Normandy has approximately 520,000 hectares of forest, representing 19% of its territory, spread across various massifs ranging from the beech forests of the Pays de Bray to the oak forests of the Norman Perche, as well as the national forests of Brotonne, Roumare, and Eawy. The region is characterized by high-quality woodland: Norman beech and oak are among the most sought-after by timber buyers, and the forest massifs benefit from a rainfall pattern favorable to sustained growth. This silvicultural quality is directly reflected in prices: with a median of €9,075/ha over the 2020–2025 period, Normandy is one of the most expensive regions in France for forest acquisition. Between July 2020 and June 2025, the region accounted for 4.6% of national forest transactions, with 1,442 sales recorded. The 2025 data only covers the 1st half of the year and is presented for information purposes only.

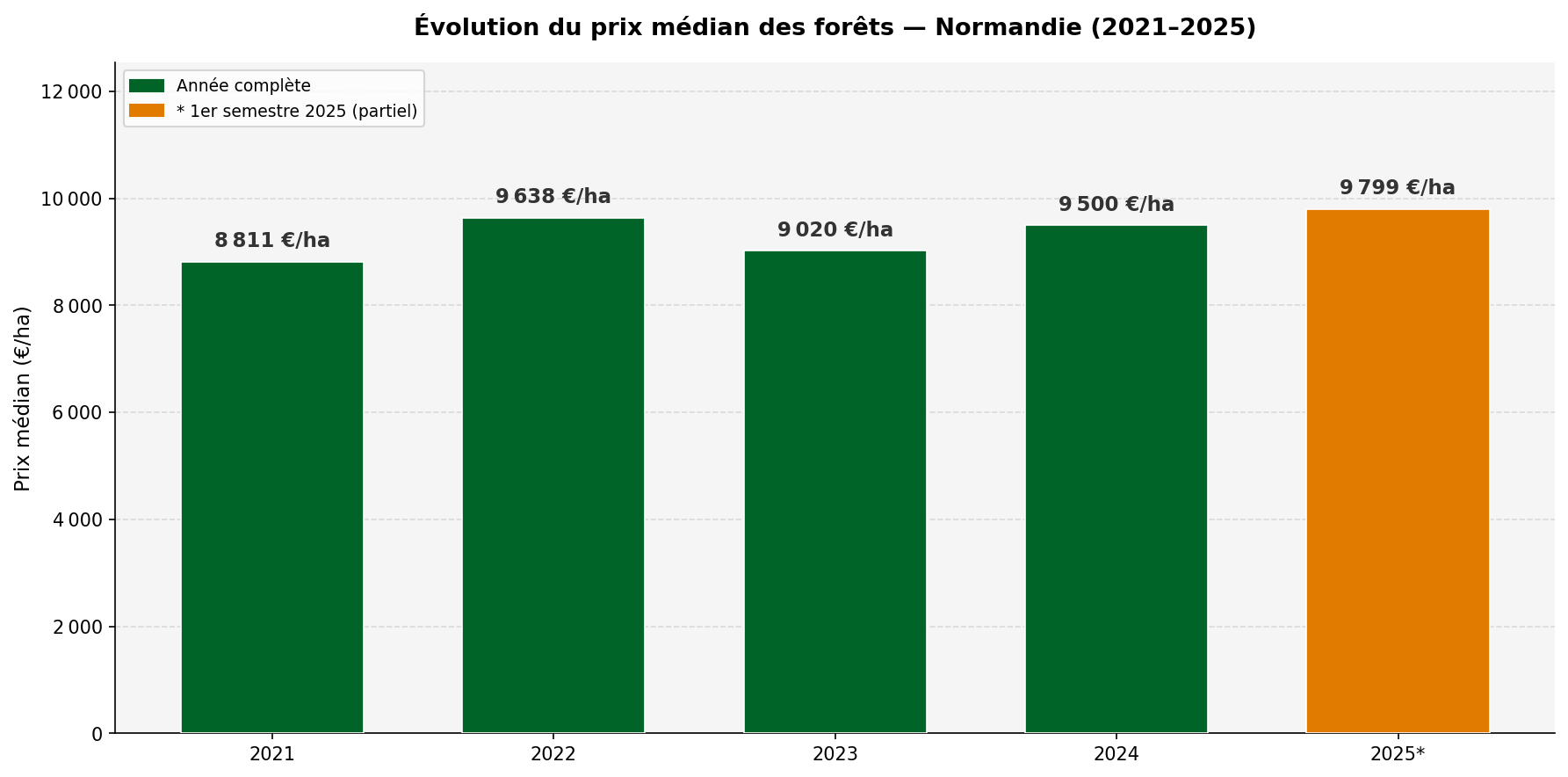

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Normandy stood at €9,799/ha, a slight increase compared to the reference year 2024. Over the whole of 2024, the median price was €9,500/ha for 260 filtered transactions. Normandy has thus maintained a price level consistently above €9,000/ha since 2021, more than double the national median. This premium positioning is explained by the quality of the species, the productivity of the massifs, and sustained demand from wood processing industries and heritage investors.

| Indicator | 2025* (H1) | 2024 (ref.) | 2020-2025 Period |

|---|---|---|---|

| Number of transactions | 142 | 260 | 1,442 |

| Median price (€/ha) | €9,799/ha | €9,500/ha | €9,075/ha |

| Average price (€/ha) | €10,443/ha | €10,200/ha | €9,962/ha |

| Median surface area (ha) | — | — | 2.7 ha |

| Volume traded (ha) | — | — | 10,895 ha |

* Partial data for the 1st half of 2025, to be interpreted with caution. Source: DVF, processed by ma-propriete.fr

Evolution of the median price of forests in Normandy (2021–2025) — Source: DVF, processed by ma-propriete.fr

The Norman trajectory differs from the national trend: after a peak of €9,638/ha in 2022, the median price returned to €9,020/ha in 2023, before recovering to €9,500/ha in 2024. This relative volatility is characteristic of a deep market where a few large transactions can influence the median. The underlying trend nevertheless remains bullish over the period as a whole, with an increase of +8% between 2021 and 2025 (H1).

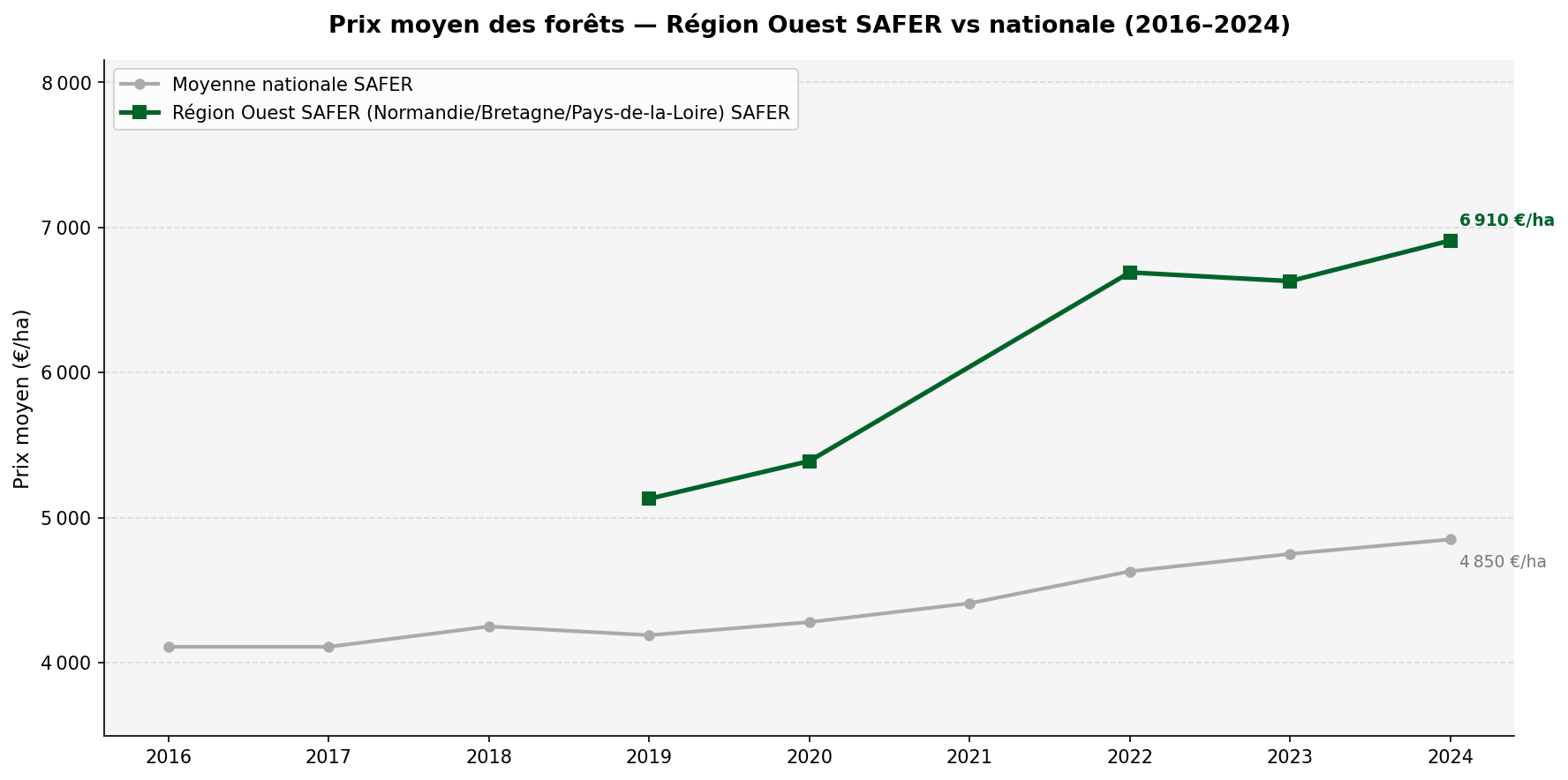

SAFER links Normandy to the "West" forest region, which also covers Brittany and the Pays de la Loire. This forest region is among the most highly valued in France according to SAFER data, with an average price of €6,910/ha in 2024 — significantly higher than the national average (€4,850/ha). Normandy is the driving force behind this valuation within the SAFER West region.

| Year | SAFER West Region average price (€/ha) |

SAFER National average price (€/ha) |

|---|---|---|

| 2019 | 5,130 | 4,190 |

| 2020 | 5,390 | 4,280 |

| 2022 | 6,690 | 4,630 |

| 2023 | 6,630 | 4,750 |

| 2024 | 6,910 | 4,850 |

Source: Groupe Safer, Le Prix des Terres (2019–2024). "West" forest region.

Average forest prices — SAFER West Region vs national average (2016–2024) — Source: Groupe Safer, Le Prix des Terres

The gap between the regional SAFER average price (€6,910/ha) and the Norman DVF median price (€9,500/ha in 2024) is significant. This is explained on the one hand by the method (average vs median), and on the other by the composition of the SAFER West region, which includes less valued territories such as certain areas of the Pays de la Loire or Brittany. Normandy truly pulls up the average for this forest region.

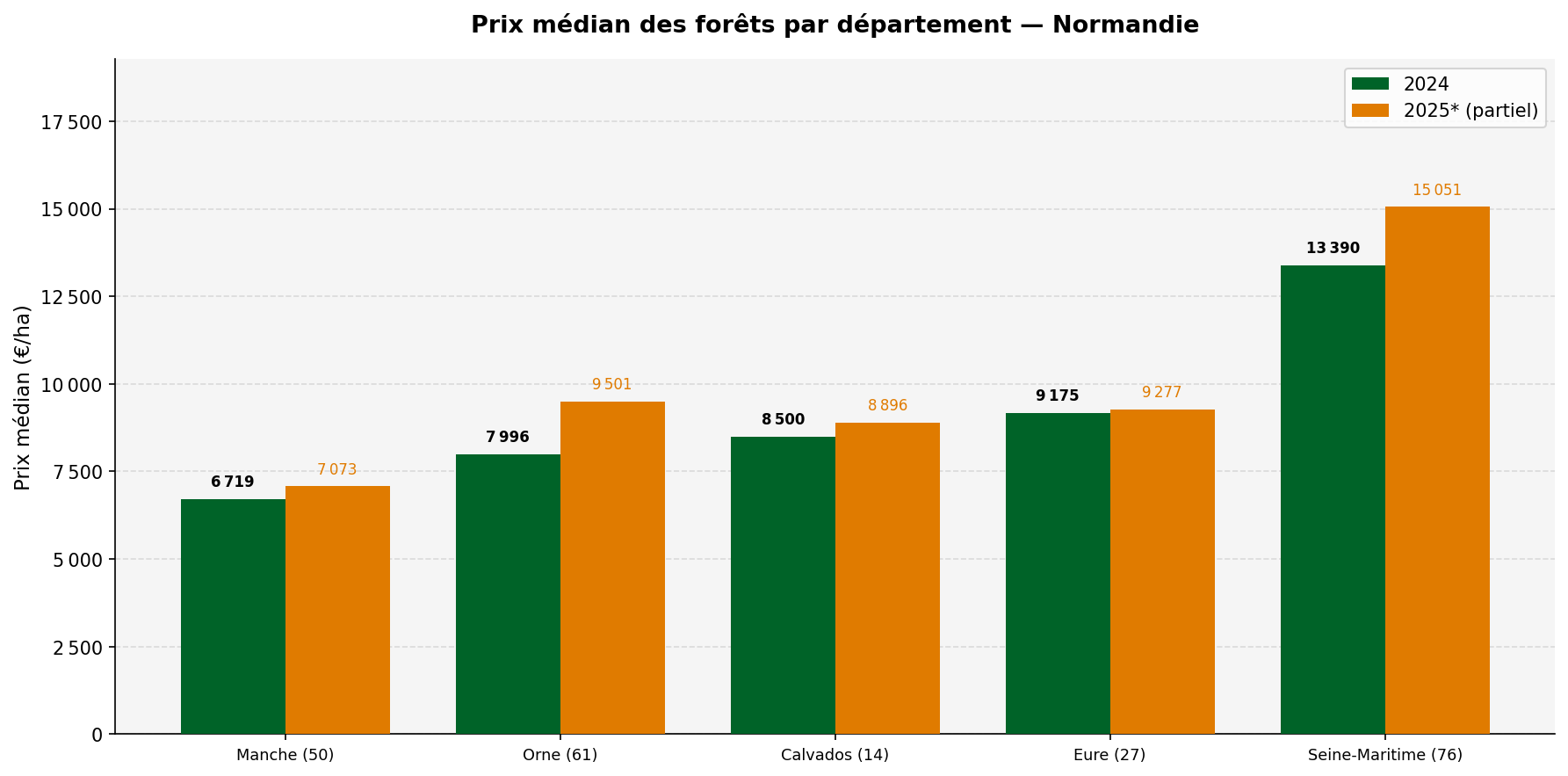

Median forest prices by department — Normandy, 2024 and 2025* — Source: DVF, processed by ma-propriete.fr

Calvados shows a median price of €8,500/ha in 2024, stable in the 1st half of 2025 (€8,896/ha, partial data to be interpreted with caution). The bocage forests and the beech massifs of the Pays d'Auge and the Bessin are appreciated there for their wood quality and landscape interest. The median surface area of 2.77 ha reflects a market of family properties and medium-sized holdings. With 212 transactions over the period, the market is well supplied.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 18 | 43 | 212 |

| Median price (€/ha) | €8,896 | €8,500 | €8,505 |

| Average price (€/ha) | €9,294 | €9,099 | €9,137 |

| Median surface area | — | — | 2.77 ha |

* Partial data for the 1st half of 2025.

Eure is one of the most active markets in Normandy with 466 transactions over the period. The median price in 2024 reached €9,175/ha, rising slightly in the 1st half of 2025 (€9,277/ha, partial data to be interpreted with caution). The Brotonne forest, the beech forests of Roumois, and the massifs of the Pays de Caux make Eure a leading forest department. Its proximity to Île-de-France and the major ports of the Seine generates sustained industrial and heritage demand. The median surface area of 2.3 ha reflects a network of active small forest owners.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 58 | 74 | 466 |

| Median price (€/ha) | €9,277 | €9,175 | €8,645 |

| Average price (€/ha) | €9,925 | €9,531 | €9,116 |

| Median surface area | — | — | 2.30 ha |

* Partial data for the 1st half of 2025.

Manche offers the most accessible forest prices in Normandy with a median price of €6,719/ha in 2024, rising in the 1st half of 2025 (€7,073/ha, partial data to be interpreted with caution). The Manche bocage, dominated by meadows, leaves less room for forests than elsewhere. The woodlands there are often poplar or resinous plantations on damp ground, valued less than the beech and oak forests of other Norman departments. Despite this, the market remains active (143 transactions) and prices remain well above the national median.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 17 | 28 | 143 |

| Median price (€/ha) | €7,073 | €6,719 | €6,268 |

| Average price (€/ha) | €7,854 | €6,672 | €7,107 |

| Median surface area | — | — | 2.08 ha |

* Partial data for the 1st half of 2025.

Orne, the heart of the Norman Perche, is home to renowned beech and oak forests. In 2024, the median price reached €7,996/ha, rising in the 1st half of 2025 (€9,501/ha, partial data to be interpreted with caution). The Bellême forest, the Perche Natural Park, and the bocage massifs of Orne are recognized for their biodiversity and wood quality. The progression in the first half of 2025 suggests a renewed interest in this department, which remains slightly behind the prices of Eure and Seine-Maritime.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 22 | 40 | 254 |

| Median price (€/ha) | €9,501 | €7,996 | €7,813 |

| Average price (€/ha) | €9,480 | €8,488 | €8,413 |

| Median surface area | — | — | 2.39 ha |

* Partial data for the 1st half of 2025.

Seine-Maritime is the most expensive department in Normandy, and one of the most highly valued in France, with a median price of €13,390/ha in 2024 and €15,051/ha in the 1st half of 2025 (partial data to be interpreted with caution). The beech forests of the Pays de Caux — Roumare, Eawy, and Jumièges forests — are among the most sought-after in France. The industrial density of the region (chemical, automotive, paper industries) generates a demand for timber and biomass that supports prices. The market there is concentrated (367 transactions) but homogeneous: the gap between average and median price is limited, a sign of low dispersion.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 29 | 73 | 367 |

| Median price (€/ha) | €15,051 | €13,390 | €13,596 |

| Average price (€/ha) | €15,452 | €13,786 | €13,698 |

| Median surface area | — | — | 3.75 ha |

* Partial data for the 1st half of 2025.

The data presented comes from DVF transactions relating exclusively to sales of forests and woods in Normandy between July 2020 and June 2025. An IQR filter is applied to neutralize extreme values. The median price is the central indicator.

DVF data excludes transfers of shares in Forestry Groups (Groupements Forestiers), which are present in the region for large properties. Partial years (2020 H2 and 2025 H1) are identified in all graphs. The small sample sizes by department (notably Manche) require careful interpretation of annual statistics.

The SAFER West region groups together Normandy, Brittany, and the Pays de la Loire. Normandy, with median prices twice as high as the national median, pulls the regional SAFER average up significantly. The gaps between the two sources (SAFER average price vs. DVF median price) nevertheless remain within the expected margin for different methodologies.

Normandy stands out as one of the most highly valued forest regions in France, with a median price exceeding €9,000/ha in 2024 and forests in Seine-Maritime regularly crossing €13,000/ha. This premium reflects the intrinsic quality of the species, the productivity of the massifs, and robust industrial and heritage demand. For buyers, the region offers contrasting opportunities: Manche remains the most accessible entry point, while Seine-Maritime and Eure represent the top end of the Norman market.

Check our forest price observatory in France and our forest listings in Normandy.

| Region | Article |

|---|---|

| Auvergne-Rhône-Alpes | See article |

| Bourgogne-Franche-Comté | See article |

| Brittany | See article |

| Centre-Val de Loire | See article |

| Grand Est | See article |

| Hauts-de-France | See article |

| Île-de-France | See article |

| Normandy | This article |

| Nouvelle-Aquitaine | See article |

| Occitanie | See article |

| Pays de la Loire | See article |

| Provence-Alpes-Côte d'Azur | See article |