Brittany is a region whose forest heritage, although modest in area compared to the large massifs of southern or eastern France, occupies a unique place in the land landscape. With approximately 400,000 hectares of woodland — representing a forest cover rate of around 15% — the region ranks among the least forested territories in France. Broadleaf species largely dominate: pedunculate oak, beech, and chestnut structure most of the stands, complemented by resinous plantations (maritime pine on the moors, Sitka spruce and Douglas fir in inland areas). Private forest ownership represents the vast majority of the surface area, and the fragmentation of plots is a marked characteristic of Breton forest land.

This article presents a detailed analysis of forest prices in Brittany, based on the exploitation of 1,180 transactions recorded in the official DVF (Demandes de Valeurs Foncières) database between July 1, 2020, and June 30, 2025. Data for the 1st half of 2025 are included but must be interpreted with caution: they only cover half a year and are not directly comparable to full years. The year 2024, the last full year available, serves as a robust reference for structural analysis.

For a global view of the French forest market, consult our observatory of forest prices in France. You can also discover forest properties currently for sale, or browse the forest listings available in Brittany.

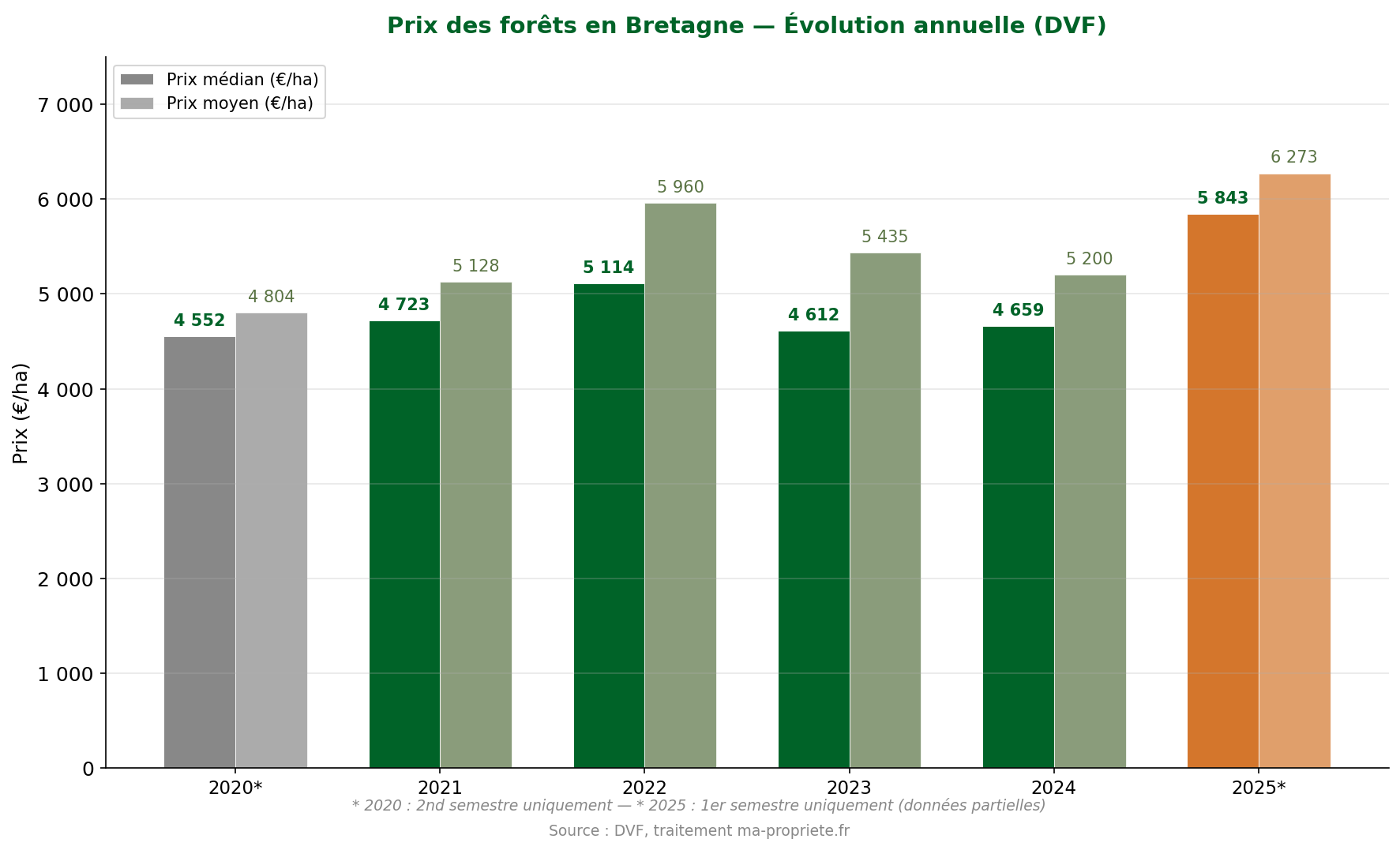

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Brittany stood at €5,843/ha, for an average price of €6,273/ha. This level, observed on only 104 transactions, marks an apparent increase compared to 2024. However, as the 1st half data only covers half a year, it cannot be directly compared to a full year and should be considered a preliminary signal.

For the reference year 2024 (full year, 225 transactions), the median price was €4,659/ha and the average price €5,200/ha. The median surface area of traded plots is 2.47 hectares, a figure that confirms the fragmentation of Breton forest land, significantly lower than the national average (3.3 hectares). Over the entire 2020-2025 period, Brittany shows a median price of €4,827/ha across 1,180 transactions, a level comparable to the national median (€4,765/ha).

The gap between the average price and the median price — approximately €600/ha in 2024 — remains moderate in Brittany. This gap reflects the influence of small plots sold at high unit prices, a common phenomenon in the forest markets of Western France. The median price, which divides transactions into two equal halves, remains the most representative indicator of the current market.

| Year | Nb of sales | Average price (€/ha) | Median price (€/ha) | Min price (€/ha) | Max price (€/ha) | Med. area (ha) |

|---|---|---|---|---|---|---|

| 2025* | 104 | 6,273 | 5,843 | 2,000 | 19,317 | 2.19 |

| 2024 | 225 | 5,200 | 4,659 | 978 | 14,847 | 2.47 |

| 2023 | 241 | 5,435 | 4,612 | 791 | 16,236 | 2.31 |

| 2022 | 248 | 5,960 | 5,114 | 1,010 | 20,557 | 2.32 |

| 2021 | 249 | 5,128 | 4,723 | 987 | 16,187 | 2.62 |

| 2020* | 113 | 4,804 | 4,552 | 1,082 | 15,201 | 2.98 |

* 2025: partial data (1st half only) — * 2020: partial data (2nd half only). Source: DVF, processing by ma-propriete.fr.

Annual evolution of forest prices in Brittany (2020-2025) — Source: DVF, processing by ma-propriete.fr

Over the four full years (2021 to 2024), the Breton median price fluctuated between €4,612 and €5,114/ha, without a clear upward trend. The year 2022 appeared as a peak (€5,114/ha), followed by a decline in 2023 and stabilization in 2024. The number of transactions is relatively stable, around 230 to 250 sales per year, testifying to a regular market in terms of volume.

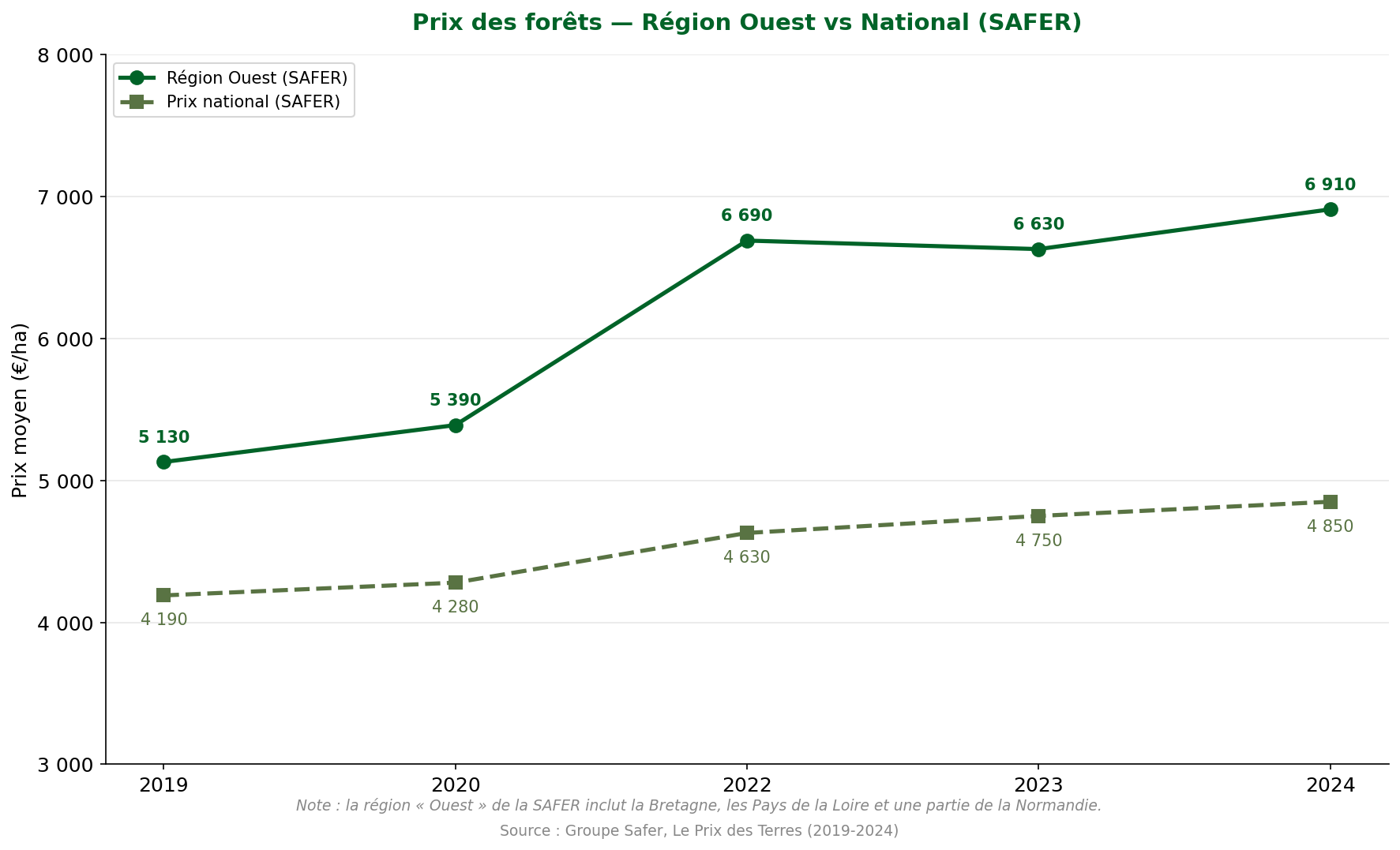

Data published by the Safer Group in its annual report Le Prix des Terres (Land Prices) allows the Breton market to be placed in a multi-year perspective. SAFER uses a division into forest regions different from administrative regions: Brittany is integrated into the "West" region, which also includes the Pays de la Loire and part of Normandy.

According to SAFER, the average price of forests in the West region stood at €6,910/ha in 2024, up +4.2% compared to 2023 (€6,630/ha). Over five years, the progression is remarkable: +34.7% between 2019 and 2024. This upward dynamic is significantly higher than the national average (+15.8% over the same period), confirming the growing attractiveness of forest land in the Greater West.

| Year | West Region (€/ha) | National Price (€/ha) | West / National Gap |

|---|---|---|---|

| 2024 | 6,910 | 4,850 | +42% |

| 2023 | 6,630 | 4,750 | +40% |

| 2022 | 6,690 | 4,630 | +44% |

| 2020 | 5,390 | 4,280 | +26% |

| 2019 | 5,130 | 4,190 | +22% |

Note: SAFER's "West" region (GRECO/IGN division) does not correspond exactly to administrative Brittany. It also includes the Pays de la Loire and part of Normandy. Source: Safer Group, Le Prix des Terres (2019-2024).

Evolution of forest prices — West Region vs National (SAFER, 2019-2024)

The price gap between the West region and the national average is widening year after year: from +22% in 2019 to +42% in 2024. This premium is explained by the quality of broadleaf stands in the West (productive oak forests), by land pressure linked to the residential attractiveness of Brittany and the Pays de la Loire, and by the scarcity of forest supply in this geographical area.

It should be noted that SAFER and DVF price levels are not directly comparable in absolute value: SAFER uses a hedonic model weighted by surface area, while our DVF analysis is based on effective transaction prices after statistical filtering. These methodological differences are detailed at the end of the article.

Brittany has four departments with distinct forest profiles. Morbihan concentrates the largest number of transactions, while Ille-et-Vilaine displays the highest prices. Finistère, more exposed to oceanic influences, presents the most moderate prices.

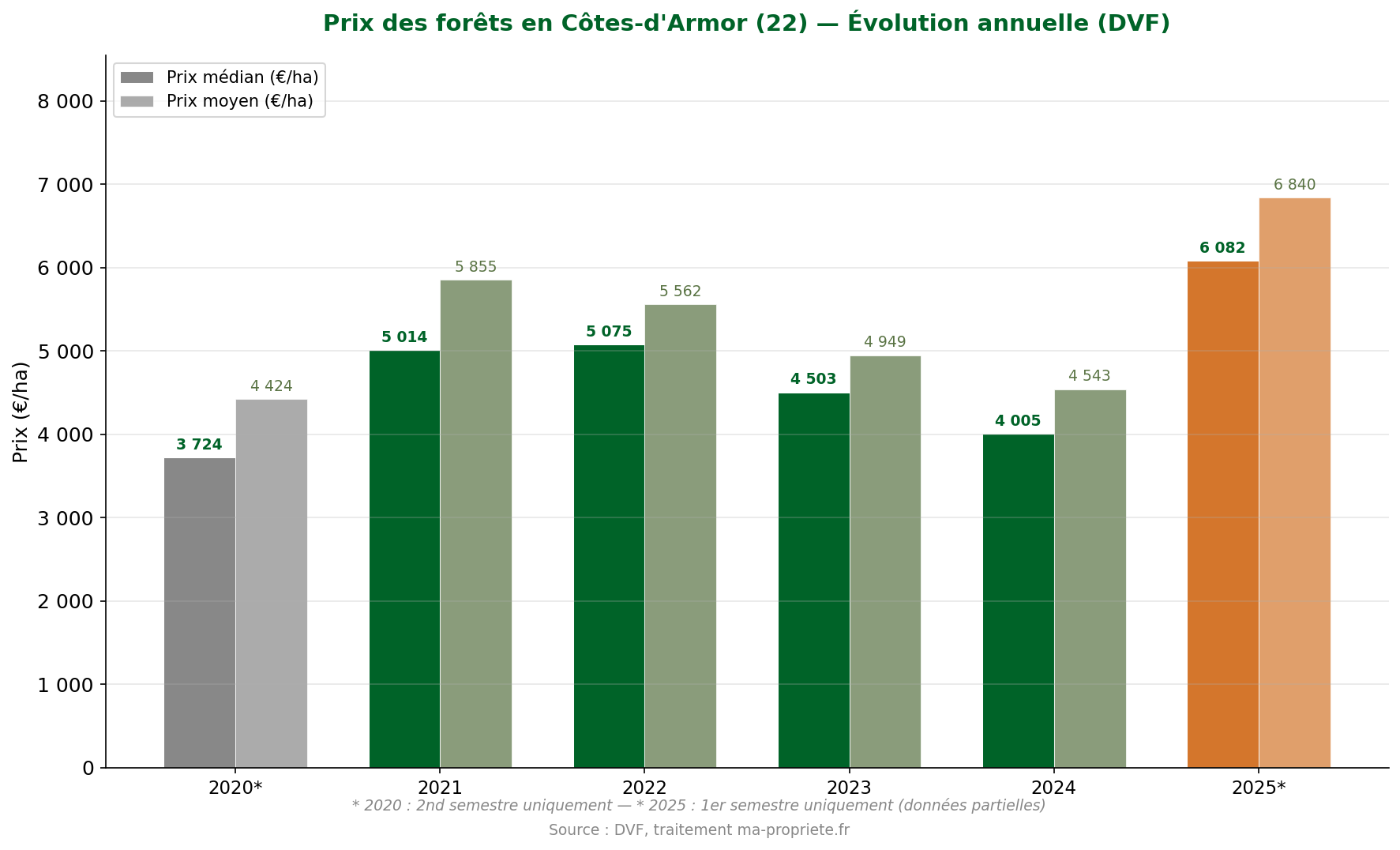

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Côtes-d'Armor reached €6,082/ha on 26 transactions, a level showing a clear apparent increase compared to 2024.

For the reference year 2024, the department showed a median price of €4,005/ha on 54 sales, for an average price of €4,543/ha. The median surface area is 2.26 hectares. Over the entire 2020-2025 period, the aggregated median price stood at €4,743/ha for 299 transactions, a level slightly lower than the regional average.

Côtes-d'Armor presents a forest massif dominated by broadleaf trees (oak, beech, chestnut), with some resinous woods in the interior sectors. The Beffou forest and the Coat-an-Noz forest are among the most notable massifs. The market is characterized by a supply of small fragmented plots, which explains the reduced median surface area of transactions.

| Year | Nb of sales | Average price (€/ha) | Median price (€/ha) | Min price (€/ha) | Max price (€/ha) |

|---|---|---|---|---|---|

| 2025* | 26 | 6,840 | 6,082 | 3,013 | 16,155 |

| 2024 | 54 | 4,543 | 4,005 | 1,952 | 9,879 |

| 2023 | 62 | 4,949 | 4,503 | 2,189 | 14,288 |

| 2022 | 68 | 5,562 | 5,075 | 2,302 | 20,197 |

| 2021 | 62 | 5,855 | 5,014 | 2,269 | 16,187 |

| 2020* | 27 | 4,424 | 3,724 | 2,616 | 7,949 |

* 2025: 1st half only — * 2020: 2nd half only. Source: DVF, processing by ma-propriete.fr.

Evolution of forest prices in Côtes-d'Armor (2020-2025) — Source: DVF, processing by ma-propriete.fr

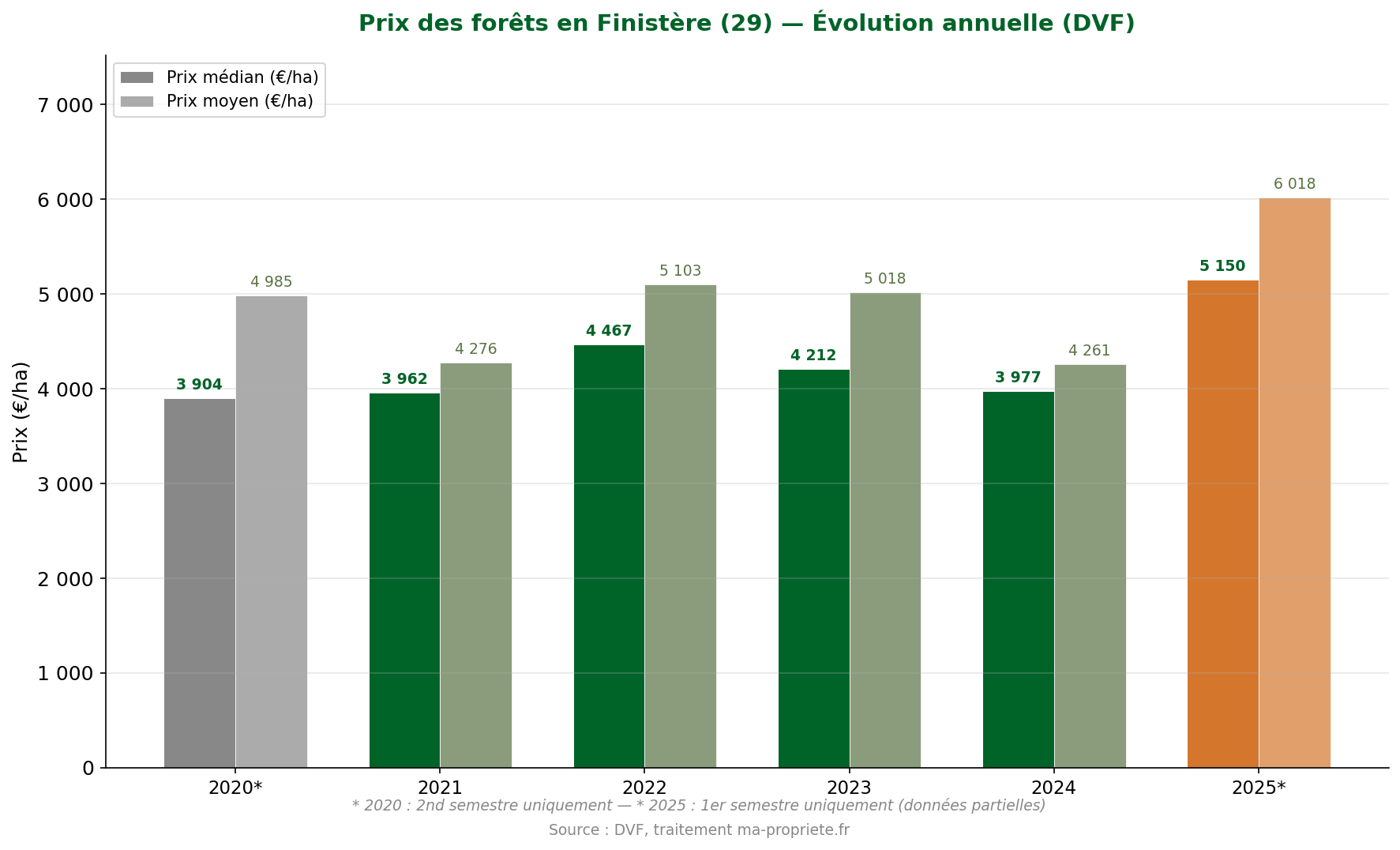

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Finistère stood at €5,150/ha on 18 transactions. This low volume invites a particularly cautious interpretation.

For the reference year 2024, Finistère recorded a median price of €3,977/ha for 54 sales, with an average price of €4,261/ha. It is the Breton department presenting the most accessible prices, with an aggregated median price of €4,077/ha over the 2020-2025 period (257 transactions).

Finistère is the western tip of Brittany, subject to the most marked oceanic influences. The climate, mild and humid, favors the growth of certain species, but the quality of the timber remains heterogeneous. Coastal woods are often small in size. In return, the interior of the department (Monts d'Arrée) offers more substantial massifs, dominated by broadleaf trees and resinous plantations. The ground price below the regional average is partly explained by the distance from the main demand basins and by the variable quality of the sites.

| Year | Nb of sales | Average price (€/ha) | Median price (€/ha) | Min price (€/ha) | Max price (€/ha) |

|---|---|---|---|---|---|

| 2025* | 18 | 6,018 | 5,150 | 3,032 | 11,250 |

| 2024 | 54 | 4,261 | 3,977 | 978 | 13,175 |

| 2023 | 50 | 5,018 | 4,212 | 791 | 14,999 |

| 2022 | 61 | 5,103 | 4,467 | 1,010 | 18,208 |

| 2021 | 55 | 4,276 | 3,962 | 987 | 11,659 |

| 2020* | 19 | 4,985 | 3,904 | 1,082 | 15,201 |

* 2025: 1st half only — * 2020: 2nd half only. Source: DVF, processing by ma-propriete.fr.

Evolution of forest prices in Finistère (2020-2025) — Source: DVF, processing by ma-propriete.fr

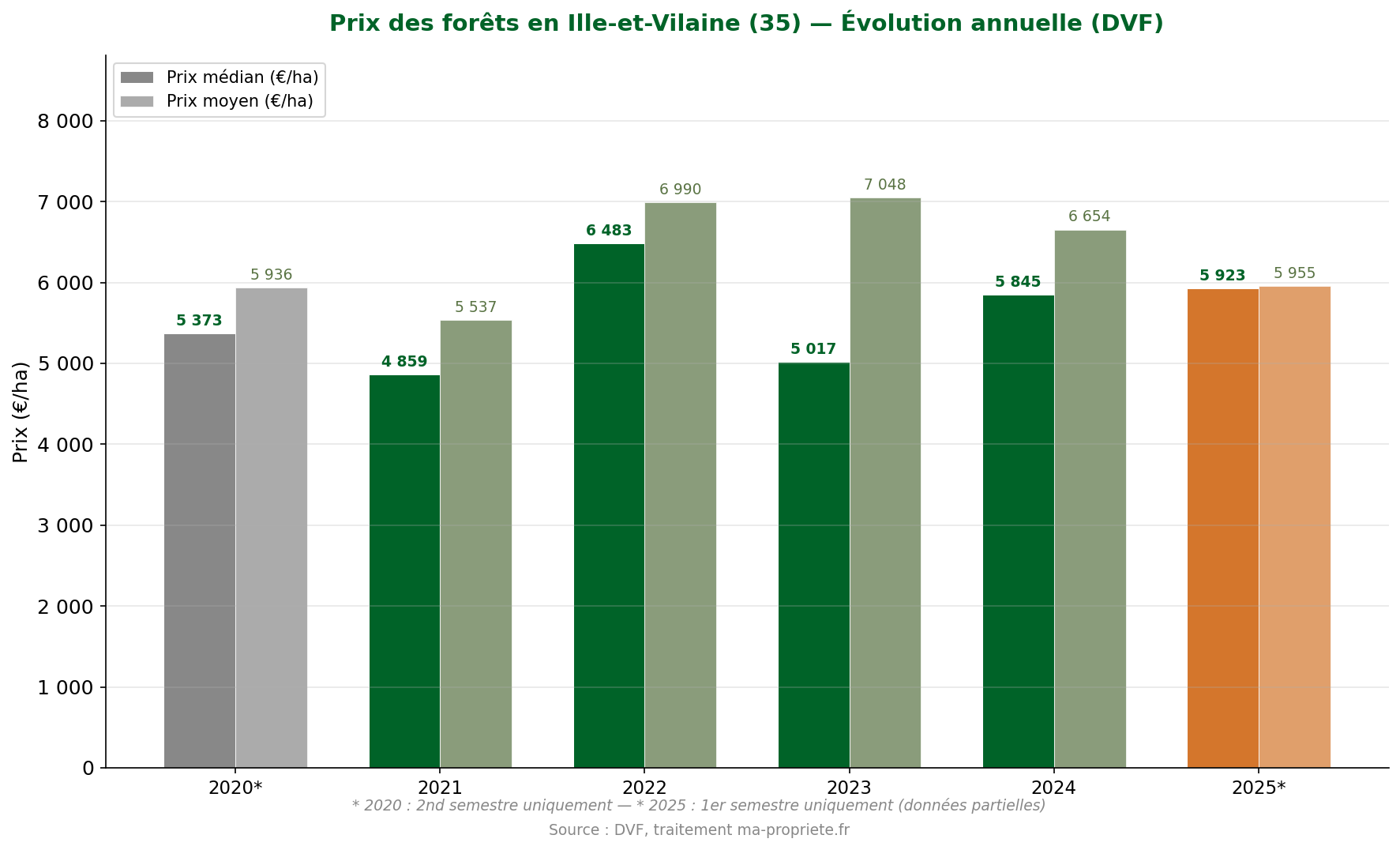

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Ille-et-Vilaine stood at €5,923/ha on 18 transactions.

For the reference year 2024, the department showed a median price of €5,845/ha for 36 sales, the highest in Brittany. The average price reached €6,654/ha. Over the 2020-2025 period, the aggregated median price was €5,534/ha for 178 transactions, clearly above the regional average (+14.6%).

Ille-et-Vilaine benefits from its proximity to Rennes, a dynamic metropolis whose attractiveness supports land demand, including for forest assets. The department's forests — Rennes forest, Paimpont forest (Brocéliande), Liffré forest — are renowned for their quality broadleaf stands (oak, beech). This combination of forest quality and land pressure explains the department's premium positioning. However, the number of transactions remains limited (36 in 2024), which calls for a cautious reading of price levels.

| Year | Nb of sales | Average price (€/ha) | Median price (€/ha) | Min price (€/ha) | Max price (€/ha) |

|---|---|---|---|---|---|

| 2025* | 18 | 5,955 | 5,923 | 3,232 | 10,711 |

| 2024 | 36 | 6,654 | 5,845 | 2,939 | 14,847 |

| 2023 | 33 | 7,048 | 5,017 | 2,550 | 15,744 |

| 2022 | 37 | 6,990 | 6,483 | 3,296 | 13,864 |

| 2021 | 42 | 5,537 | 4,859 | 2,000 | 10,991 |

| 2020* | 12 | 5,936 | 5,373 | 4,000 | 8,152 |

* 2025: 1st half only — * 2020: 2nd half only. Source: DVF, processing by ma-propriete.fr.

Evolution of forest prices in Ille-et-Vilaine (2020-2025) — Source: DVF, processing by ma-propriete.fr

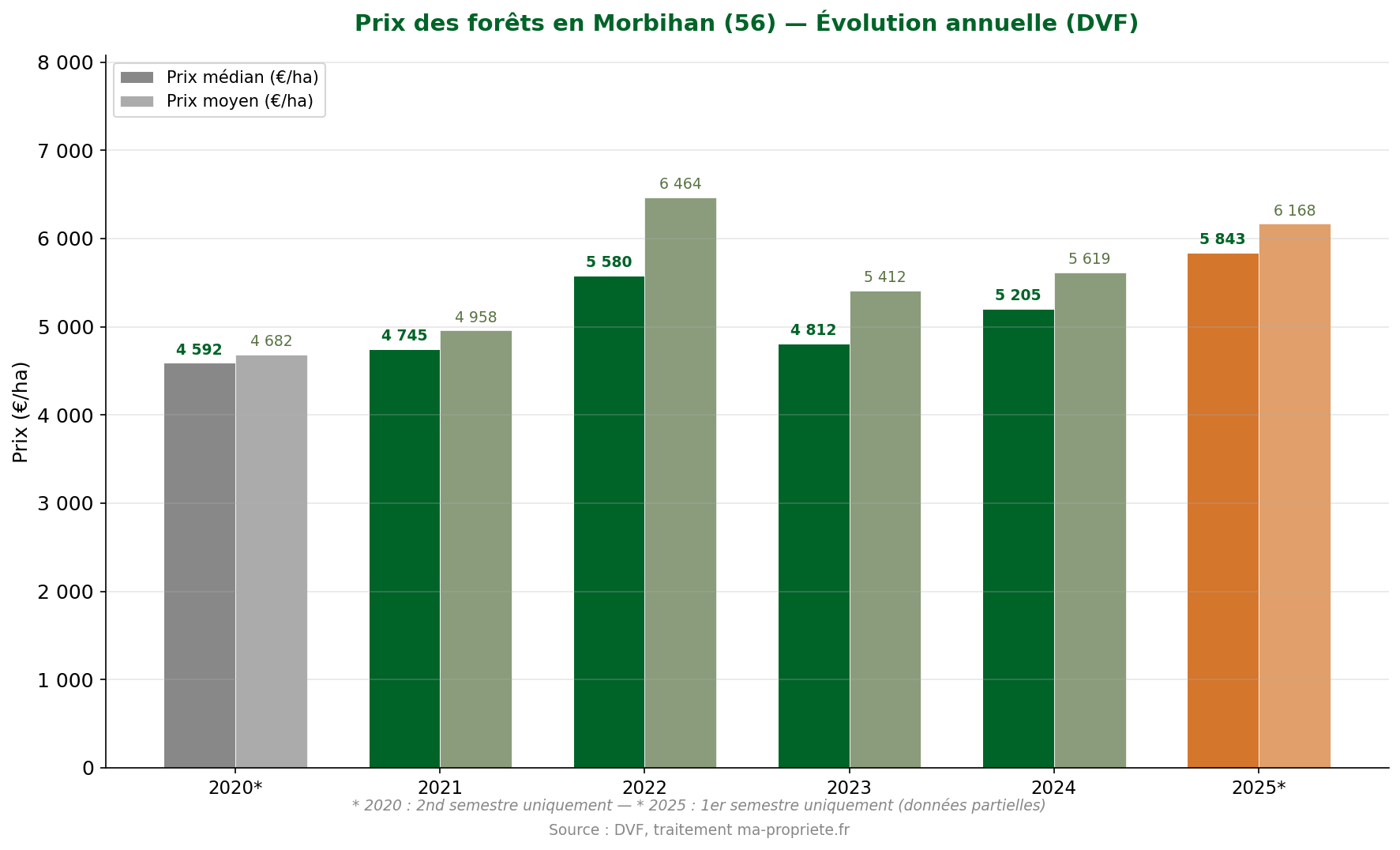

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Morbihan reached €5,843/ha on 42 transactions, a volume that offers a more solid statistical base than in other Breton departments for this beginning of the year.

For the reference year 2024, Morbihan recorded a median price of €5,205/ha for 81 sales, with an average price of €5,619/ha. It is the Breton department that concentrates the largest number of forest transactions over the entire period (446 sales, or 38% of the regional total). Over the 2020-2025 period, the aggregated median price reached €5,000/ha.

Morbihan has a varied forest heritage, between the wooded moors of the interior (Lanouée forest, Quénécan forest) and the coastal woods of the Gulf of Morbihan. Broadleaf species dominate (oak, beech, chestnut), with resinous stands (maritime pine) on the coastal fringe. Sustained demand is explained by the residential and tourist attractiveness of the department, which stimulates the market for leisure plots.

| Year | Nb of sales | Average price (€/ha) | Median price (€/ha) | Min price (€/ha) | Max price (€/ha) |

|---|---|---|---|---|---|

| 2025* | 42 | 6,168 | 5,843 | 2,000 | 19,317 |

| 2024 | 81 | 5,619 | 5,205 | 2,444 | 11,399 |

| 2023 | 96 | 5,412 | 4,812 | 1,777 | 16,236 |

| 2022 | 82 | 6,464 | 5,580 | 1,849 | 20,557 |

| 2021 | 90 | 4,958 | 4,745 | 1,701 | 9,710 |

| 2020* | 55 | 4,682 | 4,592 | 1,967 | 9,685 |

* 2025: 1st half only — * 2020: 2nd half only. Source: DVF, processing by ma-propriete.fr.

Evolution of forest prices in Morbihan (2020-2025) — Source: DVF, processing by ma-propriete.fr

The statistics presented in this article come from the DVF (Demandes de Valeurs Foncières) database, published in open data by the Ministry of the Economy. This database lists all real estate and land transfers for consideration carried out in France, with the exception of Alsace and Moselle (specific land regime).

To produce relevant indicators on the forest market, ma-propriete.fr applies a methodical filtering of the raw data:

This method produces a dataset of 31,383 transactions over the period from July 1, 2020, to June 30, 2025, covering 93 departments and representing 267,306 hectares exchanged for a value of 1.74 billion euros.

Despite its richness, the DVF database has several limitations that should be kept in mind:

Statistics published by the Safer Group in its annual report Le Prix des Terres are based on a distinct methodology:

The Breton forest market is distinguished by an intermediate price position on a national scale, a pronounced fragmentation of plots, and significant departmental gaps. Ille-et-Vilaine displays the highest prices, driven by the attractiveness of Rennes and the quality of its stands, while Finistère remains the most accessible department. Data for the 1st half of 2025, still partial, suggest an upward dynamic that will need to be confirmed with the full-year figures. For buyers and sellers alike, Brittany offers a range of forest situations — from small broadleaf leisure plots to productive inland woodlands — that justifies a case-by-case analysis, far beyond simple regional averages.

Find all of our analyses on forest prices in France, and discover forests currently for sale in Brittany on ma-propriete.fr.

| Region | Article |

|---|---|

| Auvergne-Rhône-Alpes | Forest prices in Auvergne-Rhône-Alpes |

| Bourgogne-Franche-Comté | Forest prices in Bourgogne-Franche-Comté |

| Brittany | Forest prices in Brittany |

| Centre-Val de Loire | Forest prices in Centre-Val de Loire |

| Corsica | Forest prices in Corsica |

| Grand Est | Forest prices in Grand Est |

| Hauts-de-France | Forest prices in Hauts-de-France |

| Île-de-France | Forest prices in Île-de-France |

| Normandy | Forest prices in Normandy |

| Nouvelle-Aquitaine | Forest prices in Nouvelle-Aquitaine |

| Occitanie | Forest prices in Occitanie |

| Pays de la Loire | Forest prices in Pays de la Loire |

| Provence-Alpes-Côte d'Azur | Forest prices in Provence-Alpes-Côte d'Azur |