Understanding the different forms of real estate ownership in France can be difficult. We have written this article to give you a clear and accessible understanding of them by applying them to the ownership of a rural property, whether agricultural, equestrian, wine-growing, forestry or residential.

It is indeed crucial to understand the different options available to you in terms of real estate ownership. This will allow you to make informed decisions, protect your interests and optimize the use of your property. Whether you are interested in full ownership, split ownership, usufruct, life annuity or other forms of holding, we will explore each of them.

Full ownership is the most common and best-known form of real estate ownership and applies by default. It represents the total and exclusive ownership of a property. In other words, being a full owner means holding all rights to a property, including the right to use it, modify it, rent it, sell it or destroy it, subject to current laws and regulations.

As a "full owner", you benefit from various rights and responsibilities. First of all, you have the power to fully enjoy your property. This means you can occupy it, live in it or use it according to your needs and desires. You also have the possibility of temporarily transferring your property by renting it, which can generate income.

However, full ownership also involves responsibilities. You are responsible for the maintenance and upkeep of your property, as well as the associated charges and taxes. This includes repair costs, property taxes, insurance and current expenses related to the property.

Full ownership offers several advantages to rural owners. First of all, it gives you great freedom in the use of your property. You can operate your property according to your own needs and aspirations, whether for agriculture, viticulture, livestock, landscaping or other rural activities. You have full control over decisions regarding your property, without having to consult other parties.

Furthermore, full ownership offers long-term stability and security. You are not limited in time and you can pass your property on to your heirs or sell it according to your will. Full ownership therefore constitutes a lasting heritage for future generations.

On the downside, the acquisition of rural property in full ownership can require a significant financial investment. In addition, you are solely responsible for the maintenance and management costs of the property. In a rural context, this can involve considerable expenses related to land maintenance, agricultural buildings, etc.

Split ownership consists of the separation of property rights between two distinct parties: the bare owner and the usufructuary. This division creates a coexistence of rights over the same real estate, with specific roles and rights for each party.

The bare owner holds the bare ownership, i.e. the property rights to the asset, with the exception of its use and income. The primary role of the bare owner is to own the property as a future owner, once the usufruct has ended. However, during the period of splitting, the bare owner does not have the right to use the property or receive the income it may generate.

The rights of the bare owner include in particular the right to dispose of the bare ownership, for example by selling it or passing it on by inheritance. However, these rights are limited by the rights of the usufructuary during the split ownership period. The bare owner also has the duty to maintain the property and keep it in good condition until the end of the split ownership.

On the other hand, the usufructuary holds the usufruct, which gives them the right to use the property and receive its income during the period of split ownership. The usufructuary can live in the property, rent it and collect the rents, or exploit the income from the activity of the property. In return, they will have to assume maintenance charges, property taxes, etc.

The rights of the usufructuary are temporary and are limited by the duration of the split ownership or by their death. The usufructuary has the right to enjoy the property and receive its fruits, but they cannot dispose of the bare ownership without the consent of the bare owner.

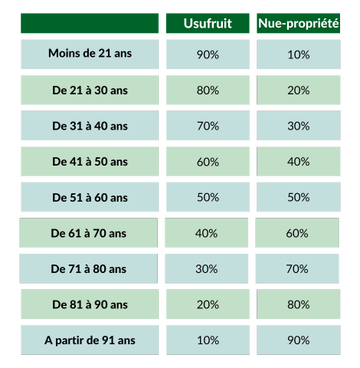

Usufruct is generally for life, meaning it disappears upon the death of the usufructuary to join the bare ownership and thus reconstitute the full ownership of the property. In this case, the valuation of the usufruct (and consequently the bare ownership) from a tax point of view is determined according to the age of the usufructuary:

Usufruct can be successive, meaning it will be passed successively to several beneficiaries, generally in a pre-established order. For example, an owner can make a donation with a reservation of usufruct and provide that upon their death the usufruct be passed to their spouse, then to their children after the death of the spouse. This form of holding allows for a progressive transmission of the use and income of the property to different generations, while retaining the property itself.

Usufruct can also be temporary. It is thus granted to a person for a fixed period and in this case its valuation is tax-estimated at 23% of the full ownership value for each 10-year period.

Split ownership can be advantageous in different situations.

First of all, it can allow an owner to pass on their heritage while retaining certain rights, in particular the right to continue using the property during their life. This can be particularly interesting for rural owners who wish to progressively unburden themselves of the management of their property while retaining its benefits.

In addition, split ownership can be used as an inheritance and tax planning strategy. Thus, an owner can pass the bare ownership of their property to their descendants. Gift taxes will be calculated on a value lower than the full ownership value (valuation of the usufruct according to the age of the usufructuary) which will reduce the amount of taxes to be paid. Upon the death of the usufructuary, the usufruct automatically joins the bare ownership without additional taxes to pay.

In practice, the owner makes a gift of the bare ownership to their heirs. Gift taxes are calculated on a reduced value (based on the age of the usufructuary) and will therefore be lower than those calculated on the full ownership of the property.

At the death of the usufructuary, the usufruct automatically joins the bare ownership to reconstitute full ownership. This operation is not then subject to inheritance taxes.

However, it is essential to understand the tax and inheritance consequences of split ownership. Thus, it is the usufructuary who will be liable for property taxes and also for the Real Estate Wealth Tax for the full ownership value of the property.

Split ownership often finds practical use in the context of the transmission of rural properties and, more broadly, businesses.

A farmer reaching retirement age can, for example, make a donation with reservation of usufruct of agricultural land to their children. The land is then leased to the person taking over the farm, whether or not they are an heir. The young retiree has thus passed on their land assets to their descendants at a lower cost, while preserving additional income at the time of retirement through the collection of farm rents.

The life annuity is a particular real estate sale concept where the payment for the property is made in the form of a life annuity, i.e. a periodic payment until the death of the seller. This form of transaction offers an interesting alternative to rural owners wishing to sell their property while ensuring a regular income for the rest of their lives.

In a life annuity, there are two parties involved: the seller, also called the annuitant, and the buyer, called the debtor. The role of the annuitant is to sell their real estate and receive the payment of the life annuity until the end of their life. The amount of the annuity is generally fixed during the sale, taking into account elements such as the age of the annuitant, the value of the property and the specific conditions of the transaction.

On the other hand, the debtor, as the buyer, undertakes to pay the life annuity to the annuitant. In addition to the annuity, the debtor also assumes the charges and responsibilities related to the property, including maintenance costs and property taxes. The debtor acquires full ownership of the property, but can only fully enjoy it after the death of the annuitant.

The sale in life annuity allows for the transmission of costs and constraints related to the management and maintenance of the property while retaining the use of the asset. This can be attractive for rural owners who wish to unburden themselves of the responsibilities associated with the property while benefiting from a continuous income.

However, it is important to consider certain disadvantages of the life annuity. For example, the amount of the life annuity can be influenced by several factors such as the life expectancy of the annuitant, economic conditions and the characteristics of the property.

Furthermore, for the buyer, the life annuity also presents risks, notably that of paying an annuity for a long period if the annuitant lives longer than expected. In addition, the buyer must take into account the costs and responsibilities associated with the property during the duration of the life annuity.

The use of companies to hold real estate assets is increasingly frequent, particularly through real estate companies. But all types of companies, civil or commercial, can hold buildings and specifically rural buildings.

The creation of a company will bring complexity to the ownership and management of a property (incorporation, accounting, general meetings, etc.) but allows for certain objectives to be met:

It is also possible to set up split ownership either on the shares held by the partners or on the buildings held by the company.

It is essential to seek advice from specialists before committing to a company incorporation, who will take into account your personal situation and your objectives to advise you on the appropriate legal path.

Companies are increasingly used in rural matters, whether for specific real estate companies: Agricultural Land Group (GFA), Viticultural Land Group (GFV), Forestry Groups, etc., or for operating companies: civil companies, EARL, GAEC, etc. They allow for the organization of the holding and transmission of rural heritage, the organization of work between several people, the choice of different social security regimes, etc.

Within the framework of an Agricultural Land Group (GFA), shares are generally valued based on the market value of the land held. For agricultural land, our land price observatory (2024 DVF data) constitutes an objective reference: the average price is €6,038/ha at the national level, with strong disparities according to regions (from €2,904/ha in Bourgogne-Franche-Comté to €13,007/ha in PACA).

The use of long-term leases associated with Land Groups thus allows for benefiting from additional exemptions from inheritance tax.

In addition to the forms of real estate ownership already mentioned, there are other less common but equally important concepts to know. Among these forms of holding is emphyteusis, which can present interesting applications in the rural context.

Emphyteusis (or emphyteutic lease) is a form of real estate ownership in which an owner grants a real right to another person, called the emphyteuta, to use and exploit the property for an extended period, generally several decades. The emphyteuta has the right to enjoy the property and receive its fruits, while having the obligation to maintain and preserve the property. At the end of the emphyteusis period, the property automatically returns to the original owner.

Emphyteusis can be used for long-term projects in the rural field, such as leasing agricultural land over an extended period. It offers farmers and operators the stability and security necessary to develop and invest in their activities, while preserving long-term land ownership.

We hope this article will be useful to you in gaining a clear understanding of the different forms of real estate ownership in France, focusing on those most relevant to rural owners without prior legal knowledge.

Each form of ownership has its own characteristics, rights and responsibilities for owners. It is essential to understand the advantages and disadvantages of each form in order to make informed decisions regarding the management of one's rural real estate heritage.

It is important to remember that every situation is unique, and it is recommended to consult a professional specialized in real estate law or inheritance planning to obtain personalized advice. These experts can help assess the rural owner's objectives, needs and specific constraints, and provide solutions adapted to their situation.