Grand Est is one of the major forest regions in France. With nearly 1.9 million hectares of woodland, forests cover approximately 33% of the regional territory, a reforestation rate significantly higher than the national average (31%). The region is home to iconic massifs — Vosges, Argonne, Champagne, and Lorraine forests — which combine a great diversity of species: beech, sessile oak, Norway spruce, silver fir, Scots pine and, in the lowlands, ash and hornbeam. The timber industry has historically been a structural element here, with a primary processing industry (sawmills, paper mills) still very present in the Vosges and Lorraine.

This article analyzes forest prices in Grand Est based on the 2,526 transactions recorded in the DVF database (Demandes de Valeurs Foncières) between July 2020 and June 2025. Data for the 1st half of 2025 are included but remain partial and must be interpreted with caution. The year 2024, the most recent full year, constitutes the main reference for this analysis. Statistics are supplemented by data published by the SAFER Group on the "East" forest region.

Find all of our data on the French forest market in our observatory of forest prices in France, and consult the listings of forests for sale on ma-propriete.fr.

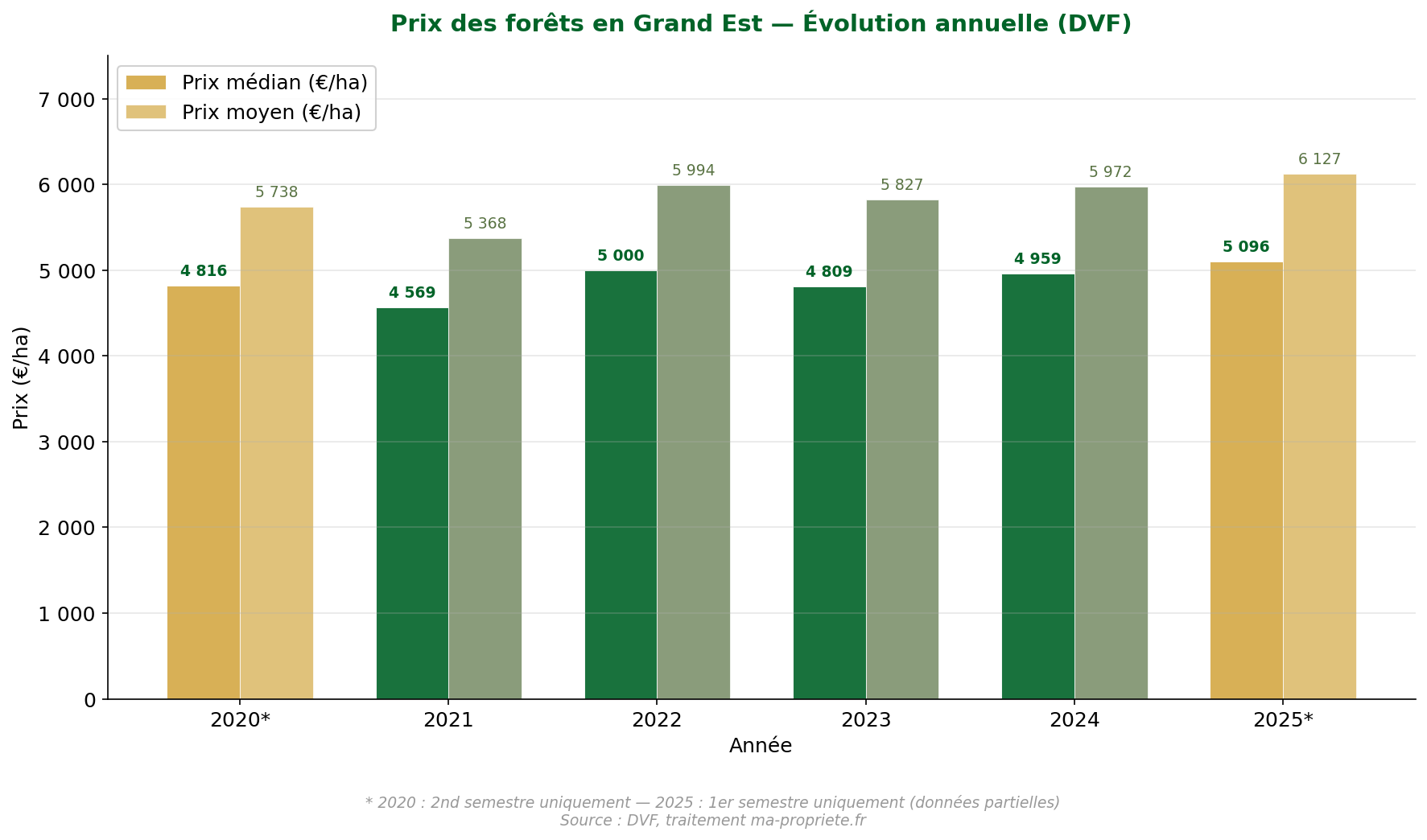

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Grand Est stood at €5,096/ha, for an average price of €6,127/ha, based on 217 transactions. These figures suggest a slight increase compared to the reference year 2024, when the median price reached €4,959/ha for 538 recorded sales.

Over the entire 2020-2025 period, the Grand Est region shows a median price of €4,849/ha and an average price of €5,820/ha. The gap between these two indicators (approximately 20%) is classic in the forest market: the arithmetic mean is mechanically pulled upwards by small plots sold at high unit prices. The median price, which separates transactions into two equal halves, more accurately reflects the current market.

The median surface area of transactions in Grand Est stands at 3.09 hectares, close to the national median (3.3 ha). The total volume exchanged over the period reached 21,610 hectares, for a total of 2,526 sales.

| Indicator | 2025* | 2024 | 2023 | 2022 | 2021 | 2020* |

|---|---|---|---|---|---|---|

| Number of transactions | 217 | 538 | 553 | 498 | 490 | 230 |

| Average price (€/ha) | 6,127 | 5,972 | 5,827 | 5,994 | 5,368 | 5,738 |

| Median price (€/ha) | 5,096 | 4,959 | 4,809 | 5,000 | 4,569 | 4,816 |

| Min price (€/ha) | 1,816 | 1,400 | 1,106 | 1,538 | 1,171 | 1,185 |

| Max price (€/ha) | 25,223 | 21,905 | 18,919 | 22,645 | 26,627 | 24,467 |

| Median area (ha) | 3.21 | 3.06 | 2.98 | 3.07 | 3.46 | 2.59 |

| Exchanged volume (ha) | 1,752 | 5,043 | 3,838 | 4,537 | 4,552 | 1,888 |

* 2025: partial data, 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Annual evolution of forest prices in Grand Est (2020-2025) — Source: DVF, ma-propriete.fr processing

The evolution over the full years (2021 to 2024) shows a generally upward trajectory. The median price rose from €4,569/ha in 2021 to €4,959/ha in 2024, an increase of +8.5% over three years. The year 2022 marked an intermediate peak at €5,000/ha, followed by a slight dip in 2023 (€4,809/ha) before another rebound in 2024. The annual volume of transactions remains stable, at around 500 to 550 sales per year, a sign of a regular market.

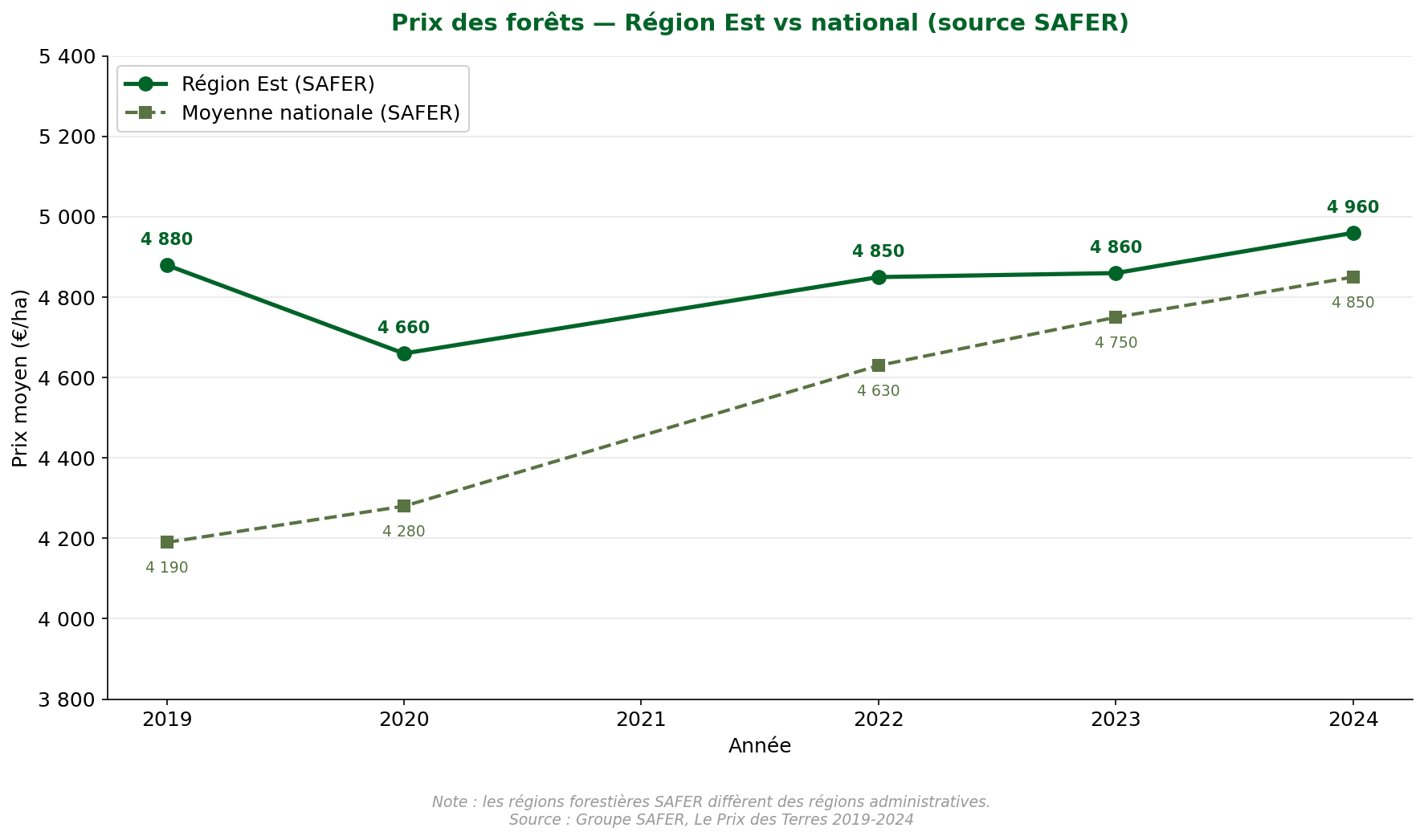

The SAFER Group publishes its own estimates of forest prices each year, established according to a different methodology from that of the DVF database. SAFER forest regions do not correspond to administrative regions: administrative Grand Est is mainly covered by SAFER's "East" forest region. The figures are therefore not directly comparable, but the underlying trend remains similar.

| Year | Average Price East (€/ha) | National Average Price (€/ha) |

|---|---|---|

| 2019 | 4,880 | 4,190 |

| 2020 | 4,660 | 4,280 |

| 2022 | 4,850 | 4,630 |

| 2023 | 4,860 | 4,750 |

| 2024 | 4,960 | 4,850 |

Source: Groupe SAFER, Le Prix des Terres 2019-2024. Empty cells = data not published for the year concerned.

Forest prices — East region vs. national average (source: SAFER, 2019-2024)

According to SAFER, the average price of forests in the East region is progressing moderately: from €4,880/ha in 2019 to €4,960/ha in 2024, an increase of +1.6% over five years. This progression is much more contained than that observed at the national level (+15.7% over the same period). The East region has historically been above the national average, but the gap is gradually narrowing: in 2019, the East region exceeded the average by +16.5%; in 2024, this gap is only +2.3%. This narrowing reflects the catch-up dynamic of other regions, driven in particular by the markets in the West and the North-Paris Basin.

The Grand Est region has ten departments. However, the three departments of Bas-Rhin (67), Haut-Rhin (68) and Moselle (57), subject to the local Alsatian-Mosellan law regime, are not covered by the DVF database. The statistics below therefore relate to the seven departments for which data is available: Ardennes (08), Aube (10), Marne (51), Haute-Marne (52), Meurthe-et-Moselle (54), Meuse (55) and Vosges (88).

The differences between departments are significant: the median price varies from single to double, from €3,616/ha in Haute-Marne to €5,875/ha in the Ardennes. This dispersion reflects very different forestry realities in terms of site quality, dominant species and land pressure.

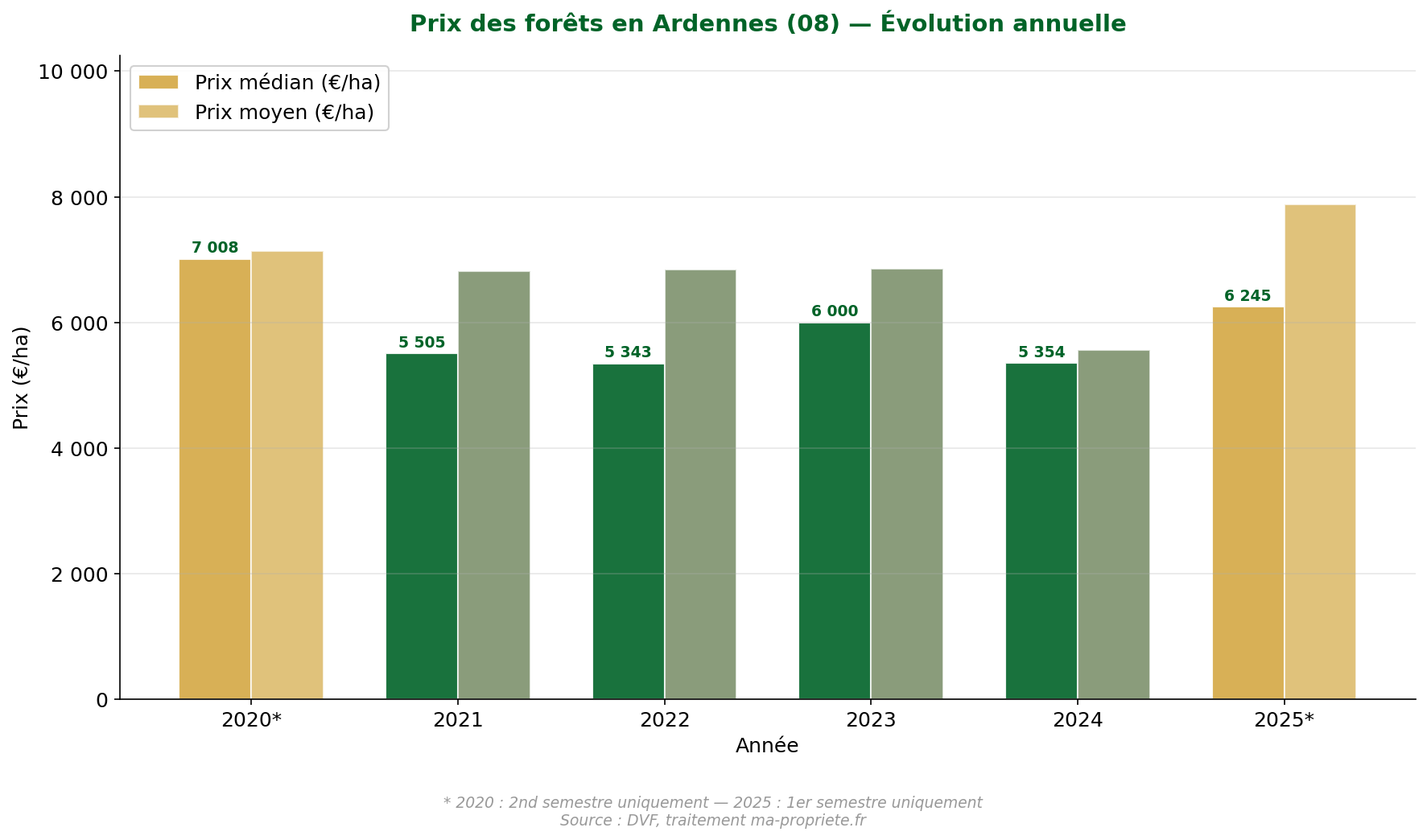

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in the Ardennes reached €6,245/ha, a sharp increase compared to 2024 (€5,354/ha). This rebound remains to be confirmed over the full year, as the low number of transactions (28 in the 1st half) limits statistical robustness.

In the reference year 2024, the department recorded 73 sales, a median price of €5,354/ha and an average price of €5,554/ha. Over the entire 2020-2025 period, the median price was €5,875/ha for 325 transactions, which places the Ardennes among the most expensive departments in the region.

The Ardennes massif, bordering Belgium, is dominated by hardwoods (sessile oak, beech) and benefits from good quality forest sites. Proximity to the Belgian and Luxembourg markets maintains steady demand.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 28 | 7,882 | 6,245 |

| 2024 | 73 | 5,554 | 5,354 |

| 2023 | 59 | 6,857 | 6,000 |

| 2022 | 67 | 6,841 | 5,343 |

| 2021 | 57 | 6,820 | 5,505 |

| 2020* | 41 | 7,129 | 7,008 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in the Ardennes (08) — Source: DVF, ma-propriete.fr processing

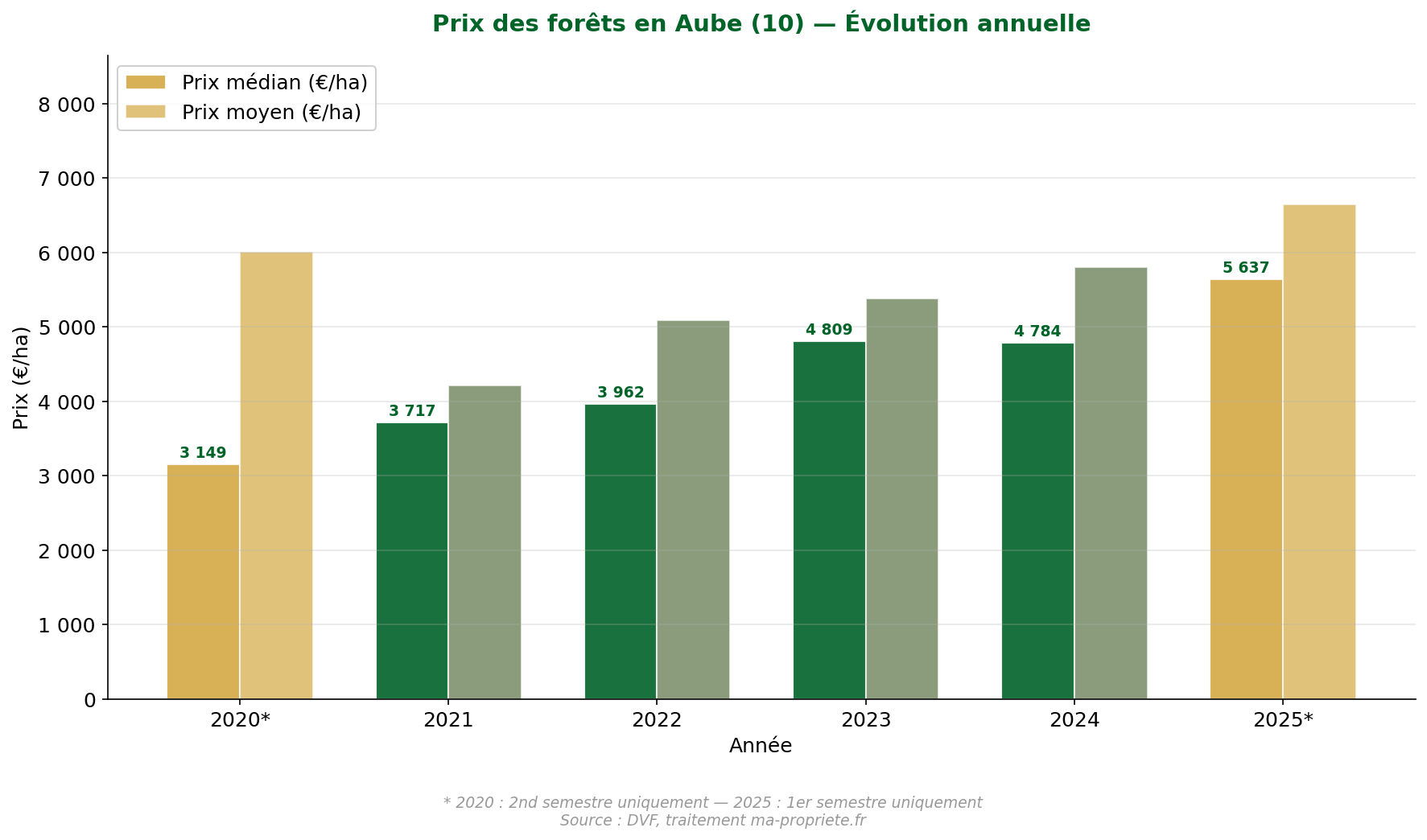

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price in Aube rose to €5,637/ha for 18 transactions, an increase compared to 2024 (€4,784/ha for 62 sales).

Over the entire 2020-2025 period, the median price stood at €4,200/ha for 297 sales. Aube is in the intermediate range for the region, with a marked upward trend since 2021: the median price rose from €3,717/ha in 2021 to €4,784/ha in 2024, or +28.7% in three years.

The department is characterized by significant forest cover in the eastern part (Orient Forest, wet Champagne), dominated by pedunculate oak, ash and hornbeam in the plains, and by beech on the plateaus. The appeal of Aube's forests is reinforced by the presence of the Orient Forest Regional Natural Park, which offers a sought-after landscape setting.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 18 | 6,648 | 5,637 |

| 2024 | 62 | 5,799 | 4,784 |

| 2023 | 74 | 5,381 | 4,809 |

| 2022 | 61 | 5,089 | 3,962 |

| 2021 | 57 | 4,216 | 3,717 |

| 2020* | 25 | 6,003 | 3,149 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in the Aube (10) — Source: DVF, ma-propriete.fr processing

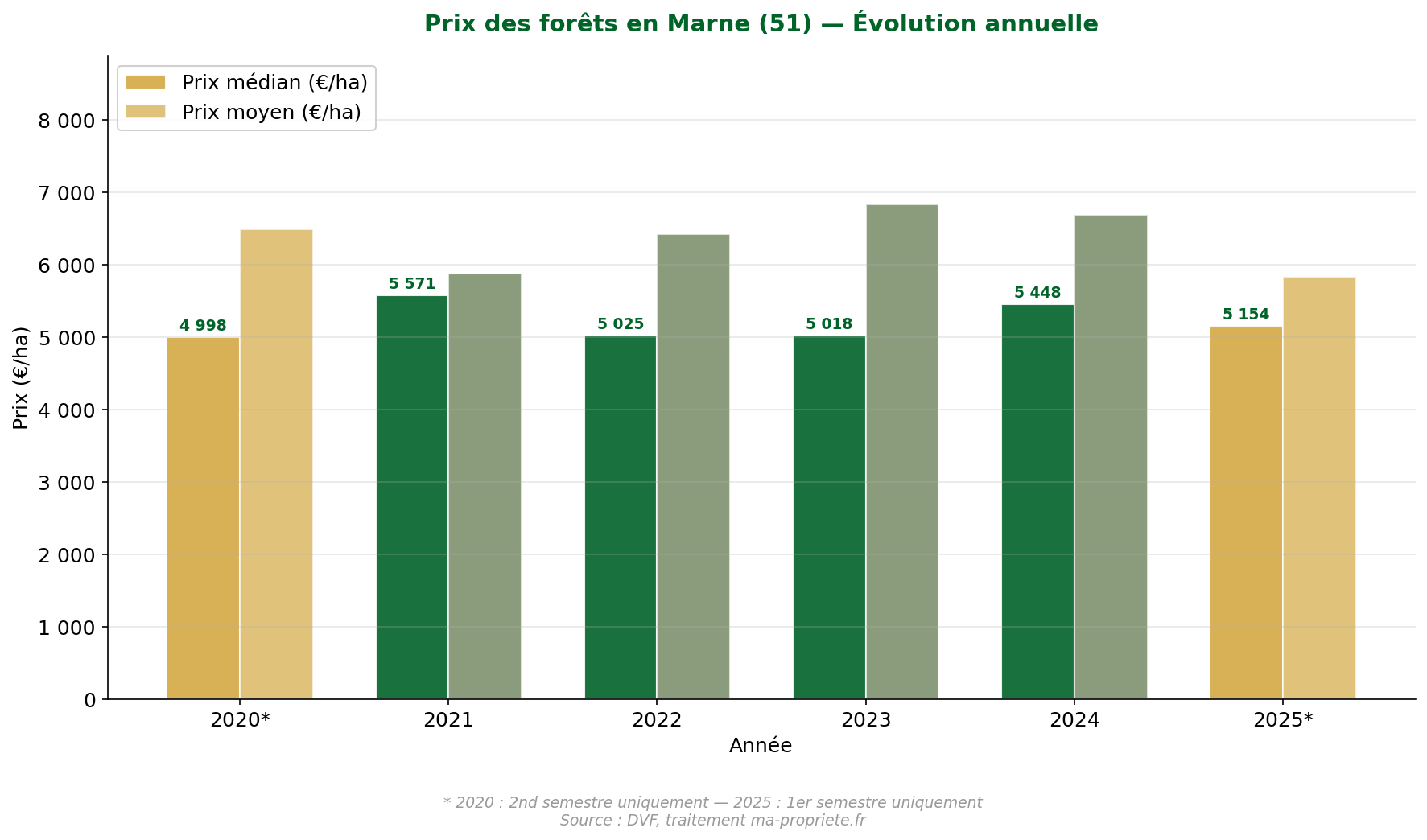

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price in the Marne stood at €5,154/ha for 47 transactions. This level is close to that observed in 2024 (€5,448/ha for 102 sales), suggesting relative market stability.

The Marne is the most active department in Grand Est in terms of forest transaction volume: 502 sales over the 2020-2025 period, nearly one-fifth of the regional total. The overall median price stood at €5,227/ha, for an average price of €6,428/ha.

The department benefits from quality forest massifs in the Montagne de Reims and in chalky Champagne, with a dominance of hardwoods (beech, oak). Proximity to Reims and Paris helps maintain steady demand, including from buyers with heritage goals.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 47 | 5,834 | 5,154 |

| 2024 | 102 | 6,684 | 5,448 |

| 2023 | 129 | 6,835 | 5,018 |

| 2022 | 89 | 6,425 | 5,025 |

| 2021 | 95 | 5,874 | 5,571 |

| 2020* | 40 | 6,484 | 4,998 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in the Marne (51) — Source: DVF, ma-propriete.fr processing

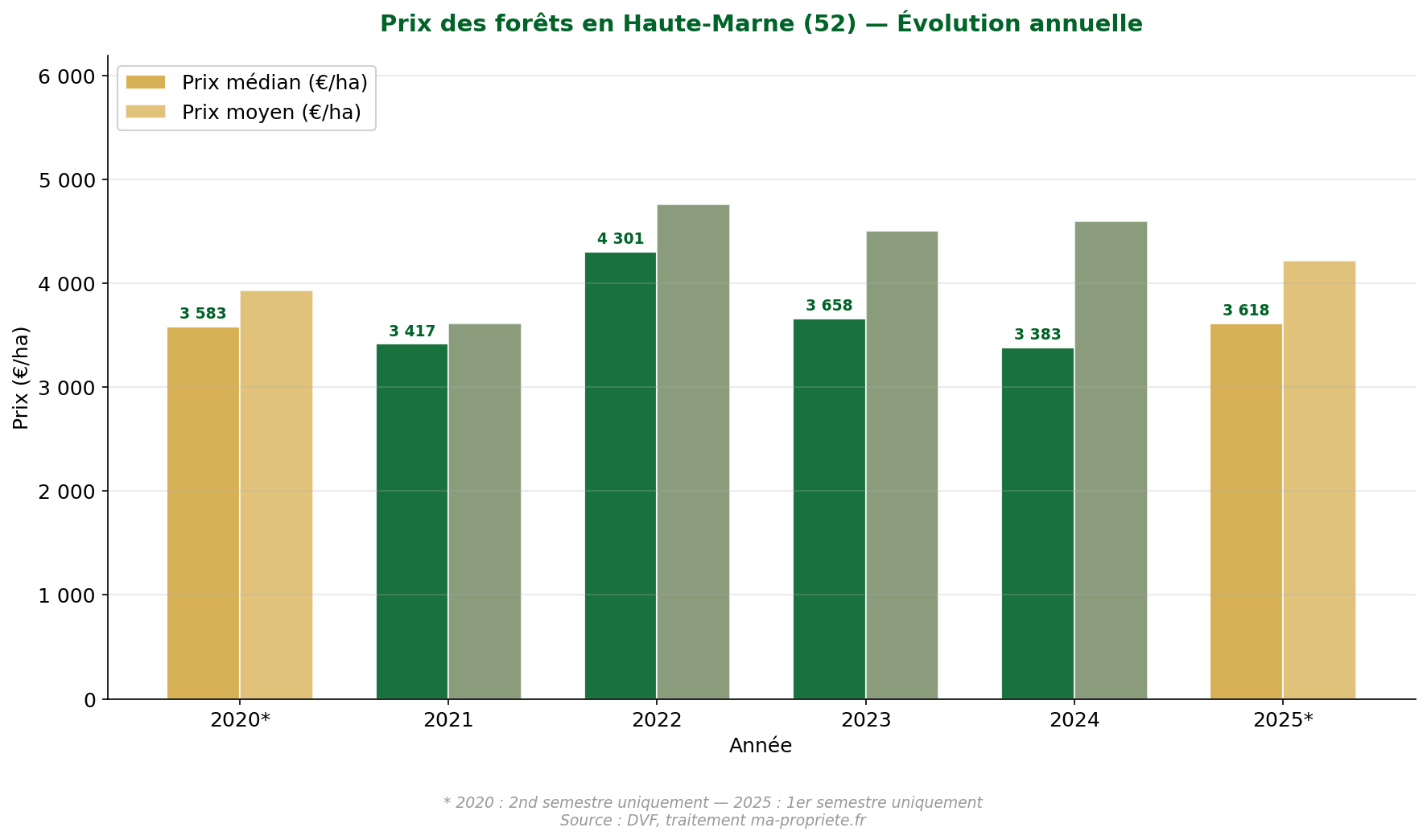

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price in Haute-Marne rose to €3,618/ha for 36 transactions. This level is comparable to that of 2024 (€3,383/ha for 79 sales), confirming the department's position among the most accessible in the region.

Over the entire 2020-2025 period, the median price stood at €3,616/ha for 317 sales, for an average price of €4,323/ha. Haute-Marne is the least expensive department in Grand Est for forest acquisition. The median surface area of transactions (4.27 ha) is the highest in the region, a sign of a market oriented towards larger-than-average plots.

The department is covered by vast forest massifs (the reforestation rate exceeds 40%), dominated by oak and beech on limestone soils. The Châtillon-sur-Seine forest, straddling Haute-Marne and Côte-d'Or, is one of the most extensive hardwood massifs in northeastern France. Distance from major urban centers explains the contained prices, despite recognized forest quality.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 36 | 4,216 | 3,618 |

| 2024 | 79 | 4,598 | 3,383 |

| 2023 | 55 | 4,504 | 3,658 |

| 2022 | 59 | 4,763 | 4,301 |

| 2021 | 61 | 3,612 | 3,417 |

| 2020* | 27 | 3,931 | 3,583 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in Haute-Marne (52) — Source: DVF, ma-propriete.fr processing

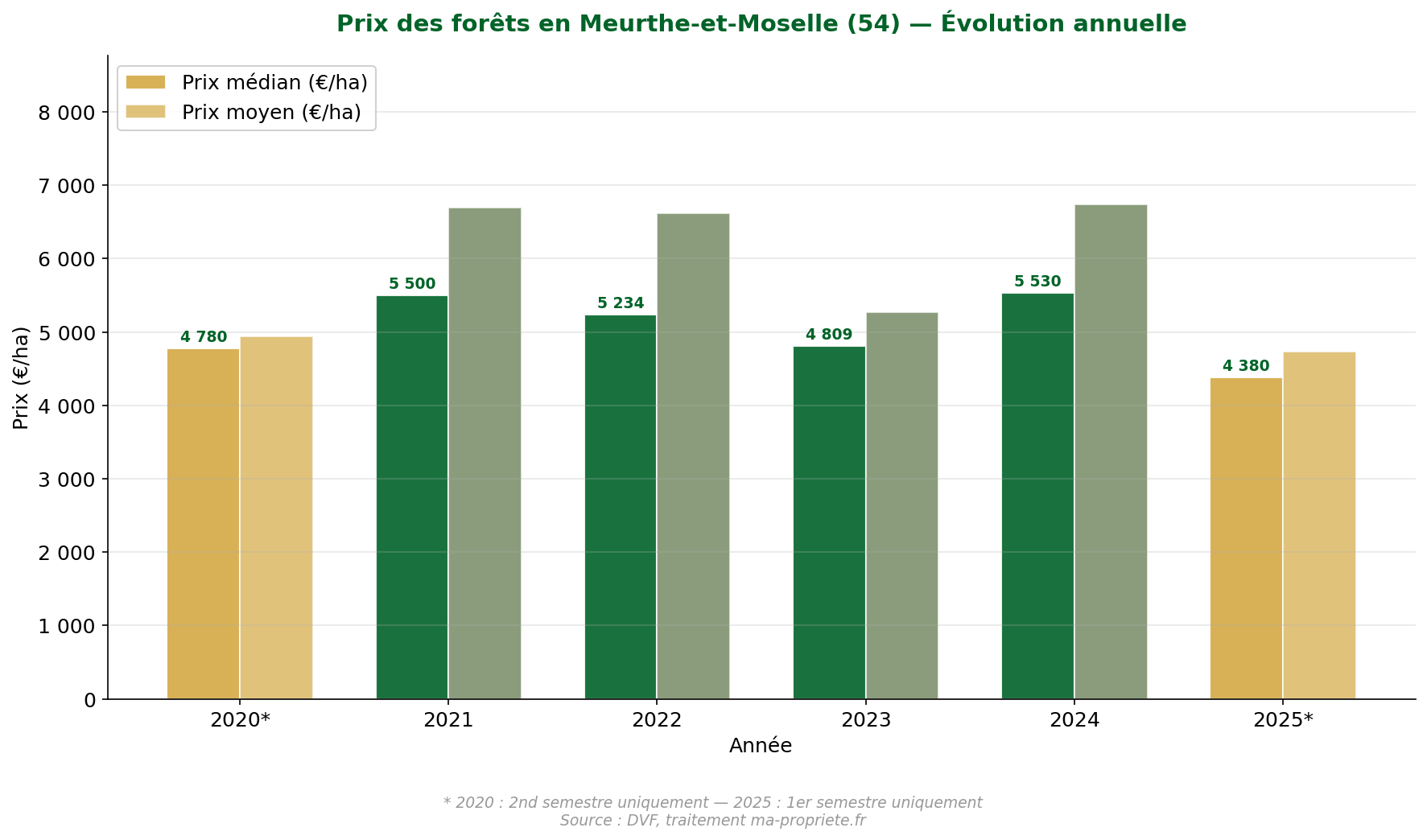

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price in Meurthe-et-Moselle stood at €4,380/ha for 22 transactions, down compared to 2024 (€5,530/ha for 63 sales). However, the low volume of transactions in the 1st half suggests not drawing hasty conclusions.

Over the entire 2020-2025 period, the median price reached €5,015/ha for 254 sales, with an average price of €6,041/ha. The department experiences marked annual fluctuations, with the median price oscillating between €4,380/ha (2025, partial) and €5,530/ha (2024). The presence of the Nancy urban area supports demand for peri-urban forests.

Meurthe-et-Moselle forests mix hardwoods (beech, oak) and conifers (spruce) according to altitude and exposure. The department has been significantly affected by health crises related to bark beetles on spruce stands in recent years, which may have locally affected the prices of coniferous plots.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 22 | 4,737 | 4,380 |

| 2024 | 63 | 6,743 | 5,530 |

| 2023 | 55 | 5,265 | 4,809 |

| 2022 | 46 | 6,614 | 5,234 |

| 2021 | 43 | 6,701 | 5,500 |

| 2020* | 25 | 4,942 | 4,780 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in Meurthe-et-Moselle (54) — Source: DVF, ma-propriete.fr processing

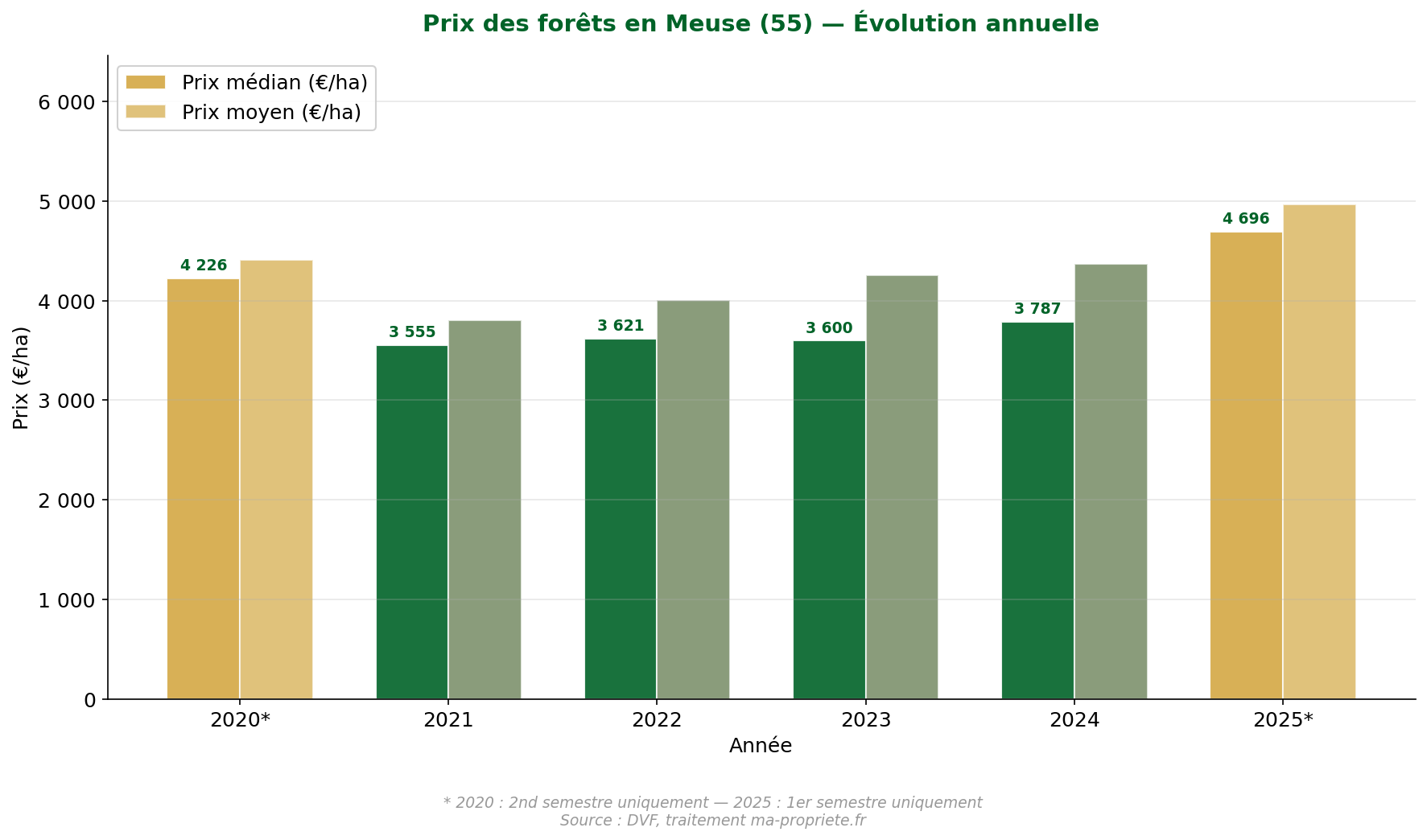

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price in the Meuse reached €4,696/ha for 23 transactions, a sharp increase compared to 2024 (€3,787/ha for 71 sales). This progression remains to be confirmed over the full year.

Over the entire 2020-2025 period, the median price stood at €3,744/ha for 312 sales, with an average price of €4,199/ha. Meuse is one of the least expensive departments in the region, just above Haute-Marne. The evolution over full years shows steady progression: from €3,555/ha in 2021 to €3,787/ha in 2024, or +6.5% in three years.

The Meuse is a very forested department (reforestation rate of around 37%), with hardwood massifs (oak, beech) on the limestone plateaus of Barrois and Argonne. Forests there retain a marked productive character, with traditional regular high forest silviculture. The median surface area of transactions (3.99 ha) is among the highest in the region.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 23 | 4,970 | 4,696 |

| 2024 | 71 | 4,368 | 3,787 |

| 2023 | 68 | 4,253 | 3,600 |

| 2022 | 58 | 4,002 | 3,621 |

| 2021 | 68 | 3,803 | 3,555 |

| 2020* | 24 | 4,412 | 4,226 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in the Meuse (55) — Source: DVF, ma-propriete.fr processing

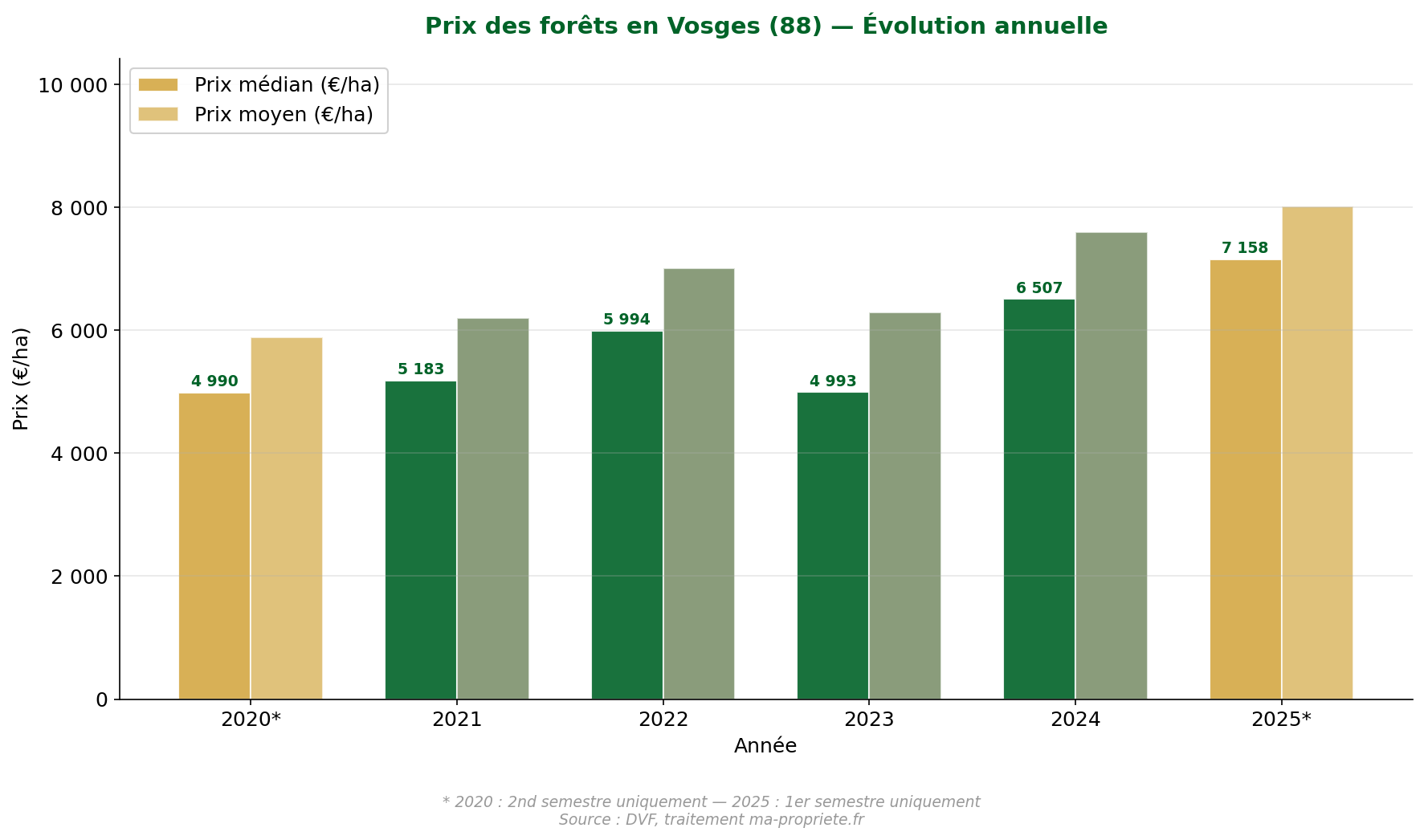

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price in the Vosges reached €7,158/ha for 43 transactions, a sharp increase compared to 2024 (€6,507/ha for 88 sales). The Vosges thus confirms its position as the most expensive department in Grand Est for purchasing a forest, well above the regional average.

Over the entire 2020-2025 period, the median price stood at €5,749/ha for 519 sales — the most active department in the region. The average price reached €6,763/ha. The upward dynamic is the most marked in Grand Est: the median price rose from €5,183/ha in 2021 to €6,507/ha in 2024, or +25.6% in three years.

The Vosges massif combines hardwoods on the western slope (beech, oak) and conifers at altitude (silver fir, spruce). Despite damage caused by bark beetles on spruce stands, demand remains steady. The Vosges benefits from a very structured timber industry (sawmills, timber, wood energy) and a strong landscape appeal that feeds demand from investors and buyers seeking forest heritage.

| Year | No. sales | Average price (€/ha) | Median price (€/ha) |

|---|---|---|---|

| 2025* | 43 | 8,017 | 7,158 |

| 2024 | 88 | 7,593 | 6,507 |

| 2023 | 113 | 6,296 | 4,993 |

| 2022 | 118 | 7,011 | 5,994 |

| 2021 | 109 | 6,203 | 5,183 |

| 2020* | 48 | 5,883 | 4,990 |

* 2025: 1st half only. 2020: 2nd half only. Source: DVF, ma-propriete.fr processing.

Forest prices in the Vosges (88) — Source: DVF, ma-propriete.fr processing

The statistics presented in this article are derived from the analysis of the DVF (Demandes de Valeurs Foncières) database, published in open data by the Ministry of Economy. This database lists all real estate and land transactions declared to the tax administration.

To isolate relevant forest transactions, the following filtering method was applied: selection of properties whose land use corresponds to woods, high forests, coppice, poplar groves and other forest stands; removal of transactions involving a surface area of less than 1 hectare; exclusion of transactions where the price per hectare is less than €500/ha or greater than €100,000/ha; finally, removal in each department of the 50% of transactions with extreme prices (the 25% lowest and 25% highest), in order to smooth atypical values and obtain indicators more representative of the current market.

The period covered runs from July 1, 2020, to June 30, 2025, for a total of 31,383 transactions retained at the national level.

Several limitations must be kept in mind when reading these statistics.

The first concerns the geographic scope. The departments of Bas-Rhin (67), Haut-Rhin (68) and Moselle (57) are subject to the land registry system (local Alsatian-Mosellan law) and are not covered by the DVF database. For the Grand Est region, this means that three out of ten departments are absent from the analysis — a significant gap that notably excludes the Vosges forests on the Alsatian side and the massifs of Moselle.

The second limitation relates to partial years. The 2020 data only cover the second half of the year (July-December), and the 2025 data only cover the first half (January-June). These two half-years cannot be directly compared to full years (2021 to 2024), nor to each other.

Thirdly, DVF data record transactions of properties in full ownership. They do not include sales of company shares, specifically shares in Forest Groups (GF or GFI). However, these companies hold a significant portion of large French forests, particularly those with a Simple Management Plan. The market for forest group shares, which mainly concerns large estates, therefore escapes this analysis. This can lead to an under-representation of the large-scale forest segment in DVF statistics.

Fourthly, mixed properties (forest + agricultural land, forest + buildings) are difficult to isolate in the DVF database. The chosen filtering method strives to keep only transactions involving predominantly forest land, but some borderline cases may remain.

Finally, the transaction volume per department can vary greatly: a department totaling fewer than 30 transactions over the study period produces statistically fragile indicators, to be interpreted with caution.

SAFER statistics (published annually in the "Le Prix des Terres" report) and the DVF statistics presented here are based on different methodologies and scopes, which it is important to distinguish.

From a geographic positioning perspective, SAFER uses a breakdown into forest regions (based on the IGN's Major Ecological Regions: West, North-Paris Basin, East, Massif Central, Southwest, Alps-Mediterranean-Pyrenees) which does not correspond to administrative regions. SAFER's "East" forest region does not exactly overlap with administrative Grand Est.

From a calculation method perspective, SAFER applies a hedonic model for equivalent quality, which aims to neutralize composition effects (size, species, location), whereas the DVF statistics presented here are based on averages and medians calculated after filtering out extreme prices. The SAFER national average price is a weighted average by regional forest areas.

From a scope perspective, SAFER only retains non-built forest properties of at least 1 hectare, provided that 80% of the surface area is classified as woods, coppice, high forest, or conifers in the land registry. The ma-propriete.fr DVF method applies a similar area threshold (1 ha) but retains properties based on the nature of the cadastral cultivation.

Despite these differences, the two sources converge on orders of magnitude and major trends: the ma-propriete.fr DVF median price is very close to the SAFER average price, with a gap generally between -3% and +3%. Multi-year trends are also consistent.

The forest market in Grand Est is characterized by a moderate but steady increase in prices over the 2021-2024 period, with a regional median price standing at around €4,850/ha — a level close to the national median. Departmental dispersion is notable: from the Vosges (€5,749/ha) and the Ardennes (€5,875/ha) with the highest prices, to Haute-Marne (€3,616/ha) and Meuse (€3,744/ha) which offer the most accessible entry points. The absence of DVF data for Bas-Rhin, Haut-Rhin, and Moselle remains a significant gap to keep in mind.

To explore prices in other French regions, consult listings for forests for sale in Grand Est, or download our complete guide to forest investment by visiting our forest price observatory.

| Region | Median Price (€/ha) | No. Sales | Link to article |

|---|---|---|---|

| Auvergne-Rhône-Alpes | 4,000 | 4,706 | Read article |

| Bourgogne-Franche-Comté | 4,784 | 3,005 | Read article |

| Brittany | 4,827 | 1,180 | Read article |

| Centre-Val de Loire | 5,579 | 1,669 | Read article |

| Grand Est | 4,849 | 2,526 | This article |

| Hauts-de-France | 8,772 | 1,777 | Read article |

| Île-de-France | 6,635 | 577 | Read article |

| Normandy | 9,075 | 1,442 | Read article |

| Nouvelle-Aquitaine | 3,667 | 7,102 | Read article |

| Occitanie | 3,612 | 3,347 | Read article |

| Pays de la Loire | 4,865 | 1,289 | Read article |

| Provence-Alpes-Côte d'Azur | 5,488 | 1,905 | Read article |

Source: DVF 2020-2025, ma-propriete.fr processing. Data for Corsica and Overseas Territories not included in this table.