781 | 735 | 12,063 |

| 2024 | 53 | 4,359 | 2,616 | 813 | 45,980 |

| 2025* | 18 | 3,017 | 2,017 | 760 | 11,603 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Lozère (48) — Source: DVF, processed by ma-propriete.fr

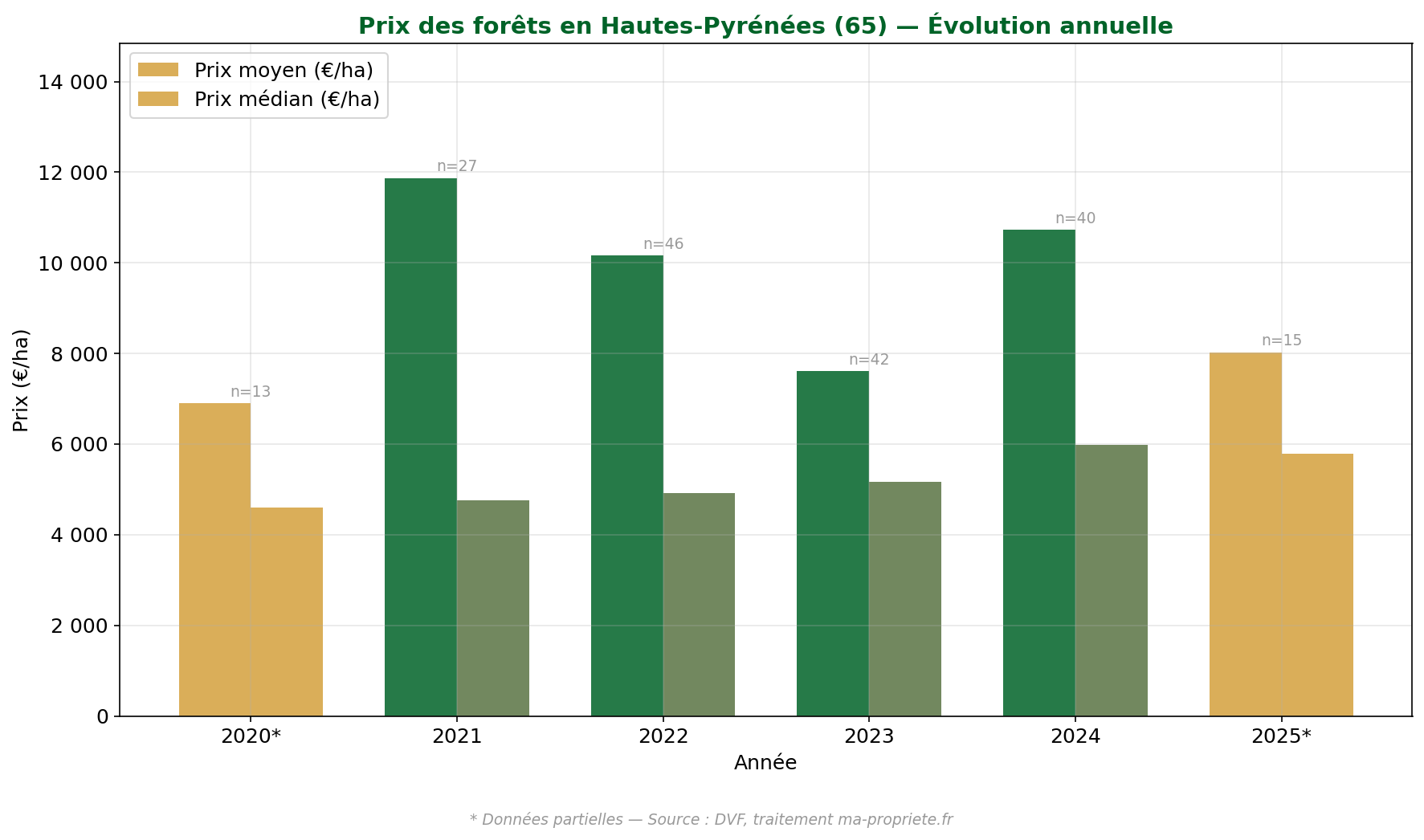

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Hautes-Pyrénées was €5,795/ha for 15 transactions.

In 2024, the median price stood at €5,974/ha for 40 sales, with a very high average price of €10,725/ha. Hautes-Pyrénées stands out for the considerable gap between the average and median price, the largest in the region. This discrepancy is explained by the presence of a few transactions at exceptional unit prices (the maximum price reached €59,292/ha in 2024), likely related to small plots in spa or tourist areas. Mountain forests (beech, fir) make up the bulk of the forest range. The median area is the smallest in the region (2.14 hectares), confirming a market dominated by small plots.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 13 | 6,900 | 4,608 | 1,200 | 23,602 |

| 2021 | 27 | 11,874 | 4,759 | 1,581 | 51,047 |

| 2022 | 46 | 10,158 | 4,917 | 1,228 | 45,637 |

| 2023 | 42 | 7,610 | 5,165 | 2,000 | 30,306 |

| 2024 | 40 | 10,725 | 5,974 | 1,939 | 59,292 |

| 2025* | 15 | 8,023 | 5,795 | 988 | 53,252 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Hautes-Pyrénées (65) — Source: DVF, processed by ma-propriete.fr

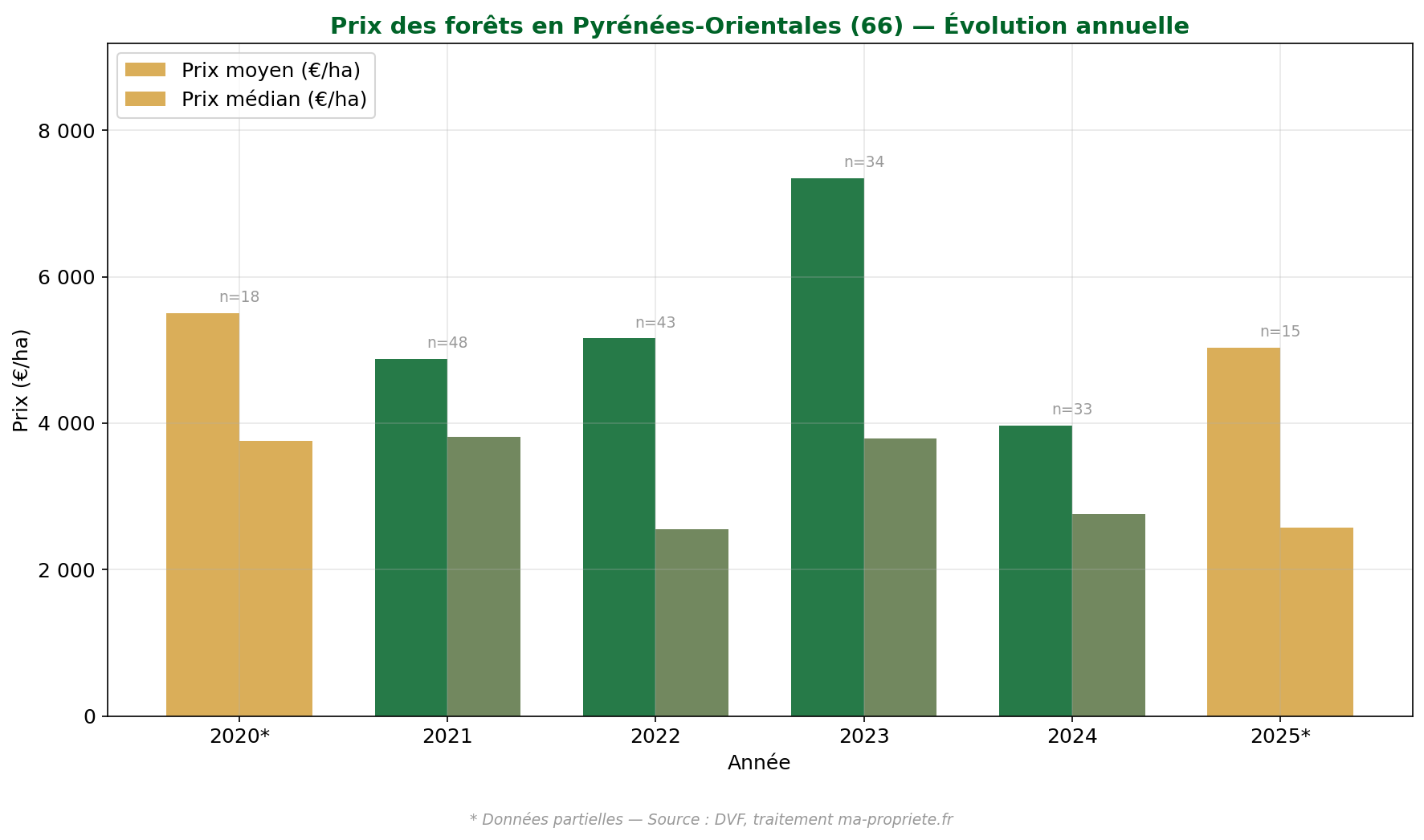

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Pyrénées-Orientales was €2,569/ha for 15 transactions.

In 2024, the median price stood at €2,761/ha for 33 sales, with an average price of €3,971/ha. Pyrénées-Orientales presents a highly contrasted market, reflecting the department's geography: dry Mediterranean forests of the Roussillon plain, the Albères scrubland, and mountain forests of Canigou and Capcir. Prices fluctuate significantly from year to year, reflecting a narrow market where a few atypical transactions can substantially alter statistics. The median surface area (4.76 hectares over the period) is higher than the regional median.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 18 | 5,507 | 3,760 | 780 | 27,360 |

| 2021 | 48 | 4,880 | 3,810 | 830 | 15,446 |

| 2022 | 43 | 5,158 | 2,551 | 940 | 19,431 |

| 2023 | 34 | 7,351 | 3,792 | 857 | 29,345 |

| 2024 | 33 | 3,971 | 2,761 | 1,026 | 11,565 |

| 2025* | 15 | 5,033 | 2,569 | 824 | 22,370 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Pyrénées-Orientales (66) — Source: DVF, processed by ma-propriete.fr

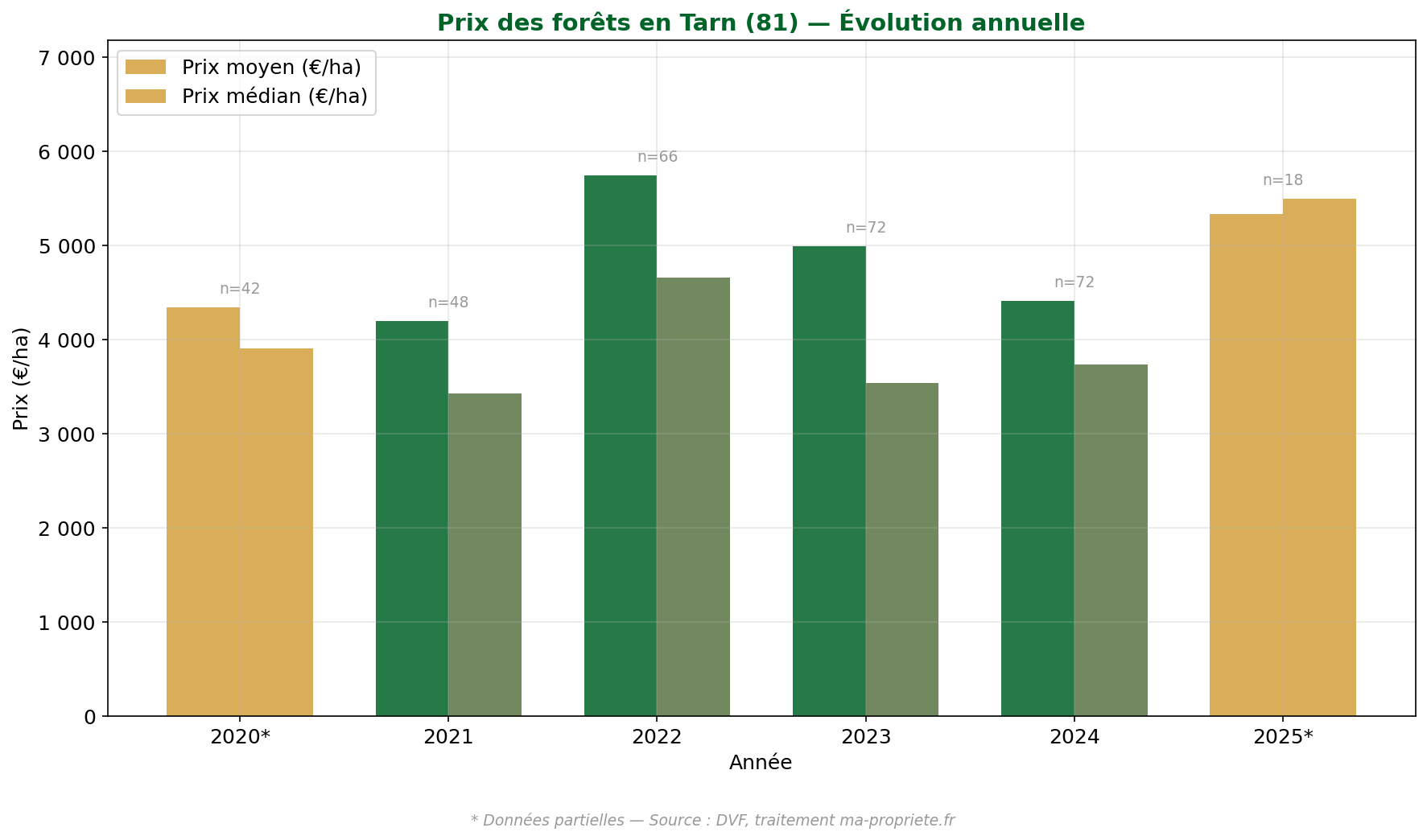

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Tarn was €5,492/ha for 18 transactions, a high level compared to previous years.

In 2024, the median price stood at €3,732/ha for 72 sales, with an average price of €4,406/ha. Tarn is one of the most active departments in the region in terms of transaction volume (318 over the period). Its forest landscape is dominated by oak and chestnut forests in the Montagne Noire and Sidobre areas, while the Gaillac hillsides house more fragmented woodlands. Prices remain relatively stable year after year, a sign of a well-established market.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 42 | 4,342 | 3,905 | 1,283 | 12,218 |

| 2021 | 48 | 4,192 | 3,426 | 1,165 | 12,053 |

| 2022 | 66 | 5,738 | 4,653 | 1,434 | 18,048 |

| 2023 | 72 | 4,989 | 3,538 | 1,118 | 16,403 |

| 2024 | 72 | 4,406 | 3,732 | 1,150 | 11,572 |

| 2025* | 18 | 5,332 | 5,492 | 1,721 | 9,884 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Tarn (81) — Source: DVF, processed by ma-propriete.fr

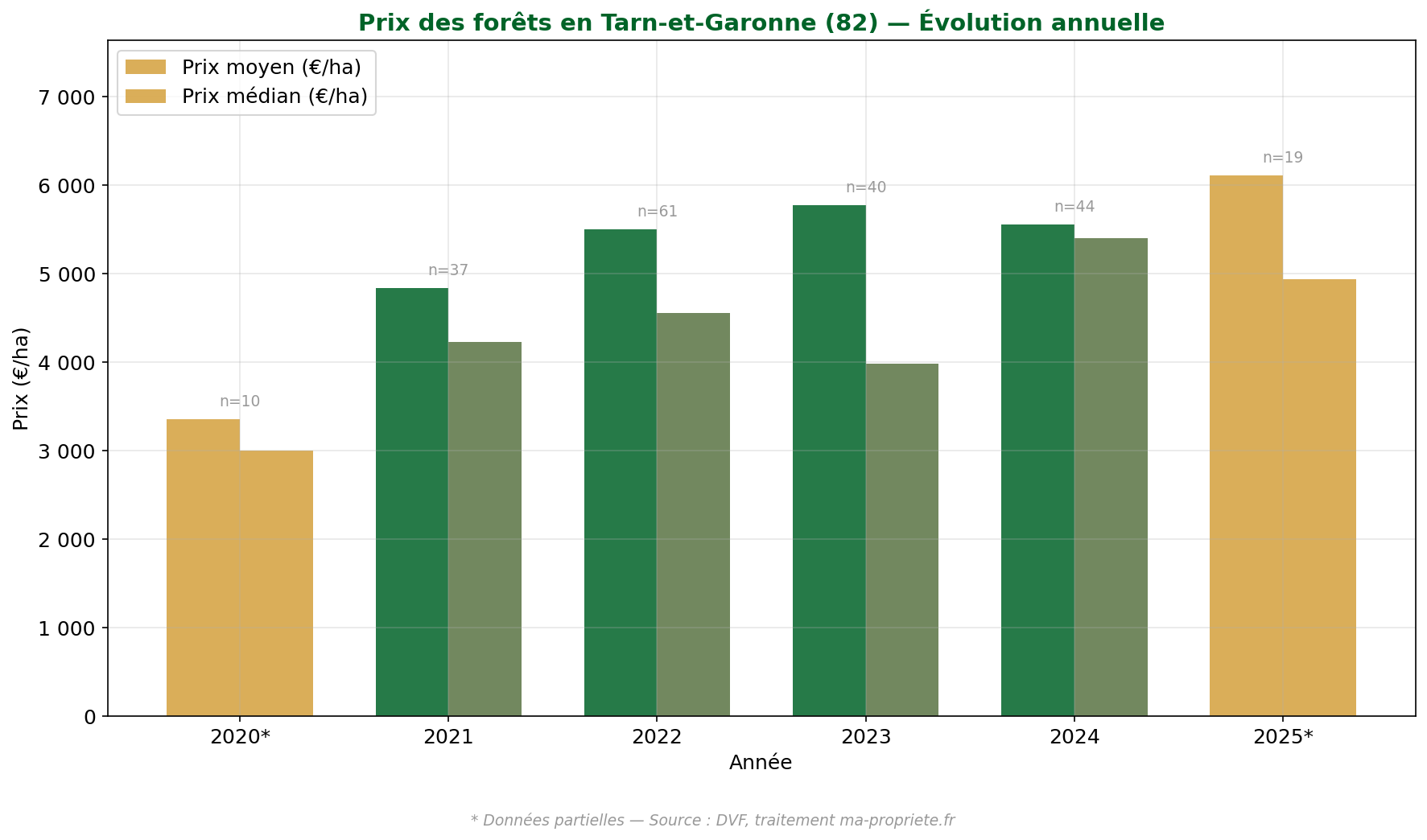

In the first half of 2025 (partial data, to be interpreted with caution), the median price in Tarn-et-Garonne was €4,931/ha for 19 transactions.

In 2024, the median price stood at €5,400/ha for 44 sales, with an average price of €5,553/ha. Tarn-et-Garonne shows one of the highest prices in western Occitanie, which may be surprising for a department of plains and hillsides. This level is partly explained by the dominance of small wooded plots in an agricultural context, where demand is supported by neighboring owners. The department shows a clearly upward trajectory over the period, with a median price rising from €3,001/ha in 2020 to €5,400/ha in 2024.

| Year | No. of sales | Average price (€/ha) | Median price (€/ha) | Min price | Max price |

|---|---|---|---|---|---|

| 2020* | 10 | 3,353 | 3,001 | 1,500 | 5,414 |

| 2021 | 37 | 4,832 | 4,224 | 1,432 | 14,416 |

| 2022 | 61 | 5,497 | 4,549 | 1,065 | 13,649 |

| 2023 | 40 | 5,773 | 3,976 | 1,384 | 20,782 |

| 2024 | 44 | 5,553 | 5,400 | 1,199 | 11,992 |

| 2025* | 19 | 6,103 | 4,931 | 2,004 | 20,806 |

* Partial data. Source: DVF, processed by ma-propriete.fr.

Forest prices in Tarn-et-Garonne (82) — Source: DVF, processed by ma-propriete.fr

The statistics presented in this article are derived from the analysis of the DVF (Demandes de Valeurs Foncières) database, published by the Ministry of Economy. This database lists all real estate and land transfers carried out in France, except for Alsace and Moselle (which fall under the Land Book).

Our processing covers the period from July 1, 2020, to June 30, 2025. The selected transactions meet the following criteria: cadastral nature of woods or forests, area greater than or equal to 1 hectare, and price per hectare between €500 and €100,000. To limit the influence of extreme values on indicators, the 50% of prices furthest from the median are excluded within each department. This "trimming" method yields statistics more representative of the current market.

The median price is the preferred indicator in our analysis: it separates transactions into two equal halves and is more resistant than the average to extreme values. The average price is provided as a supplement, with the caution that it is mechanically pulled upward by high unit price transactions.

Several limitations should be kept in mind when reading these statistics.

Alsace and Moselle do not appear in the DVF database. Transactions carried out in these three departments are therefore not included in our analyses.

DVF data does not always clearly distinguish "pure" forest properties from mixed properties (forest + farmland, forest + buildings). Filtering by cadastral nature helps limit this bias, but some transactions may include a non-forest component that influences the price per hectare.

DVF data does not cover sales of company shares, such as Forestry Groups (GF or GFI). However, these structures hold a significant portion of French forest heritage, particularly large estates with a Simple Management Plan. Prices practiced in the transfer of Forestry Group shares therefore escape our analysis and belong to a distinct market with different valuation logic (liquidity discount, tax advantages, forest yield).

The year 2020 only covers the second half (July to December), and the year 2025 only the first half (January to June). These two partial periods are not comparable to the full years 2021-2024 in terms of volume and representativeness.

SAFER statistics and those from our DVF processing show notable differences, explaining the price discrepancies observed.

The first point concerns geographical positioning: SAFER uses a division into forest regions based on the IGN's GRECOs (Large Ecological Regions), which do not correspond to administrative regions. Thus, administrative Occitanie is divided between the "South-West," "Massif Central," and "Alps-Mediterranean-Pyrenees" forest regions, making direct comparison impossible.

Methodologically, SAFER relies on a hedonic model integrating property characteristics (area, location, station quality), while our approach is based on a descriptive statistical analysis of raw DVF transactions. Furthermore, SAFER only includes non-built forest properties of 1 hectare or more, with a threshold of 80% of areas recorded as woods, coppice, high forest, and conifers in the cadastre.

Despite these differences, both sources converge on major trends: the Occitanie region remains one of the most accessible areas in France for forest acquisition, and prices are progressing moderately over the recent period.

With a median price of €3,632/ha in 2024, Occitanie confirms its status as one of the most accessible French regions for acquiring a forest estate. The diversity of forest contexts — from the Pyrenees to the Lot limestone plateaus, from Mediterranean scrubland to the Aveyron plateaus — translates into a wide range of prices between departments, offering varied opportunities to different buyer profiles.

The regional market is active and steady, with approximately 700 transactions per year and stable median prices in recent years. For buyers looking for significant acreage on a controlled budget, the departments of Lozère, Lot, Ariège, and Aude offer the most favorable conditions. Buyers seeking leisure plots or urban proximity will lean more toward Hérault or Hautes-Pyrénées, where prices reflect more sustained land pressure.

Find all our analyses on the price of forests in France and view forests for sale in Occitanie on ma-propriete.fr.

| Region | Article |

|---|---|

| Auvergne-Rhône-Alpes | Read the article |

| Bourgogne-Franche-Comté | Read the article |

| Brittany | Read the article |

| Centre-Val de Loire | Read the article |

| Grand Est | Read the article |

| Hauts-de-France | Read the article |

| Île-de-France | Read the article |

| Normandy | Read the article |

| Nouvelle-Aquitaine | Read the article |

| Occitanie | You are here |

| Pays de la Loire | Read the article |

| Provence-Alpes-Côte d'Azur | Read the article |