Auvergne-Rhône-Alpes is the third largest forest region in mainland France by area, with nearly 2.7 million hectares of forest, or approximately 45% of its territory. Its wooded massif is remarkably diverse: beech and fir forests in the Alps, chestnut and pine forests in Ardèche and Haute-Loire, oak forests in the Rhone corridor, spruces on the plateaus of the Massif Central… This silvicultural wealth is accompanied by a dynamic wood-forest sector, the leading industrial employer in the region in several departments.

This article presents, for the first time based on DVF (Demandes de Valeurs Foncières) data, a complete analysis of the forest market in Auvergne-Rhône-Alpes: median prices, transaction volumes, departmental disparities. The data covers the period July 2020 – June 2025, with the full years 2021 to 2024 serving as a reference. The 2025 data only covers the 1st half of the year and is presented for information purposes, with the necessary caution.

For a national perspective, find our observatory of forest prices in France, and for forest properties available for sale, consult our forest listings.

Over the entire 2020-2025 period, 4,706 forest transactions were recorded in the DVF data for the Auvergne-Rhône-Alpes region, involving 30,350 hectares exchanged. It is the fourth region in terms of number of sales, behind Nouvelle-Aquitaine, Occitanie and the Auvergne-Rhône-Alpes duo. In terms of hectare volume, the region accounts for approximately 11% of the national market.

The regional median price stands at €4,000/ha over the entire period, for an average price of €4,892/ha. The gap between the average and the median — nearly €900/ha — is a sign of significant dispersion: a few high-priced transactions, particularly in alpine or peri-urban areas, pull the average up, whereas the median better reflects the reality of the current market.

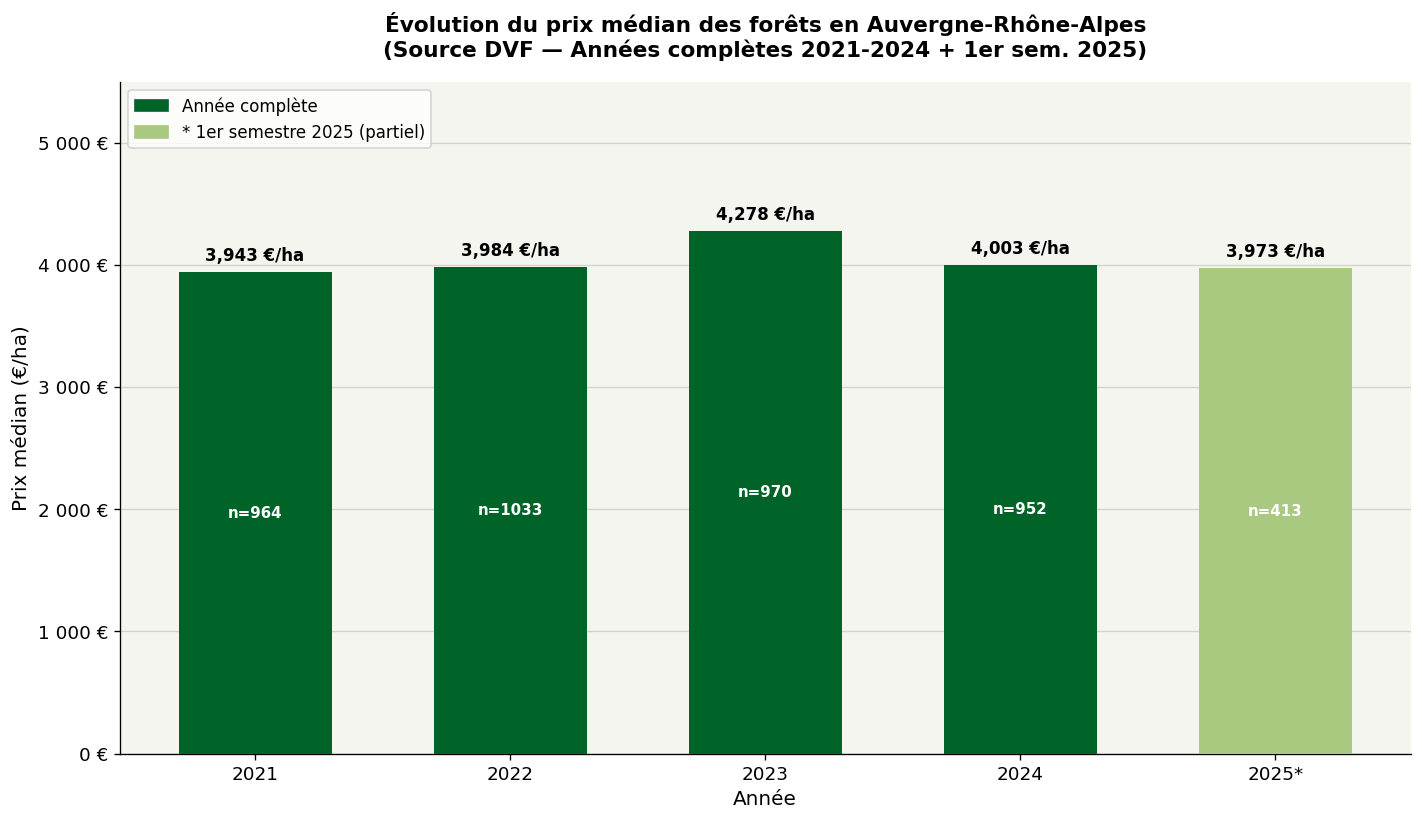

| Indicator | 2025* (H1) | 2024 | 2023 | 2022 | 2021 |

|---|---|---|---|---|---|

| Number of transactions | 413 | 952 | 970 | 1,033 | 964 |

| Median price (€/ha) | €3,973/ha | €4,003/ha | €4,278/ha | €3,984/ha | €3,943/ha |

| Average price (€/ha) | €4,737/ha | €5,027/ha | €5,037/ha | €4,888/ha | €4,795/ha |

| 1st quartile (€/ha) | €2,493/ha | €2,521/ha | €2,607/ha | €2,502/ha | €2,392/ha |

| 3rd quartile (€/ha) | €5,969/ha | €6,472/ha | €6,492/ha | €6,233/ha | €6,014/ha |

| Median area (ha) | 3.17 ha | 3.27 ha | 3.05 ha | 3.11 ha | 3.32 ha |

* Partial 2025 data — 1st half only (January-June 2025). To be interpreted with caution.

Evolution of the median price of forests in Auvergne-Rhône-Alpes (2021-2025) — Source: DVF, ma-propriete.fr processing

In terms of trends, the regional market shows relative stability over four years. The median price fluctuates between €3,943/ha (2021) and €4,278/ha (2023), with a modest peak in 2023 followed by a slight decline in 2024 to €4,003/ha. The 1st half of 2025 (partial data, to be interpreted with caution) falls within the same range, at €3,973/ha, with no sign of a breakthrough upwards or downwards. The region is below the national median (€4,846/ha in 2024), which reflects the nature of regional forest land: productive mid-mountain massifs but far from tight land markets.

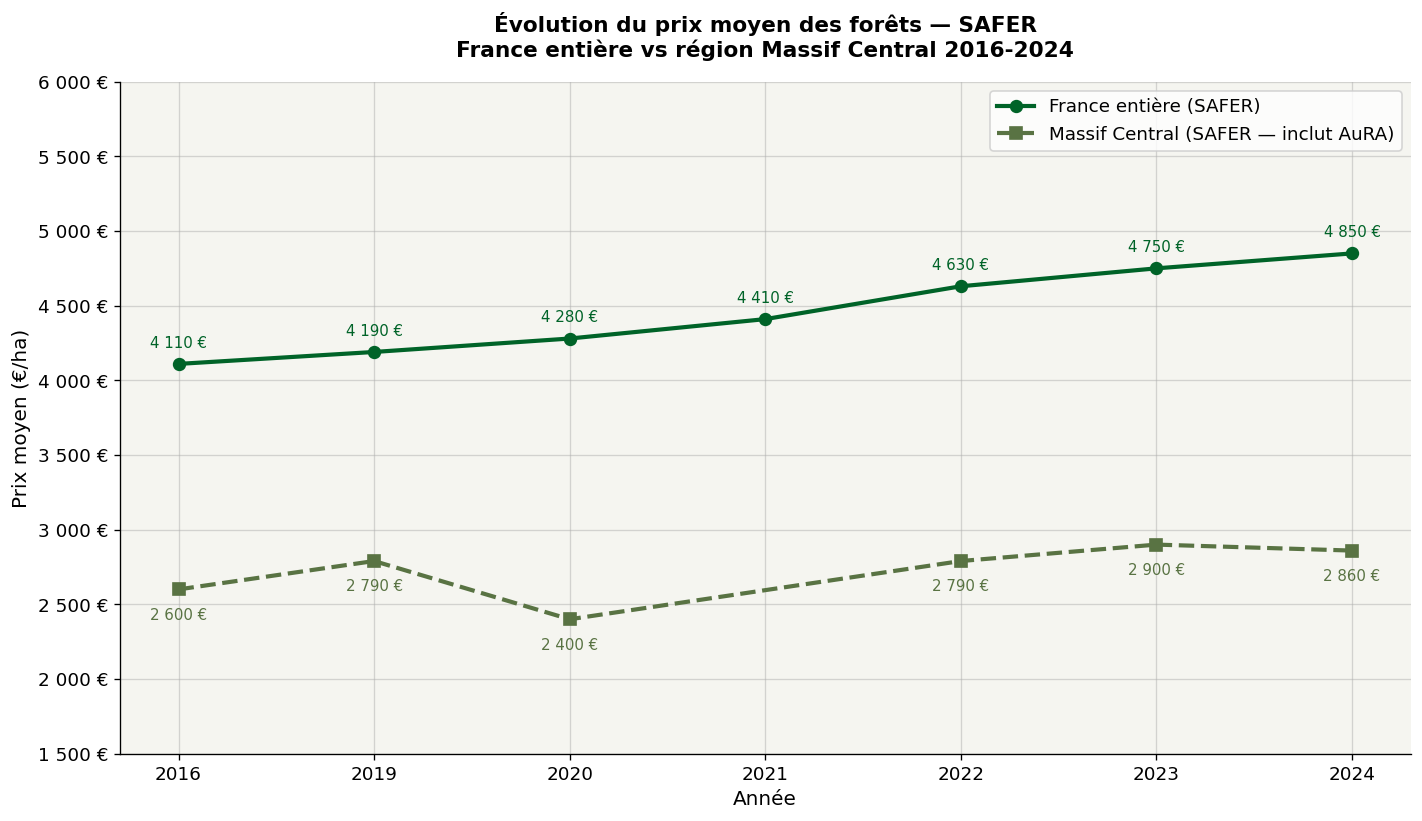

Data published annually by the SAFER Group allows for a historical reading since 1997. The Auvergne-Rhône-Alpes region partially overlaps two SAFER forest zones: the Massif Central (for the volcanic departments and upper Ardèche) and Alpes-Méditerranée-Pyrénées (for the alpine departments). The table below presents the national evolution and the Massif Central region, which remains the closest reference for a large part of the region's forests.

| Year | France (SAFER) | Massif Central (SAFER) | National variation |

|---|---|---|---|

| 2016 | €4,110/ha | €2,600/ha | — |

| 2019 | €4,190/ha | €2,790/ha | +2.0% |

| 2020 | €4,280/ha | €2,400/ha | +2.1% |

| 2022 | €4,630/ha | €2,790/ha | +5.0% |

| 2023 | €4,750/ha | €2,900/ha | +2.6% |

| 2024 | €4,850/ha | €2,860/ha | +2.1% |

Evolution of the average price of forests — SAFER, France vs Massif Central (2016-2024) — Source: Groupe SAFER, Le Prix des Terres

Two lessons emerge from this comparison. On the one hand, the Massif Central forest, mainly composed of conifers, beech forests and coppice, is sustainably valued below the national average (a gap of €1,700 to €2,000/ha depending on the year). On the other hand, the long-term trend is towards rising prices: +2.5% per year on average over the 2016-2024 period, confirming the growing status of the forest as a heritage asset. It should be noted that DVF and SAFER figures are not directly comparable: SAFER applies a hedonic model for equivalent quality, while DVF data integrates all recorded transactions, after filtering for extreme values.

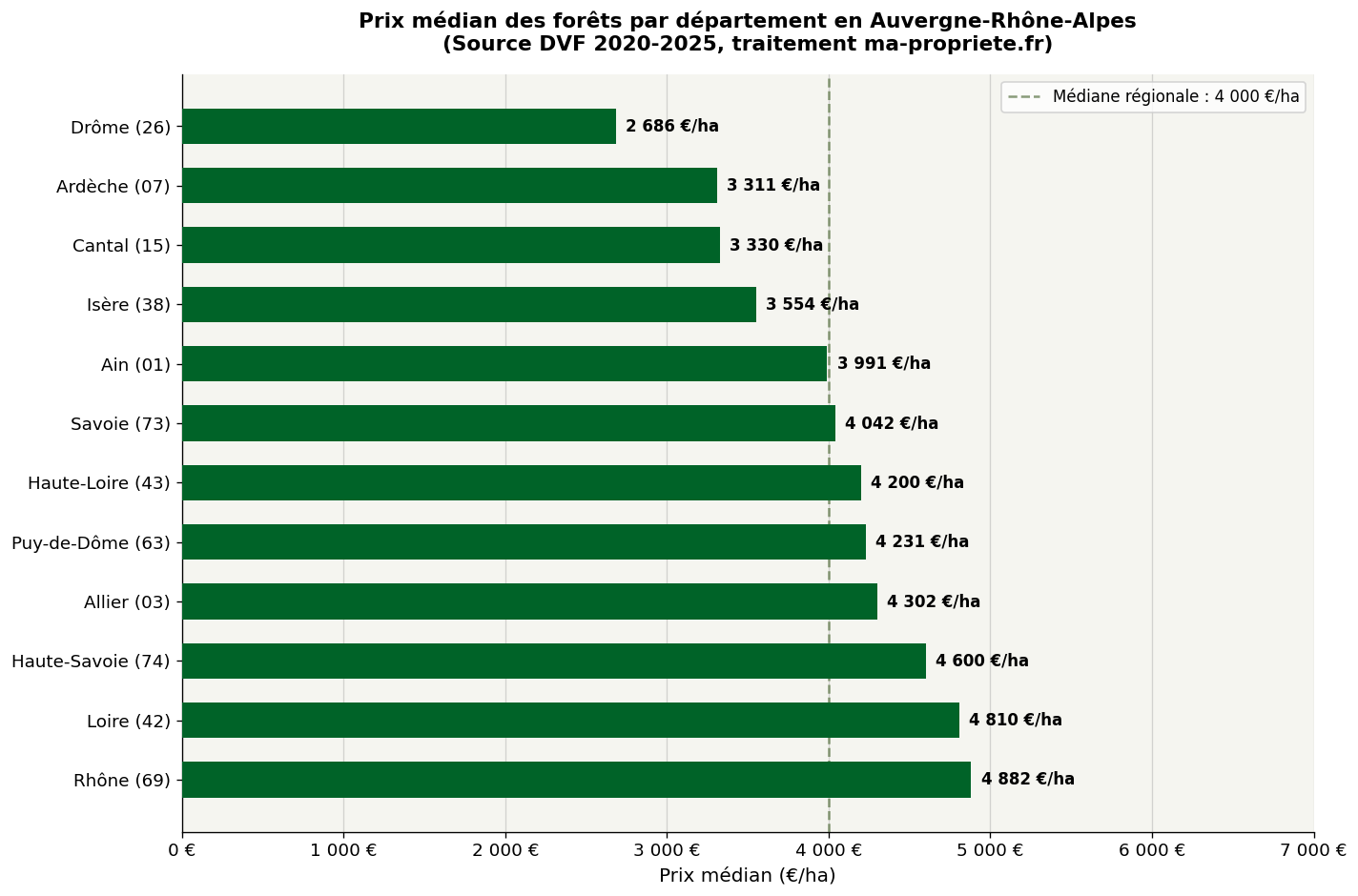

Median price of forests by department in Auvergne-Rhône-Alpes — Source: DVF 2020-2025, ma-propriete.fr processing

The department of Ain presents an active forest market with 295 transactions recorded over the period. The median price stands at €3,991/ha for an average price of €4,639/ha, with a median area of 3.4 ha. In 2024, the median price increased significantly to €4,740/ha (68 transactions), confirming a growing valuation of the massifs in Ain. The 1st half of 2025 (partial data, to be interpreted with caution) marks a decline to €3,207/ha, but on a very limited number of transactions (19), insufficient to draw a conclusion.

Ain offers great forest diversity: oak and hornbeam high forests in Bresse and Bugey, coniferous forests in the Jura massif, alluvial woodlands along the Saône. The proximity of the Lyon metropolitan area generates sustained residential and heritage demand.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 70 | €3,482/ha | €3,997/ha |

| 2022 | 57 | €3,918/ha | €4,844/ha |

| 2023 | 62 | €4,042/ha | €4,599/ha |

| 2024 | 68 | €4,740/ha | €5,133/ha |

| 2025* (H1) | 19 | €3,207/ha | €4,545/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Allier, a department in the heart of the Massif Central, shows a median price of €4,302/ha over the period, for an average price of €5,288/ha (220 transactions). The year 2023 was particularly remarkable with a peak at €6,028/ha median (40 transactions), before a decline in 2024 to €4,253/ha. The 1st half of 2025 (partial data) stabilized at €4,216/ha.

The forests of Allier are dominated by pedunculate oak in the plain areas and conifers on the heights of the Bourbonnaise Mountain. The Tronçais Forest, one of the most beautiful oak forests in Europe, contributes to the department's high-end forest image, even if transaction volumes are concentrated on smaller massifs.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 42 | €4,585/ha | €5,224/ha |

| 2022 | 54 | €4,099/ha | €5,207/ha |

| 2023 | 40 | €6,028/ha | €5,826/ha |

| 2024 | 55 | €4,253/ha | €5,525/ha |

| 2025* (H1) | 14 | €4,216/ha | €4,590/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Ardèche is the most forested department in the region in terms of the number of transactions: 652 sales recorded, with a median area of 3.87 ha. The median price stands at €3,311/ha, one of the lowest in the region, for an average price of €4,589/ha. The Ardèche market is characterized by strong dispersion: chestnut forests for fruit and silvicultural purposes in lower Vivarais, Mediterranean pine forests, and mixed forests on the northern plateaus. In 2024, the median price rose to €3,881/ha after a low in 2022. The 1st half of 2025 (partial data) marks a decline to €2,819/ha, but the 47 available transactions call for caution in interpretation.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 144 | €3,682/ha | €5,126/ha |

| 2022 | 142 | €3,008/ha | €4,459/ha |

| 2023 | 146 | €3,481/ha | €4,232/ha |

| 2024 | 118 | €3,881/ha | €5,004/ha |

| 2025* (H1) | 47 | €2,819/ha | €3,997/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

With 256 transactions and a median price of €3,330/ha, Cantal positions itself among the most accessible forest markets in the region. The average price of €3,752/ha is also the lowest in Auvergne-Rhône-Alpes. This situation reflects the nature of Cantal's forests: conifers from post-war reforestation (Douglas firs), oak coppices on the slopes, in a context of agricultural decline and distance from major demand basins. The 1st half of 2025 (partial data, to be interpreted with caution) is notable: 24 transactions at a median of €4,355/ha, the highest level since 2021 for this department — a signal to be confirmed over the full year.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 50 | €2,863/ha | €3,419/ha |

| 2022 | 55 | €2,984/ha | €3,335/ha |

| 2023 | 54 | €3,168/ha | €4,170/ha |

| 2024 | 47 | €3,300/ha | €3,530/ha |

| 2025* (H1) | 24 | €4,355/ha | €4,877/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Drôme records the lowest median price in the region: €2,686/ha for 322 transactions. The median area of 4.2 ha is one of the highest in Auvergne-Rhône-Alpes, which reflects the structure of the local market around intermediate-sized properties. Drôme's forests cover very varied contexts: Scots and pubescent pine on the reliefs of Provençal Drôme, pubescent and holm oaks in the Rhone valley, conifers in Vercors and Diois. This climatic diversity — from semi-arid Mediterranean to mountain — induces a high variability in values. The 1st half of 2025 (partial data) stands at €2,816/ha (30 transactions), in line with previous years.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 74 | €2,357/ha | €3,515/ha |

| 2022 | 63 | €3,569/ha | €4,766/ha |

| 2023 | 58 | €3,872/ha | €4,095/ha |

| 2024 | 73 | €2,378/ha | €3,786/ha |

| 2025* (H1) | 30 | €2,816/ha | €2,966/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Isère presents 424 transactions and a median price of €3,554/ha, for an average price of €4,205/ha and a median area of 3.17 ha. The Isère market is driven by a double demand: heritage in the peri-urban valleys of Grenoble and North Isère, and silvicultural in the Chartreuse, Vercors and Belledonne massifs. Stability is the dominant characteristic: the median price fluctuates between €3,366/ha (2021) and €4,000/ha (2022), with no marked trend over the period. The 1st half of 2025 (partial data) stands at €3,732/ha (36 transactions).

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 84 | €3,366/ha | €3,896/ha |

| 2022 | 93 | €4,000/ha | €4,674/ha |

| 2023 | 95 | €3,561/ha | €3,912/ha |

| 2024 | 82 | €3,500/ha | €4,320/ha |

| 2025* (H1) | 36 | €3,732/ha | €4,056/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Loire stands out as one of the most valued markets in the region: a median price of €4,810/ha over the period, for an average price of €5,710/ha (527 transactions). The median area of 2.38 ha — the lowest in the region — reflects demand oriented towards small woodlands for leisure purposes in a peri-urban context (Saint-Etienne basin, Forez plain). The years 2022 and 2023 were dynamic, with medians at €5,038 and €5,237/ha respectively. The 1st half of 2025 (partial data, to be interpreted with caution) stands at €4,973/ha (55 transactions), confirming Loire's high positioning.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 90 | €3,996/ha | €4,776/ha |

| 2022 | 119 | €5,038/ha | €5,897/ha |

| 2023 | 110 | €5,237/ha | €6,539/ha |

| 2024 | 109 | €4,810/ha | €5,822/ha |

| 2025* (H1) | 55 | €4,973/ha | €5,407/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Haute-Loire has 568 transactions for a median price of €4,200/ha and an average price of €4,919/ha. This Massif Central department is characterized by coniferous forests on the Velay and Mézenc plateaus, and mixed woodlands in the gorges. The market is relatively active and regular in transaction volume. The year 2021 marked a peak with a median at €4,745/ha, while 2024 shows a decline to €3,536/ha. The 1st half of 2025 (partial data) stands at €3,466/ha (55 transactions).

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 119 | €4,745/ha | €5,248/ha |

| 2022 | 135 | €3,977/ha | €4,649/ha |

| 2023 | 109 | €5,029/ha | €5,390/ha |

| 2024 | 102 | €3,536/ha | €4,644/ha |

| 2025* (H1) | 55 | €3,466/ha | €4,562/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Puy-de-Dôme is the most active department in the region in terms of the number of transactions: 695 sales, representing nearly 15% of the regional market. The median price of €4,231/ha for an average price of €4,877/ha places this department in the regional median range. Puy-de-Dôme's forests cover the flanks of the Chaîne des Puys, the Combrailles, the Livradois and the Forez: oaks, chestnuts, Douglas firs and spruces coexist in a dense bocage fabric. The market remains steady, with no strong directional trend over the 2021-2024 period. The 1st half of 2025 (partial data, to be interpreted with caution) stands at €4,762/ha (67 transactions), above the 2024 level.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 136 | €4,210/ha | €4,986/ha |

| 2022 | 159 | €4,019/ha | €4,740/ha |

| 2023 | 136 | €4,435/ha | €4,863/ha |

| 2024 | 139 | €4,032/ha | €4,812/ha |

| 2025* (H1) | 67 | €4,762/ha | €5,222/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Rhône shows the second highest median price in the region: €4,882/ha over the period, for an average price of €5,786/ha (374 transactions). The median area of 2.81 ha reflects demand oriented towards small peri-Lyon woodlands, often acquired for leisure or heritage diversification. The year 2023 was particularly sustained, with a median at €5,977/ha. The 1st half of 2025 (partial data, to be interpreted with caution) stands at €5,155/ha (29 transactions), in line with 2024 levels.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 85 | €4,183/ha | €5,103/ha |

| 2022 | 73 | €4,379/ha | €6,126/ha |

| 2023 | 81 | €5,977/ha | €6,721/ha |

| 2024 | 74 | €5,034/ha | €5,480/ha |

| 2025* (H1) | 29 | €5,155/ha | €6,711/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

Savoie presents the smallest market in terms of volume in the region: only 142 transactions, with a median area of 2.61 ha. Its median price of €4,042/ha is misleading because the average price reaches €6,112/ha — one of the highest in Auvergne-Rhône-Alpes. This significant gap signals the presence of exceptional transactions, particularly on high mountain properties or bordering ski areas. Interannual variability is strong: a median at €6,026/ha in 2021, then €2,718/ha in 2022. The 1st half of 2025 (partial data, to be interpreted with caution) stands at €4,199/ha (18 transactions — insufficient volume for robust analysis).

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 29 | €6,026/ha | €9,143/ha |

| 2022 | 35 | €2,718/ha | €3,804/ha |

| 2023 | 27 | €3,085/ha | €4,290/ha |

| 2024 | 30 | €4,462/ha | €8,681/ha |

| 2025* (H1) | 18 | €4,199/ha | €4,564/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution. Low transaction volume — limited interpretation.

Haute-Savoie has 231 transactions with a median price of €4,600/ha and an average price of €5,495/ha. It is the third highest median price in the region, behind Rhône (€4,882/ha) and Loire (€4,810/ha). The median area of 2.09 ha — the lowest in the entire region — reflects a fragmented market, where small peri-urban plots around Annecy, Thonon and Annemasse concentrate a significant share of sales. The trend over 2021-2024 is towards stability, with medians between €4,500 and €5,000/ha. The 1st half of 2025 (partial data) marks a decline to €3,300/ha, but on a volume of only 19 transactions.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 41 | €4,978/ha | €4,767/ha |

| 2022 | 48 | €5,000/ha | €5,767/ha |

| 2023 | 52 | €4,500/ha | €5,520/ha |

| 2024 | 55 | €4,752/ha | €5,506/ha |

| 2025* (H1) | 19 | €3,300/ha | €5,160/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution. Low transaction volume — limited interpretation.

Haute-Savoie has 231 transactions with a median price of €4,600/ha and an average price of €5,495/ha. It is the third highest median price in the region, behind Rhône (€4,882/ha) and Loire (€4,810/ha). The median area of 2.09 ha — the lowest in the entire region — reflects a fragmented market, where small peri-urban plots around Annecy, Thonon and Annemasse concentrate a significant share of sales. The trend over 2021-2024 is towards stability, with medians between €4,500 and €5,000/ha. The 1st half of 2025 (partial data) marks a decline to €3,300/ha, but on a volume of only 19 transactions.

| Year | No. sales | Median price | Average price |

|---|---|---|---|

| 2021 | 41 | €4,978/ha | €4,767/ha |

| 2022 | 48 | €5,000/ha | €5,767/ha |

| 2023 | 52 | €4,500/ha | €5,520/ha |

| 2024 | 55 | €4,752/ha | €5,506/ha |

| 2025* (H1) | 19 | €3,300/ha | €4,789/ha |

* Partial data for the 1st half of 2025, to be interpreted with caution.

The data presented in this article is taken from the DVF (Demandes de Valeurs Foncières) database, published by the Ministry of Economy. This database lists all real estate transfers that have occurred in France, with the exception of the local regime of Alsace-Moselle (Bas-Rhin, Haut-Rhin, Moselle).

The processing method applied by ma-propriete.fr includes the following steps: selection of transactions relating to wood-type properties (high forests, coppices, poplar groves and other forest stands); exclusion of transactions with an area of less than 1 hectare; removal of prices below €500/ha and above €100,000/ha; and finally, exclusion of the 25% of transactions with the lowest prices and the 25% with the highest prices in each department. This last step — which amounts to keeping only the central interquartile — aims to eliminate poorly qualified mixed assets and atypical transactions, to retain only the current market.

The median price is systematically preferred to the average price as a trend indicator, as it is less sensitive to exceptional transactions. The average price is provided for supplementary purposes.

Several limitations deserve explanation. First, the DVF database excludes the three departments of the Alsace-Moselle local regime (67, 68, 57), whose forest market is managed by a different legal regime — which explains their absence from the statistics. Secondly, DVF data only records sales of real estate in the strict sense: they do not include the transfer of shares in companies, particularly Forestry Groups (GF) and Forestry Land Groups (GFF). These structures nevertheless represent a significant part of the market for large forest estates, which often have a Simple Management Plan. This exclusion implies that DVF statistics under-represent the high-end segment of the market. Thirdly, the 2020 data only covers the second half of the year (July-December), and the 2025 data only the first half (January-June): these two partial years are not comparable to the full years 2021-2024. Fourthly, the cadastral qualification of forest plots is not always homogeneous from one department to another, which can introduce biases in inter-departmental comparisons.

SAFER publishes its forest market statistics every year as part of the annual report Le Prix des Terres. Its methodology differs significantly from that applied to DVF data. SAFER uses a hedonic model that adjusts prices to constant quality, notably by neutralizing the area structure of sales. It works on regional forest perimeters (GRECO/IGN) which do not correspond to administrative regions: thus, part of Auvergne-Rhône-Alpes falls under the "Massif Central" forest region, and another under "Alpes-Méditerranée-Pyrénées". By construction, SAFER prices tend to be more stable from one year to the next, as they are less sensitive to fluctuations in market composition. The geographical positioning of the two sources may also differ for departments located on the edge of several climatic zones.

The forest market in Auvergne-Rhône-Alpes presents a dual characteristic: structural price stability over the 2021-2024 period, with a median price oscillating around €4,000/ha, and strong departmental heterogeneity, with gaps ranging from €2,686/ha in Drôme to €4,882/ha in Rhône. The region is positioned below the national median (€4,846/ha in 2024), which reflects the nature of its forest heritage: productive massifs but in mid-mountain areas, far from the tightest land markets. Partial data for the 1st half of 2025 (to be interpreted with caution) does not indicate a break in the trend. To go further in your acquisition or sale process, consult our national forest price observatory and our forest listings in Auvergne-Rhône-Alpes.

| Region | Link to the article |

|---|---|

| Nouvelle-Aquitaine | Forest prices in Nouvelle-Aquitaine |

| Occitanie | Forest prices in Occitanie |

| Bourgogne-Franche-Comté | Forest prices in Bourgogne-Franche-Comté |

| Grand Est | Forest prices in Grand Est |

| Centre-Val de Loire | Forest prices in Centre-Val de Loire |

| Normandie | Forest prices in Normandie |

| Hauts-de-France | Forest prices in Hauts-de-France |

| Bretagne | Forest prices in Bretagne |

| Pays de la Loire | Forest prices in Pays de la Loire |

| Provence-Alpes-Côte d'Azur | Forest prices in Provence-Alpes-Côte d'Azur |

| Île-de-France | Forest prices in Île-de-France |