The Île-de-France region has approximately 290,000 hectares of forests — accounting for 24% of its territory — a significant proportion of which is public land (state-owned forests of Fontainebleau, Rambouillet, Sénart, Isle-Adam, and Saint-Germain-en-Laye). This public heritage mechanically limits the supply of private forests available for sale. The region represented only 1.8% of French forest transactions between July 2020 and June 2025 (577 sales), a low volume considering the regional economic importance. This niche market, with high heritage potential, targets wealthy buyers seeking properties accessible from Paris. The presence of internationally renowned forest massifs like Fontainebleau (climbing, hiking, biodiversity) contributes to a specific valuation. As the 2025 data only covers the 1st half of the year, it is presented for indicative purposes.

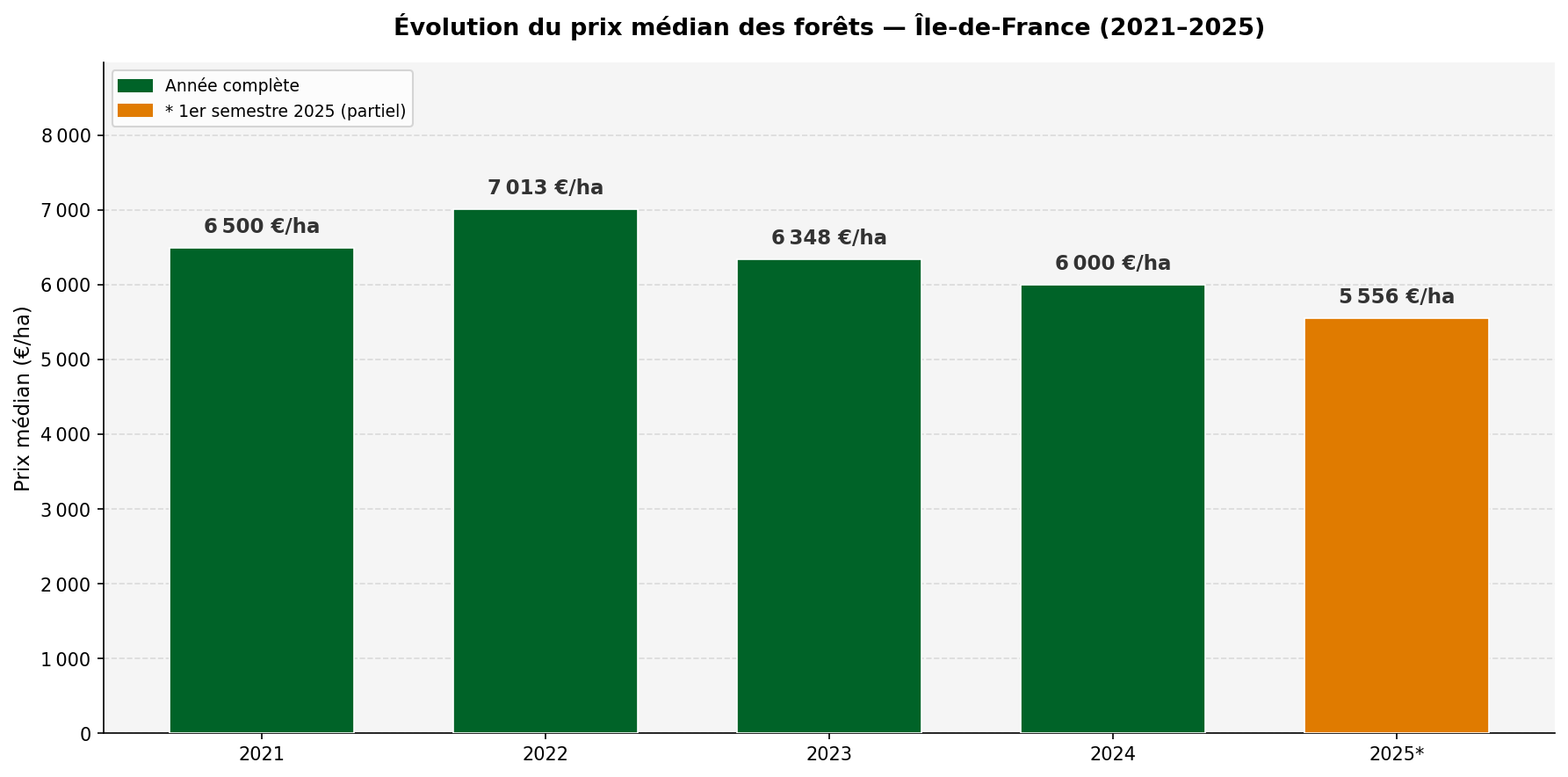

In the 1st half of 2025 (partial data, to be interpreted with caution), the median price of forests in Île-de-France stood at €5,556/ha, a slight decrease compared to the reference year 2024. For the full year 2024, the median price was €6,000/ha for 111 filtered transactions. This level, lower than what might be expected from France's leading economic region, is explained by the market composition: available private forests are often small (median area of 2.82 ha), peri-urban, and their price is driven up more by their heritage potential than by their intrinsic forestry value.

| Indicator | 2025* (H1) | 2024 (ref.) | Period 2020-2025 |

|---|---|---|---|

| Number of transactions | 41 | 111 | 577 |

| Median price (€/ha) | €5,556/ha | €6,000/ha | €6,635/ha |

| Average price (€/ha) | €6,970/ha | €6,738/ha | €8,197/ha |

| Median area (ha) | — | — | 2.82 ha |

| Exchanged volume (ha) | — | — | 5,013 ha |

* Partial data for the 1st half of 2025, to be interpreted with caution. Source: DVF, processed by ma-propriete.fr

Evolution of the median price of forests in Île-de-France (2021–2025) — Source: DVF, processed by ma-propriete.fr

The trajectory in the Paris region shows a slight erosion since the peak in 2022 (€7,013/ha), with a gradual return toward €6,000/ha in 2024. This moderate decline contrasts with the increase observed in comparable regions and can be explained by competition from the real estate market and low liquidity — the number of transactions remains limited and sensitive to the entry or exit of a few major sellers. It should be noted that the gap between the average price (€8,197/ha over the period) and the median price (€6,635/ha) reveals a few very high transactions related to exceptional forests near Paris, particularly in Essonne or Yvelines.

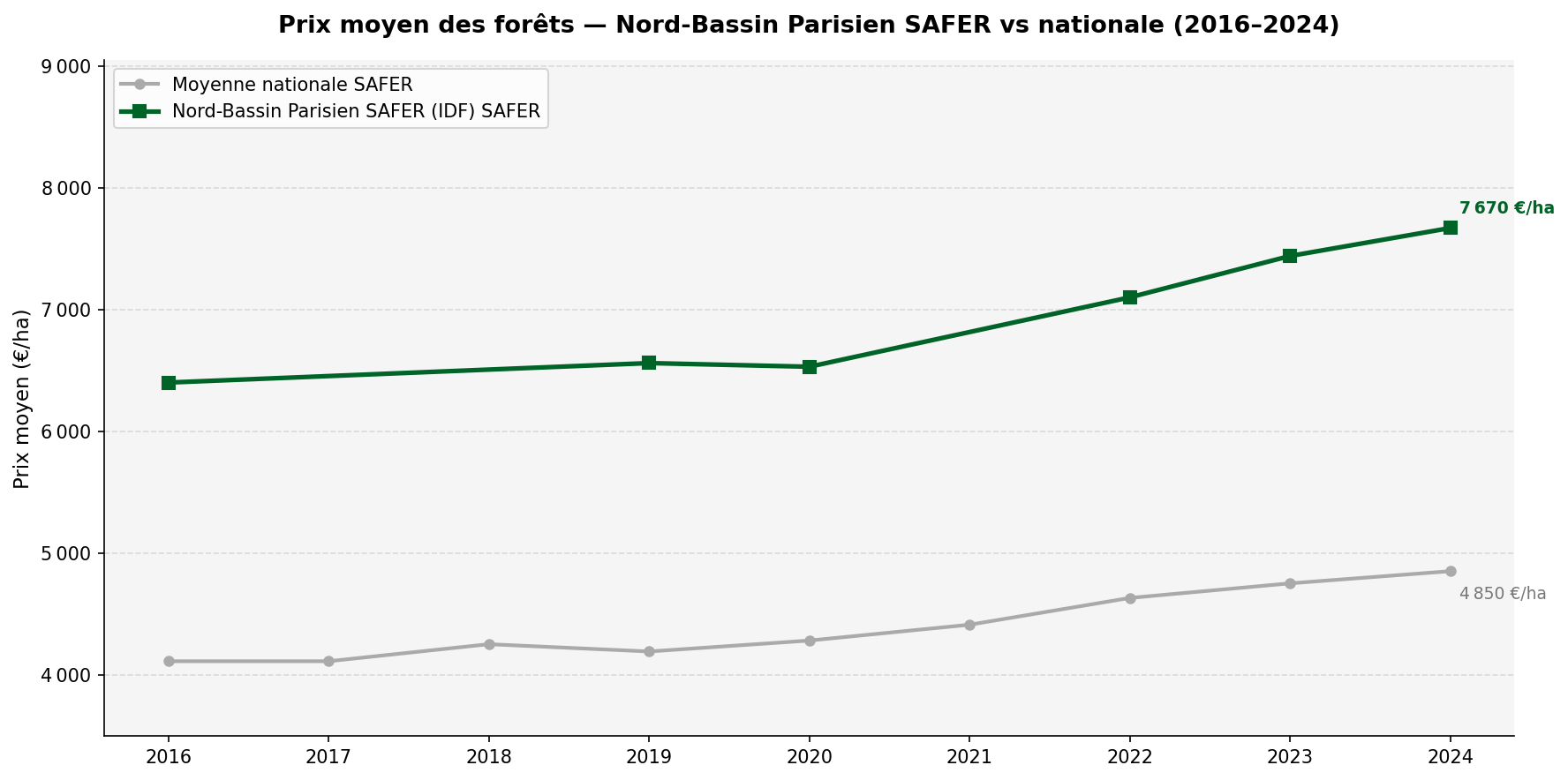

The Île-de-France region is linked by SAFER to the "Nord-Bassin Parisien" (North-Paris Basin) forest region, which also includes Hauts-de-France, eastern Normandy, and part of the Centre region. This region records the highest forest prices in France according to SAFER statistics, with €7,670/ha in 2024. The Paris region market weighs heavily in this average due to the high valuation of peri-urban forests with very high heritage value.

| Year | Average Price North-Paris Basin SAFER (€/ha) |

National Average Price SAFER (€/ha) |

|---|---|---|

| 2016 | 6,400 | 4,110 |

| 2019 | 6,560 | 4,190 |

| 2022 | 7,100 | 4,630 |

| 2023 | 7,440 | 4,750 |

| 2024 | 7,670 | 4,850 |

Source: Groupe Safer, Le Prix des Terres (2016–2024). Forest region "Nord-Bassin Parisien".

Average price of forests — North-Paris Basin SAFER vs national average (2016–2024) — Source: Groupe Safer, Le Prix des Terres

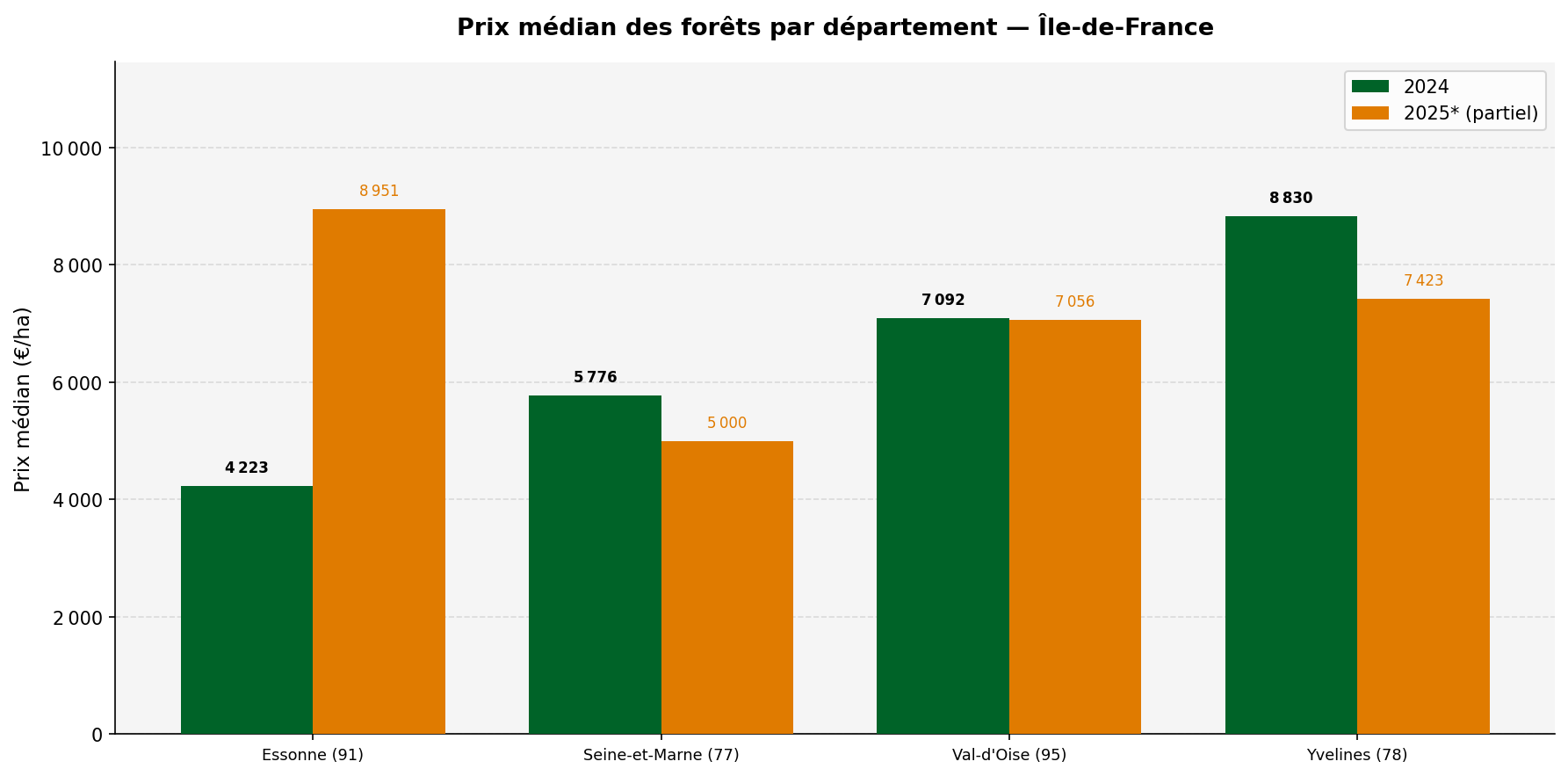

Median price of forests by department — Île-de-France, 2024 and 2025* — Source: DVF, processed by ma-propriete.fr

Important methodological note: In Île-de-France, the number of transactions per department remains low (17 to 73 transactions depending on the department and the year). The median prices presented here, particularly for 2025, should be interpreted with increased caution. Paris (75), Seine-Saint-Denis (93), and Val-de-Marne (94) do not show a significant forest market in the DVF data and are excluded from the analysis.

Seine-et-Marne is the reference forest department in Île-de-France, featuring the Fontainebleau massif (classified as a UNESCO Biosphere Reserve), the Trois Pignons forest, and many private massifs on the Brie plateaus. In 2024, the median price was €5,776/ha for 69 filtered transactions — the most liquid market in the region. In the 1st half of 2025, the median price is €5,000/ha (partial data to be interpreted with caution). Seine-et-Marne offers the best liquidity and a diverse choice of properties, making it the most accessible department for Paris region buyers.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 29 | 69 | 345 |

| Median price (€/ha) | €5,000 | €5,776 | €6,001 |

| Average price (€/ha) | €6,540 | €6,159 | €7,128 |

| Median area | — | — | 2.66 ha |

* Partial data for the 1st half of 2025.

Yvelines, with the Rambouillet forest (20,000 ha, largely state-owned) and the Marly and Saint-Germain massifs, constitutes a forest market of high heritage value but low liquidity. In 2024, the median price reached €8,830/ha, for only 17 filtered transactions. In the 1st half of 2025, the median price stood at €7,423/ha (partial data to be interpreted with caution, based on 8 transactions). The rarity and quality of the properties explain this high-end positioning.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 8 ⚠ | 17 | 83 |

| Median price (€/ha) | €7,423 ⚠ | €8,830 | €8,830 |

| Average price (€/ha) | €8,269 | €8,458 | €9,747 |

| Median area | — | — | 3.47 ha |

⚠ Low volume — indicative data. * Partial data for the 1st half of 2025.

Essonne is home to the southern part of the Fontainebleau forest as well as the Trois Pignons and Montmorency massifs. In 2024, the median price was €4,223/ha for 16 filtered transactions, a surprising level given the location. This figure reflects the market composition: plots are often landlocked, small, difficult to manage for forestry, and their value is more heritage-based than productive. In the 1st half of 2025, the 4 filtered transactions give a median of €8,951/ha, but this sample is too small to be significant.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 4 ⚠ | 16 | 92 |

| Median price (€/ha) | €8,951 ⚠ | €4,223 | €6,097 |

| Average price (€/ha) | €10,301 | €7,683 | €9,247 |

| Median area | — | — | 2.97 ha |

⚠ Very low volume — indicative data only. * Partial data for the 1st half of 2025.

Val-d'Oise has notable forest massifs — Isle-Adam, Montmorency, and Carnelle forests — but the private market is very narrow. In 2024, the median price reached €7,092/ha for only 9 filtered transactions. A single transaction in 2025 (€7,056/ha) does not allow for a reliable statistic. These data should be considered as simple orders of magnitude.

| Indicator | 2025* (H1) | 2024 | 2020-2025 |

|---|---|---|---|

| Transactions | 1 ⚠ | 9 | 57 |

| Median price (€/ha) | €7,056 ⚠ | €7,092 | €8,000 |

| Average price (€/ha) | €7,056 | €7,074 | €10,713 |

| Median area | — | — | 2.93 ha |

⚠ Very low volume — indicative data only. * Partial data for the 1st half of 2025.

DVF data cover forest and woodland transactions in Île-de-France between July 2020 and June 2025. An IQR filter is applied. The median price is the central indicator used.

In Île-de-France, the low liquidity of the private forest market makes annual statistics by department less robust. DVF data exclude the sale of shares in Forestry Groups (Groupements Forestiers) — which are particularly present for large estates in Seine-et-Marne and Yvelines. The high proportion of state-owned forests (not for sale) considerably reduces the available private supply. The years 2020 (H2) and 2025 (H1) are partial.

The SAFER North-Paris Basin region includes Île-de-France among several territories. The very high heritage value of certain Paris region forests (proximity to Paris, recreational uses, listed sites) produces high SAFER average prices for this forest region, which are not representative of the current market in each individual department.

Île-de-France presents an atypical forest market: low liquidity, high heritage value, but with median prices lower than regional wealth might suggest. In 2024, the median price of €6,000/ha places the region in the high national average, but far behind Normandy or Hauts-de-France. Seine-et-Marne accounts for most transactions and offers the best accessibility, while Yvelines and Val-d'Oise constitute a niche market for exceptional estates. For the Paris region buyer, the neighboring Centre-Val de Loire or Normandy regions often offer better value for money.

Consult our observatory of forest prices in France and our forest listings in Île-de-France.

| Region | Article |

|---|---|

| Auvergne-Rhône-Alpes | View article |

| Bourgogne-Franche-Comté | View article |

| Brittany | View article |

| Centre-Val de Loire | View article |

| Grand Est | View article |

| Hauts-de-France | View article |

| Île-de-France | This article |

| Normandy | View article |

| Nouvelle-Aquitaine | View article |

| Occitanie | View article |

| Pays de la Loire | View article |

| Provence-Alpes-Côte d'Azur | View article |